Download

1 / 20

200 likes | 339 Views

Governance & reporting considerations in the new world of NFPs & the ACNC. Dr Eva Tsahuridu – Policy Adviser, Professional Standards & Governance, CPA Australia Ram Subramanian – Policy Adviser, Reporting and Auditing, CPA Australia. Overview. Statutory definition of charity

E N D

Governance & reporting considerations in the new world of NFPs & the ACNC Dr Eva Tsahuridu – Policy Adviser, Professional Standards & Governance, CPA Australia Ram Subramanian – Policy Adviser, Reporting and Auditing, CPA Australia

Overview • Statutory definition of charity • Governance standards • New financial reporting requirements from 1 July 2013 • Annual information statements • Reduction in red tape

Governance • ‘the set of practices and procedures in place to ensure that an entity operates to achieve its objectives in an effective and transparent manner’ (explanatory statement) • Need for strategy / direction & control & transparency • Responsible persons need to ensure that financial affairs are managed in a responsible manner and for the entity’s purpose • Members of the governing body are the responsible persons in an entity. • Who are the responsible persons in your entity? • Treasurers would ordinarily be considered responsible persons • responsibility for ensuring that finances are in order, but also: • role in preparation of financial statements / annual information statement • role in ensuring compliance with governance standards

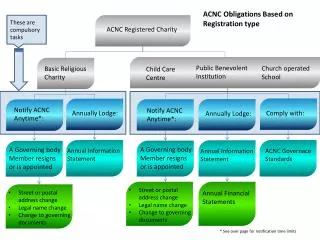

Governance Standards • Governance standards apply to all ACNC registered entities (except basic religious entities) • Effective from 1 July 2013 • Entities need to choose how to comply with the principles of the governance standards • what needs to be done in order to ensure compliance may vary between entities • standards specify what needs to be achieved, rather than how each entity can achieve the specific outcomes in its unique circumstances • External conduct standards (expected in 2013) • to regulate funds sent by registered charities outside Australia, and their activities outside Australia

Purpose of governance standards • provide a minimum level of confidence to the public that registered entities: • manage their affairs openly, accountably and transparently • use their resources (including contributions and donations) effectively and efficiently • minimise the risk of mismanagement and misappropriation, and • pursue their purposes. • policies, processes and systems help entities comply with the governance standards- attention to values and culture is also required

Governance Standards a • Standard 1 - purposes and not-for-profit nature of a registered entity • Need to comply with purpose • Accounting system to ensure donations etc. used for purpose • Need to provide information on purpose and nfp character of entity • How do you demonstrate that your entity runs a not for profit entity and works for its charitable purpose? • How do you inform the public about your charitable purpose? • Standard 2 - accountability to members • If you have members: • How do you fulfill your accountability obligations to them? • How do you enable them to ask questions about the running of the entity?

Governance Standards b • Standard 3 - compliance with Australian laws • Need to ensure that a registered entity is governed in a way that ensures its on going operations and the safety of its assets, through compliance with Australian laws (including preventing the misuse of its assets) • Are you aware of your entity’s legal obligations? • Do you have appropriate controls and systems in place?

Governance Standards c • Standard 4 - suitability of responsible entities • ‘A responsible entity’ is an entity responsible for the control and/or management of a registered entity. E.g. trustee of a charitable trust, director, board, committee member. • A registered entity must be satisfied that its responsible entities are not disqualified from managing a corporation; or disqualified by the Commissioner, at any time in the preceding 12 months, from being a responsible entity of a registered entity. • How do you ensure that responsible entities are suitable? • How do you check that they are not unsuitable?

Governance Standards d • Standard 5 - duties of responsible entities • exercising due care and diligence (reasonable person test) • acting in good faith in the best interests of the registered entity, to further the purposes of the registered entity • not misusing position or information • disclosing perceived or actual material conflicts of interest • ensuring responsible management of financial affairs • not allowing the registered entity to operate while insolvent. • How do you make responsible entities aware of their duties? • How do you ensure they behave in accordance with those duties? • What processes do you have in place to deal with non fulfillment of duties? • What processes/policies/procedures do you have in place to deal with conflicts of interest? • What processes/policies/procedures do you have in place to ensure responsible financial management?

Financial reporting – some points to consider • Financial reporting requirements • Reporting to other regulators • The Reporting Entity concept • Some audit and review considerations • Annual Information Statements • Some key takeaway points

Financial reporting requirements from 1 July 2013 • ACNC Act requirements • ACNC Amendment Regulation 2013 (no. 3) • Sets out requirements for annual financial reports • Responsible entities’ declaration • Standards applicable to special purpose financial reports • Transitional rules – medium and large charities • One year grace period for financial report preparation if: • Not currently preparing financial reports complying with accounting standards • Medium and large entities can provide a statement consisting specified information (similar to Annual Information Statement)

Reporting obligations to other regulators SOURCE:REGULATORY IMPACT ASSESSMENT OF POTENTIAL DUPLICATION OF GOVERNANCE AND REPORTING STANDARDS FOR CHARITIES - COAG

Reporting obligations to other regulators Example • incorporated in ACT • Income $230,000 • Gross assets $200,000 • Current assets $45,000 • Members 1,500 ACNC • No financial reports • No audit or review • AIS required (minimal information) Australia Capital Territory • Financial reports required • Audit required

Reporting obligations to other regulators Example • incorporated in Queensland • Turnover $120,000 • Gross assets $250,000 • Current assets $120,000 • Members 850 ACNC • No financial reports • No audit or review • AIS required (minimal information) Queensland • Financial reports required • Audit required

The Reporting Entity Concept • Definitions for what constitutes a “Reporting Entity” “an entity in respect of which it is reasonable to expect the existence of users who rely on the entity’s general purpose financial statements for information that will be useful to them for making and evaluating decisions about the allocation of resources” “General purpose financial statements are those intended to meet the needs of users who are not in a position to require an entity to prepare reports tailored to their particular information needs” • Dependent users • Separation of management from economic interest • Economic or political importance • Financial characteristics • Research by Australian Accounting Standards Board

The Reporting Entity Concept • Example: likely reporting entity • Well-known charitable company limited by guarantee • Revenue $15 million • Members 500,000 • Employees 300 • Creditors 60 • Directors 15 • Raises funds from public through debenture issue & donations • Example: likely non-reporting entity • Incorporated association • Revenue $255k • Members and management committee 10 • Loan from local bank

Some audit and review considerations • Who can do the audit or review? • Responsibility for selecting accounting policies, estimates and judgements rest with preparer of financial statements • Implications if being audited or reviewed for the first time • Feedback from the audit/review process

Annual information statements – some points to consider • Required by all charities (small, medium and large) • Publicly available • Not audited or assured • Some detail on income, and grants and donations made • Could be cash based for small charities

Some takeaway points • Plan and prepare • Additional reporting requirements • Transitional rules – comparative information