Download

1 / 9

90 likes | 200 Views

Coordination of tax policies in the EU: the case of anti-abuse measures. Michel Aujean Former Director of Tax Policy EU Commission, Associé Taj, France. Direct taxation: Role of ECJ Jurisprudence.

E N D

Coordination of tax policies in the EU: the case of anti-abuse measures Michel Aujean Former Director of Tax Policy EU Commission, Associé Taj, France

Direct taxation: Role of ECJ Jurisprudence • Court’s jurisprudence mostly concerned with “the four freedoms”, prohibits discrimination/obstacles to cross-border economic activity within the Internal Market • EU Commission (Tax Policy Communication of May 2001): “more pro-active strategy in the field of tax infringements” • Asymmetric effects: “the Court can only destroy but not positively legislate” (negative integration) • Even where a ruling forces a number of Member States to introduce new tax rules they often do so in vastly differing ways.

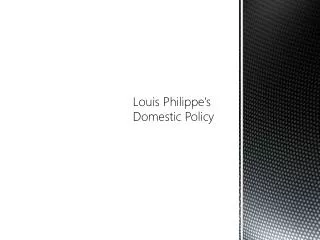

Direct tax cases decided by/pending before the ECJ (by year of reference to the Court)

The Need for Coordination of Tax Systems • Solutions: -”Litigation”:“more pro-active strategy in the field of tax infringements” (Tax Policy Communication of May 2001), -”Harmonisation”: = replacing national systems by a common EU system ( as for VAT); but either not required for the single market (goes beyond what is necessary in most cases), or not possible in the present institutional setting (EP only consulted, unanimity), =>”Coordination of tax systems”: the search of a constructive solution adopted by consensus can be an attractive and effective tool = building on national systems but rendering them compatible with the Treaty and with each other.

The Scope of the Coordination of Tax Systems Commission has adopted a “Coordination package” (19 December 2006): • A Framework Communication explaining the content and scope of « coordination »: Commission Communication of 19.12.2006 (COM(2006) 823 final)Co-ordinating Member States' direct tax systems in the Internal Markethttp://ec.europa.eu/taxation_customs/resources/documents/taxation/COM (2006)823_en.pdf • A Communication applying the principle of coordination to exit taxes, notably on companies: Commission Communication of 19.12.2006 (COM(2006) 825 final) Exit taxation and the need for co-ordination of Member States' tax policieshttp://ec.europa.eu/taxation_customs/resources/documents/taxation/COM (2006)825_en.pdf • A Communication applying coordination to the tax treatment of cross border losses. Commission Communication of 19.12.2006 (COM(2006) 824 final)Tax Treatment of Losses in Cross-Border Situations of 19.12.2006http://ec.europa.eu/taxation_customs/resources/documents/taxation/COM (2006)824_en.pdf

The Scope of the Coordination of Tax Systems Commission has adopted a new Communication on 10 th December 2007: The application of anti-abuse measures in the area of direct taxation - within the EU and in relation to third countries (COM (2007) 785): • Doctrine of abuse of rights developed by the ECJ in its (mainly non-tax) case law, abuse occurs only where the purpose of law is defeated despite formal observance of the conditions laid down in the law, and there is an intention to obtain an advantage by artificially creating the conditions for obtaining it. • On direct taxation, ECJ has held that the need to prevent tax avoidance or abuse can constitute an overriding reason in the public interest capable of justifying a restriction on fundamental freedoms. However, notion of tax avoidance is limited to wholly artificial arrangements aimed at circumventing the application of the legislation of the MS concerned.

A Panel Discussion • Philip Kermode, Director of Tax Policies,European Commission: • Anti-abuse in a changing world: whatpolicy line for the EU? • Richard Lyal, Legal Advisor, European Commission: • Anti-abuse measures targeted to cross-border situations: EU compatible or not? • Frans Vanistendael, Academic Chairman, IBFD • Research and literature: what do they say ? How relevant are recent country specific developments? • Werner Stuffer, Partner, PricewaterhouseCoopers • Examples of recentdevelopments; bad or good?: CFC, Thin cap: