Download

1 / 143

1.43k likes | 1.59k Views

P a g e | 1 Internat i o n al As s o c ia t ion of R i s k a n d Co m p l ian ce Pr o f e s s iona l s ( I A RCP) 1200 G St r e et N W S u it e 8 0 0 Wa s h i n g t o n , D C 2000 5 - 6705 U S A T el: 202 - 44 9 - 9 750 w ww.ris k - c o m p l ia n c e - ass o c iat i on . c o m.

E N D

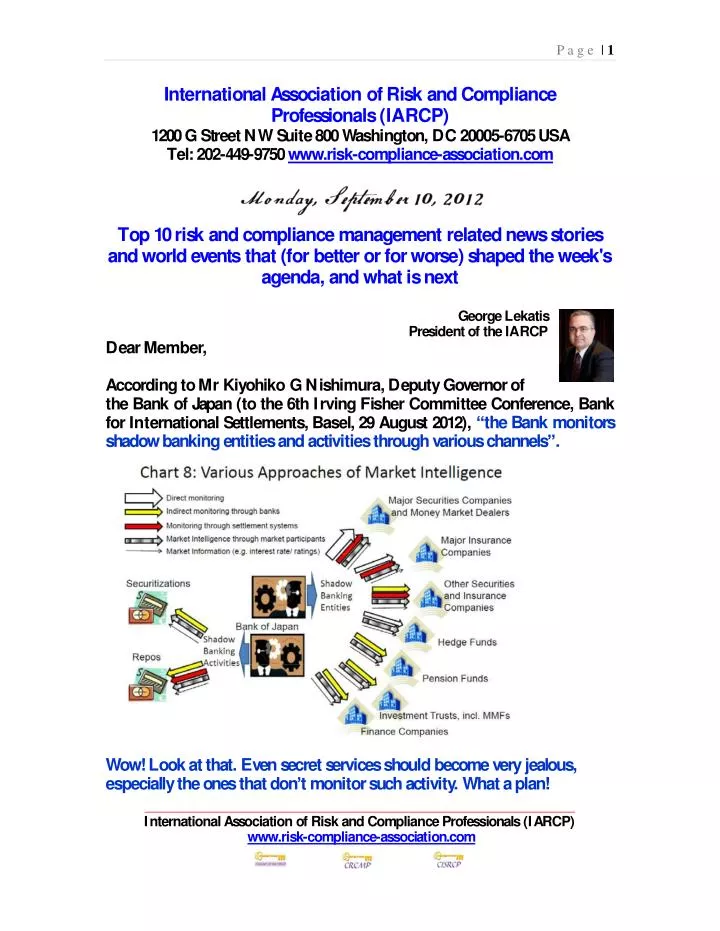

P age |1 InternationalAssociationofRiskandComplianceProfessionals(IARCP) 1200GStreetNWSuite800Washington,DC20005-6705USATel:202-449-9750www.risk-compliance-association.com Top10riskandcompliancemanagementrelatednewsstoriesandworldeventsthat(forbetterorforworse)shapedtheweek's agenda,andwhatisnext GeorgeLekatisPresidentoftheIARCP DearMember, AccordingtoMrKiyohikoGNishimura,DeputyGovernorof theBankofJapan(tothe6thIrvingFisherCommitteeConference,BankforInternationalSettlements,Basel,29August2012),“theBankmonitorsshadowbankingentitiesandactivitiesthroughvariouschannels”. Wow!Lookatthat.Evensecretservicesshouldbecomeveryjealous,especiallytheonesthatdon’tmonitorsuchactivity.Whataplan! InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |2 Hecontinues: “Amongstthesechannels,directmonitoringofmajorshadowbankingentitiesisofcoursethemostsignificant. Thus,thebankhasincreasedthenumberofstaffdirectlymonitoringmajorsecuritiescompanies. However,itispracticallyimpossibletoconductdialogueswithallfinancialinstitutionsofashadowbankingnature,andmoreover,shadowbankingactivitiestendtochangerapidlywithdevelopmentsinfinancialmarkets.” Itisaveryinterestingspeech. ReadmoreatNumber7B,justaftertheveryinterestingspeechofMrYoshihisaMorimoto,MemberofthePolicyBoardoftheBankofJapan. WelcometotheTop10list. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |3 SomeThoughtsonGlobalRisksandMonetaryPolicy CharlesL.Evans,PresidentandChiefExecutiveOfficer FederalReserveBankofChicago EBA,EIOPAandESMA JointConsultation PaperonDraftRegulatoryTechnicalStandardsontheuniformconditionsofapplicationofthecalculationmethodsunderArticle6.2oftheFinancialConglomeratesDirective(JC/CP/2012/02) CryptographicKeyManagementWorkshop2012 Purpose:NISTisconductingatwo-dayKeyManagementWorkshopon September10-11. ThesubjectoftheworkshopisthetechnicalandadministrativeaspectsofCryptographicKeyManagementSystems(CKMSs)thatcurrentlyexistandmayberequiredforU.S.Federaluseinthefuture. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |4 ShortSellingRegulationUpdateMarketMaker&PrimaryDealer ExemptionNotificationProcedure TheEuropeanSecuritiesandMarketsAuthority(ESMA)is publishingthisnoticetoalertfinancialmarketparticipantstoits upcomingconsultationonthemarketmakingandauthorisedprimarydealerexemptionundertheEU’sShortSellingRegulation(SSR)andthe proceduretobefollowedbyfirmsandregulatorsindealingwithnotificationsofintentiontousetheexemption. PreliminaryAnnualReportonU.S.HoldingsofForeignSecurities PreliminarydatafromanannualsurveyofU.S.portfolioholdingsof foreignsecuritiesat year-end2011werereleased. DrAndreasDombret,MemberoftheExecutiveBoardoftheDeutscheBundesbank Foreignbanksbetweenfinancialcrisisand financialstability InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |5 EconomicactivityandpricesinJapanandmonetarypolicy SpeechbyMrYoshihisaMorimoto,MemberofthePolicyBoardoftheBankofJapan,atameetingwith businessleaders,Ishikawa,2August2012. Marketintelligence,marketinformationandstatisticsincentralbanking KeynoteSpeechbyMrKiyohikoGNishimura,DeputyGovernoroftheBankofJapan,tothe6thIrvingFisherCommitteeConference,BankforInternationalSettlements,Basel,29August2012. NewsRelease-Thedogandthefrisbee–paperbyAndrewHaldane InapapergivenattheFederalReserveBankofKansasCity’s36theconomicpolicy symposiuminJacksonHole,Wyoming,AndrewHaldane–ExecutiveDirectorforFinancialStabilityandmemberoftheFinancialPolicyCommittee–exploreswhythetypeofcomplexfinancialregulation developedoverrecentdecadesmaybesub-optimalforcrisiscontrol InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |6 VIIAnnualSeminaronRisk,FinancialStabilityandBanking SãoPaulo Averyinterestingpresentation WhatcausedtheGlobalFinancialCrisis? CentralBankofIrelandPublishesJuly2012MoneyandBankingStatistics TheCentralBankofIrelandpublishedtheJuly2012MoneyandBankingStatistics Loansandothercredit InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |7 NUMBER1 SomeThoughtsonGlobalRisksandMonetaryPolicy CharlesL.Evans,PresidentandChiefExecutiveOfficer FederalReserveBankofChicago Introduction Thankyoufortheinvitationtospeaktoyoutoday.Iam veryhappyfortheopportunitytoparticipateinMarketNewsInternationalseminarandtooffermythoughtsontheU.S.andworldeconomies. Weliveinanamazinglyinterconnectedworld—aworldinwhich financialmarketsarelinkedbytheinstantaneoustransmissionofinformationandbusinessactivityisintertwinedamongnations. Foralongtime,U.S.consumersandfirmshavebeenanimportantsourceofdemandforAsianeconomies. Thiscomeswithplusesandminuses:Withouttherobustgrowthinthe U.S.in1997–98,theAsianfinancialcrisismaywellhavebeenmuchworsethanitactuallywas;incontrast,therecessionandsluggishgrowthinthe U.S.overthepastfiveyearshaveweighedheavilyonthedemandforproductsfromAsia. MycommentstodaywillfocusprimarilyontheoutlookfortheU.S.,butwithaneyeonitspotentialimpactonAsianeconomies. Ofcourse,hereIhavetocoverthesubstantialdownsideriskstotheforecaststemmingfromboththeEuropeandebtsituationandtheU.S.fiscalcliff. Iwillalsodiscusshowthisoutlookandothereconomicanalysesshapemyviewsfortheappropriatestanceofmonetarypolicy. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |8 BeforeIturntothefocusoftoday’sdiscussion,Iwouldliketoremindyouthattheviewsexpressedaremyownanddonotnecessarilyrepresent thoseoftheFederalOpenMarketCommittee(FOMC)ortheFederalReserveSystem. Outlook Let’sstartwiththeeconomicoutlook. Wearealltoofamiliarwiththefactthatthefinancialcrisisthatunfoldedin2007and2008precipitatedaglobalrecessionthatwasunusuallydeepandlengthyintheU.S.andotheradvancedeconomies. Perhapsthisshouldn’thavebeensurprising. ThedetailedanalysisbyCarmenReinhartandKennethRogoff(2009)concludesthatrecessionscausedbyfinancialcrisesgenerallyaresevereandarefollowedbyanemicrecoveries. Byanyyardstick,thiscertainlydescribestheU.S.recoverytodate: Outputgrowthhasaveragedonly2-1/4percentannually,andresourcegapsremainhuge. Inparticular,theunemploymentrateremainsover8percent—wellabovethe5-1/4to6percentratemostFOMCparticipantsviewasbeingconsistentwithafullyemployedlaborforceoverthelongerrun. Bothpublicandprivatesectorforecastsseerelativelymodestratesofgrowthoverthenextfewyears. Forexample,mostrecentforecastsbytheprivatesectorhave2012grossdomesticproduct(GDP)growthatlessthan2percent;apacethatmaynotevenbeenoughtokeepupwithpotential. Growthin2013isexpectedtobeonlymoderatelyhigher. Moreover,boththeEuropeandebtsituationandtheloomingU.S.fiscalcliffimpartsubstantialdownsideriskstotheforecast. Evenabsentanynegativeshocks,suchtepidgrowthrateswouldclosethelargeexistingresourcegapsonlyverygradually. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |9 Indeed,Iexpectthatwewillfaceunemploymentwellabovesustainablelevelsforsometimetocome. ImplicationsforAsia IntheaftermathoftheGreatRecession,mostAsianeconomiesenjoyedareturntosolidlevelsofgrowth. Today,however,growthinAsiafacessomenewchallenges. OneofthesechallengesisthatAsianeconomieswillnotbeimmunetothetepidgrowthprospectsfacingtheworld’sadvancedeconomies. ForecastsforgrowthinAsiahavebeenmarkeddownoverthepastyear, reflectinginparttheimpactofthedowngradeintheoutlookforAsian exportsfortheU.S.andtheeuroarea. Forexample,theU.S.andtheeuroareaaccountforaboutone-thirdofChina’smerchandiseexports. Therecessionandweakrecoveriesinthoseeconomieswerebigfactorsin theChinesecurrentaccountsurplusfallingfromabout10percentofGDPin2007tolessthan3percentin2011. Thisweaknessremainsaconsiderationaswelookforward;indeed,itisanimportantreasonwhytheInternationalMonetaryFund(IMF)isprojectingthattheChinesecurrentaccountsurpluswillfallevenmoreby2013. Internationaltradeisanexcellentthing:Exploitingcomparativeadvantagesraiseslivingstandardsforallnations. However,allcountriescan’tsimultaneouslyexporttheirwayoutoftheirproblems.Fortheworldasawhole,thecurrentaccounthastobalance. Thus,countrieswithlargeexternalsurplusesfaceriskstotheireconomiesposedbyslowdownsintheirtradingpartners. Aggregateworldgrowthmustreflectaggregateddomesticdemands.Soifdemandisgoingtobesluggishinalargeshareoftheworldeconomy, othernationsmusttakeuptheslack,orworldgrowthwillfall. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |10 Inflation Withregardtoinflation,asyouknow,theFOMC’slong-runinflationobjectiveis2percentasmeasuredbythepriceindexforpersonalconsumptionexpenditures(PCE). Foranumberofreasons,Idon’tforeseemuchriskthatinflationwillriseabovereasonabletolerancelevelsrelativetothisobjective. First,weseeevidenceoflowexpectationsforinflationandgrowthinthetoday’shistoricallylowTreasuryyields. Iftherewerewarningsignsofdangerousinflationarypressures,theten-yearratewouldn’tbeintheneighborhoodof1-3/4percent! Second,evenwiththelatestincreaseinoilprices,energyandcommoditypricesremainwellofftheirrecentpeaksastheglobaloutlookdims. Third,asIjustnoted,theoutputgapremainslargeandislikelytocloseonlyslowly. Inthiseconomicenvironment,wagepressuresarepracticallynonexistent. Anditishardtoenvisionhowmajorpersistentinflationpressureswillemergewithoutaparallelincreaseinwagecosts.Suchparallelpriceandwageincreaseswereabigpartofthe1970sinflation,ascenariosomefear repeatingtoday. Fourth,inflationarydynamicsdependinlargepartonthemomentumgeneratedbypeople’sexpectationsoffutureinflation;currently,inflationexpectationsarewellanchored,whichwilltendtokeepinflationfrom movingeitherupordown. Puttingallofthesefactorstogetheralongwiththefactthatcoreinflationaveraged1.8percentoverthepastyear,Iconcludethatinflationwilllikely remainnearorbelowour2percenttargetoverthemediumterm. SourcesofRiskandTheirImplications Iwouldnowliketoturntotwoimportantdownsideriskstotheoutlookforgrowth. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |11 ThiswillbeabitofaU.S.-centricview,butclearlytheserisksalsohaveimportantimplicationsforgrowthhereinAsiaandtherestoftheworld. Europe LetmebeginwiththeEuropeandebtsituation. Obviously,thedevelopmentsinEuropeposeasignificantdownsiderisktotheU.S.economyandworldeconomicgrowthmorebroadly. ThedirecteffectsofslowerEuropeangrowthontheU.S.economywould berelativelysmall. Theeurozonenationsaccountforlessthan15percentofU.S.merchandiseexports. Thus,accordingtostandardelasticityestimates,evenamoderate eurozonerecessionwouldreduceU.S.exportsbyonlyacoupleoftenthsofGDP. Theindirecteffectsofeurozonedevelopmentscould,however,bemoresevere,bothintheU.S.andAsia.Onepossiblechannelwouldbethrough financialcontagion. Iflossesoneuro-centricassetsputalargeenoughdentinthebalancesheetsoffinancialinstitutionsthatlendtoU.S.householdsand businesses,theincreasesinthecostandavailabilityofcreditwouldreducegrowthintheU.S.withpossiblespillovereffectsintoAsiaaswell.Clearly,thisisariskworthmonitoring. Fortunately,though,U.S.financialinstitutionsareinmuchbettershapetohandlesuchpotentiallossesthantheywerein2008. RecognizingtherisksposedbytheEuropeandebtsituation,U.S.institutionshavereducedtheirdirectexposuretoEuropeanassetsandtightenedlendingstandardstoEuropeanbanks. Ontheregulatoryfront,themostrecentstresstestsmadelargeU.S.banksdemonstratethattheywouldhaveadequatecapitalevenintheeventofasharpEuropeanrecessionwithcontagiontoglobalfinancialmarkets. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |12 Asecondpossiblechannelwouldbethroughtheeffectsofuncertaintyoncurrentdemand. Throughouttherecovery,U.S.businessandhouseholdsentimenthasbeenveryfragile. Everyhintofbadnewsseemstogenerateawaveofincreasedcautionandanassociatedpullbackinspendingasfirmsandfamiliesseektoprotect theirindividualbalancesheets. AfterwhattheU.S.economywentthroughintheGreatRecession,thisskittishnessisunderstandable—particularlyifonecanenvisionaverylargedownsidetothenewsevent. And,asIjustnoted,givendevelopmentsinEurope,therecertainlyaresomeseriousdownsidescenariosonecanenvision,eveniftheyarenot themostlikelyoutcomes. Soitwouldbenosurpriseifyetanotherwaveofuncertaintyputafurtherdentinconsumptionandinvestment. U.S.fiscalcliff AnotherrisktotheU.S.economycomesfromtheso-calledfiscalcliff.UndercurrentU.S.law,numeroustaxandspendingprovisionsenactedin variousstimuluspackagesdatingasfarbackas2001arescheduledto expireonJanuary1,2013. Inaddition,ifnobudgetagreementisreachedbyCongress,therewillbesignificantautomaticspendingsequestrationandotherspendingcutsinJanuary. AccordingtoprojectionsmadebytheCongressionalBudgetOffice(CBO),ifallthesethingstookplace,realGDPgrowthwouldbereduced byabout4percentagepointsin2013. I’mnotsayingthatapullbackofthismagnitudeshouldbethebase-casescenario. Theordersofmagnitudearejusttoobigtobeabasecase. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |13 Butwhenyougothroughthevariousitemsandmakeguessesatwhichmaystayandwhichmaygo,itiseasytoenvisionscenariosthatincludeamarkedincreaseinfiscalrestraintin2013. Inaddition,giventhepoliticalprocess,itseemsunlikelythatwewillknowmuchaboutthesizeorcompositionofthecutsuntillateintheprocess. It’salsoeasytoseehowtherhetoricofpublicnegotiatingstancescouldproduceanatmospherethatcausesalreadyjitteryhouseholdsandbusinessestoputsomespendingplansonhold. Insum,amessyresolutiontothefiscalcliffproblemspresentsanimportantdownsiderisktoU.S.growthprospectsand,byextension,toworldeconomicgrowth. Andeventhepossibilityofsuchanoutcomecouldbeadraginthesecond halfoftheyear. PolicyChoices LetmenowswitchgearsandtalkaboutmyviewsregardingthechoicesfacingmonetarypolicymakersintheU.S. Yes,wehavesubstantialliquidityalreadyinplaceinourfinancialsystem.Onthesurface,thislookslikesubstantialmonetaryaccommodation. Butasalargebodyofeconomictheorytellsus,forthisliquiditytobesufficientlyaccommodative,thepublicneedstoexpectthatwewillkeepitinplaceforaslongasisnecessarytorestoretheeconomytoasoundfooting. ThisiswhyIbelieveweshouldclarifytheFed’sforwardguidancewithregardtothefuturecourseofpolicy.Letmenowgointothedetailsbehindthesethoughts. Anexpliciteconomicstate-contingentpolicy Inweighingalternativepolicyapproaches,Ithinkthebestwaytoprovideforwardguidanceisbytyingourpolicyactionstoexplicitmeasuresofeconomicperformance. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |14 Therearemanywaysofdoingthis,includingsettingatargetforthelevel ofnominalGDP. Butrecognizingthedifficultnatureofthatpolicyapproach,Ihaveamoremodestproposal:IthinktheFedshouldmakeitclearthatthefederalfundsratewillnotbeincreaseduntiltheunemploymentratefallsbelow7percent. KnowingthatrateswouldstaylowuntilsignificantprogressismadeinreducingunemploymentwouldreassuremarketsandthepublicthattheFedwouldnotprematurelyreduceitsaccommodation. BasedontheworkIhaveseen,Idonotexpectthatsuchpolicywouldleadtoamajorproblemwithinflation. ButIrecognizethatthereisachancethatthemodelsandotheranalysissupportingthisapproachcouldbewrong. Accordingly,Ibelievethatthecommitmenttolowratesshouldbedroppediftheoutlookforinflationoverthemediumtermrisesabove3percent. Theeconomicconditionalityinthis7/3thresholdpolicywouldclarifyourforwardpolicyintentionsgreatlyandprovideamoremeaningfulguideon howlongthefederalfundsratewillremainlow. Inaddition,Iwouldindicatethatclearandsteadyprogresstowardstrongergrowthisessential. Becausewearenotseeingthatnow,Isupportfurtheruseofourbalancesheettoprovideevenmoremonetaryaccommodation. InJunewedecidedtocontinueourMaturityExtensionProgram,whichputsdownwardpressureonlong-terminterestratesbyextendingtheaveragematurityoftheFederalReserve’ssecuritiesportfolio. Ithoughtthatwasausefulstep. However,Ibelieveitistimetotakeevenstrongersteps,suchasthepurchaseofmoremortgage-backedsecurities,toincreasethedegreeofmonetarysupportfortherecovery. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |15 AssuggestedrecentlybymycolleaguesEricRosengrenandJohnWilliams,thesecouldbeopen-endedpurchases,meaningthattheywouldcontinueatacertainrateuntiltherewasclearevidenceofimprovementineconomicconditions. Tome,oneexampleofclearevidencewouldbearesumptionofrelativelysteadymonthlydeclinesinunemploymentfortwoorthreequarters. Oncethismomentumwasconfidentlyestablished,theFedcouldstopaddingtoourbalancesheetbutkeepthefundsrateatzero. Thefundsratewouldremainunchangedinmythinking,untiltheunemploymentratehitatleast7percentorthemedium-terminflationoutlookdeteriorateddramaticallyandroseabove3percent. Later,reductionsintheFed’sbalancesheetassetswouldoccursometimeafterthefirstincreaseinthefundsrate. ThiscorrespondstothegeneralexitprinciplestheFOMCagreeduponlastyear. Presumably,thepaceofassetreductionswouldbemeasuredandconsistentwithacontinued,robustrecoveryinthecontextofpricestability. AccommodationintheContextofaSymmetricInflationTargetandBalancedPolicy Ican’ttellyouhowoftenpeoplelookatmeinhorrorwhenIsaythatweshouldadoptaconditionalpolicythattoleratestheriskofinflationexceedingourtargetbyasmuchas1percentagepoint. HowcanIacceptinflationrisingaboveourstatedtarget?Isn’tthisblasphemyforacentralbanker? InJanuary,inthesameframeworkdocumentthatannouncedour2percentinflationtarget,wealsostatedanumberofprinciplesfortheconductofmonetarypolicy. OnewasthatpolicywouldtakeabalancedapproachinachievingthetwolegsoftheFederalReserve’sdualmandate—maximumemploymentandpricestability. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |16 Anexplicitreal-sidemandatemakestheFederalReservedifferentthanmostcentralbanks. Whilejustaboutallcentralbanksfollowaflexibleinflationtargeting approach,inwhichtheyseektominimizereal-sidefluctuationsinpursuitoftheirinflationobjective,mostareexplicitlychargedonlywithaninflationobjective. ButfortheFed,maximumemploymentisanexplicitpartofourpolicymandate. IstronglysupportthepolicyprinciplesdocumentwereleasedinJanuary.Butwe’restillhearingquestionsaboutwhetherourinflationgoalissymmetricandaboutthespecificsofhowpolicywillbeimplemented underthebalancedapproacharticulatedinthisframework. AsChairmanBernanke(2012)statedathisAprilpressconference,the2percentinflationgoalisasymmetricobjectiveandnotaceilingoninflation. Symmetrymeansthatinflationbelow2percentshouldbeviewedasthesamepolicymissasifinflationoverran2percentbyequalamount. Weneedtotakesymmetryseriously. Ifwedisproportionatelyrecoilatinflationalittleabove2percentversusalittlebelow,thenwearenotsymmetricallyweighingpolicymisses. Andwewillnotaverage2percentinflation,whichisourgoal. Thereissomeriskofthismisperceptiontakinghold.ConsidertheFOMC’slatestSummaryofEconomicProjections(SEP),whichincludestheprojectionsofallFOMCparticipants,votersandnon-votersalike. Init,severalforecastshavethefundsraterisingbefore2014,eventhoughthroughouttheprojectionperiodmostseeinflationatorbelow2percentandunemploymentwellabovethesustainablerateindicatedbythe long-runprojections. Withoutfurtherexplanation,it’sdifficulttoseehowthisisconsistentwithasymmetricinflationgoalandabalancedapproachtoachievingthetwolegsinourdualmandate. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |17 IbelievetheFOMCcandobetteratdescribingourthinkingwithrespect totolerancebandsaroundourlong-runinflationandunemploymentgoals. Clarificationwouldincreasebothtransparencyandaccountability. Importantly,itwouldreassureeconomicagentsthatFedpolicywouldnottightenprematurely. Tome,asymmetricinflationgoalandabalancedapproachtopolicymeanthatifwearemissingouremploymentmandatebyalargeamount,butareclosetoourinflationtarget,thenweshouldbewillingtoundertakepoliciesthatcouldsubstantiallyreducetheemploymentgapeveniftheyruntheriskofamodest,transitoryriseininflationthatremainswithinareasonabletolerancerangeofourtarget. Ibelievesuchactions,suchasthe7/3thresholdpolicyIhavebeenadvocating,wouldproducesmallernetlossesrelativetoourdualmandategoalsthanwouldcurrentpolicy. Conclusion:TheNeedforaVibrantEconomytoCushionRisks Findingawaytodelivermoreaccommodation—whetheritismonetary orfiscal—isparticularlyimportantnowbecausedelaysinreducingunemploymentarecostly. Anunusuallylargepercentageoftheunemployedhavebeenwithoutworkforquiteanextendedperiodoftime;theirskillscanbecomelesscurrentorevendeteriorate,leavingaffectedworkerswithpermanentscarsontheirlifetimeearnings. Andanyresultingloweraggregateproductivityalsoweighsonpotentialoutput,wagesandprofitsfortheeconomyasawhole. Thedamageintensifiesthelongerthatunemploymentremainshigh.Failuretoactaggressivelynowcouldlowerthecapacityoftheeconomy formanyyearstocome. Suchpotentialcostswouldcomewiththecontinuationofasubparpaceofeconomicrecovery. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |18 ThesignificantrisksIdiscussedearlier–financialdisruptionfromaworseningofthesituationinEuropeoramessyresolutionofU.S.fiscalpolicy–raisethespecterofanevenmoreworrisomeoutcome. Atthemomenteconomicgrowthisnotmuchabovestallspeed.Anothernegativeshockcouldsendtheeconomyintorecession. Andifarecessionarydynamictakeshold,itwouldbeespeciallydifficult toregainmomentum. IhaveoutlinedsomepolicyactionsthatIthinkcantakeusinthedirectionofamorevibrantandresilienteconomy. Giventherisksweface,Ithinkitisvitalthatwemakesuchmovestoday.Idon’tthinkweshouldbeinamodewherewearewaitingtoseewhatthenextfewdatareleasesbring. Wearewellpastthethresholdforadditionalaction;weshouldtakethatactionnow. Thankyou. Note CharlesL.EvansistheninthpresidentandchiefexecutiveofficeroftheFederalReserveBankofChicago.Inthatcapacity,heservesontheFederalOpenMarketCommittee(FOMC),theFederalReserveSystem'smonetarypolicy-makingbody. TheFederalReserveBankofChicagoisoneof12regionalReserveBanksacrossthecountry.These12banks—alongwiththeBoardofGovernorsinWashington,D.C.—makeupournation'scentralbank. AsheadoftheChicagoFed,Evansoverseestheworkofroughly1400employeesinChicagoandDetroitwhoconducteconomicresearch,supervisefinancialinstitutions,andprovidepaymentservicestocommercialbanksandtheU.S.government. BeforebecomingpresidentinSeptemberof2007,Evansservedasdirectorofresearchandseniorvicepresident,supervisingtheBank'sresearchonmonetarypolicy,banking,financialmarketsandregional InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |19 economicconditions.Priortothat,Evanswasavicepresidentandsenior economistwithresponsibilityforthemacroeconomicsresearchgroup. HispersonalresearchhasfocusedonmeasuringtheeffectsofmonetarypolicyonU.S.economicactivity,inflationandfinancialmarketprices.IthasbeenpublishedintheJournalofPoliticalEconomy,AmericanEconomicReview,JournalofMonetaryEconomics,QuarterlyJournalofEconomics,andtheHandbookofMacroeconomics. Evansisactiveintheciviccommunity.HeisaboardmemberatChicagoMetropolis2020andtheMetroChicagoInformationCenter,andatrusteeatRushUniversityMedicalCenter. EvanshastaughtattheUniversityofChicago,theUniversityofMichiganandtheUniversityofSouthCarolina.Hereceivedabachelor'sdegreeineconomicsfromtheUniversityofVirginiaandadoctorateineconomicsfromCarnegie-MellonUniversityinPittsburgh. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |20 NUMBER2 • EBA,EIOPAandESMA • JointConsultationPaperonDraftRegulatoryTechnicalStandardsontheuniformconditionsofapplicationofthecalculationmethodsunderArticle6.2oftheFinancialConglomeratesDirective(JC/CP/2012/02) • RespondingtothisConsultation • EBA,EIOPAandESMA(theESAs)invitecommentsonallmattersinthispaperandinparticularonthespecificquestionsstatedintheattacheddocument“OverviewofquestionsforConsultation”attheendofthispaper. • Commentsaremosthelpfulifthey: • respondtothequestionstated; • indicatethespecificquestiontowhichthecommentrelates; • containaclearrationale; • provideevidencetosupporttheviewsexpressed/rationaleproposed;and • describeanyalternativeregulatorychoicesEBAshouldconsider. • ExecutiveSummary • TheCRR/CRDIVproposals(theso-calledCapitalRequirementsRegulation-henceforth‘CRR’-andtheso-calledCapitalRequirements InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |21 Directive–henceforth‘CRD’)setoutprudentialrequirementsforbanksandotherfinancialinstitutionswhichareexpectedtoapplyfrom1January2013. InanticipationofthefinalisationofthelegislativetextsfortheCRR/CRDIV,theEBA,EIOPAandESMA(hereaftertheESAs)throughtheJointCommittee,havedevelopedthedraftRTSinaccordancewiththemandatecontainedinArticle46(4)oftheCRRandArticle139ofCRDIV(amendingArticle21a(2a)oftheDirective2002/87/EC)onthebasisoftheEuropeanCommission’sproposals. ThisArticleprovidestheESAsthroughtheJointCommittee,todevelop draftRegulatoryTechnicalStandards(RTS)withregardtotheconditionsoftheapplicationoftheArticle6(2)oftheDirective2002/87/EC(hereaftertheDirective). FurthertheESAshavedevelopedthedraftRTShavingregardtoArticle230inconnectionwithArticles220and228oftheDirective 2009/138/EC2. Totheextentthatthetextsmaychangebeforetheiradoption,theESAsshalladaptitsdraftRTSaccordinglytoreflectanydevelopments. TheRTSincludedinthisconsultationhavetobesubmittedtotheEUCommissionby1January2013. PleasenotethattheESAshavedevelopedthepresentdraftRTSbasedontheEuropeanCommission’slegislativeproposalsfortheCRR/CRDIV. Theyhavealsotakenintoaccountmajorchangessubsequentlyproposed bytherevisedtextsproducedbytheCounciloftheEUandtheEuropean Parliament,duringtheordinarylegislativeprocedure(co-decision process). Followingtheendoftheconsultationperiod,andtotheextentthatthefinaltextoftheCRR/CRDIVchangesbeforetheadoptionoftheRTS,theESAswilladaptthedraftRTSaccordinglytoreflectanydevelopments. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |22 MainfeaturesoftheRTS ThisconsultationpaperputsforwarddraftRTSinordertoensurethat institutionsthatarepartofafinancialconglomerateapplytheappropriatecalculationmethodsforthedeterminationofrequiredcapitalatthelevel oftheconglomerate. Theyarebasedinparticularonthefollowingelements: GeneralPrinciples oEliminationofmultiplegearing; oEliminationofintra-groupcreationofownfunds;oTransferabilityandavailabilityofownfunds;and oCoverageofdeficitatfinancialconglomeratelevelhavingregardtodefinitionofcross-sectorcapital. Technicalcalculationmethods 1.Method1:“Accountingconsolidationmethod”: TheFICODprovidesinrelationtoMethod1thattheownfundsarecalculatedonthebasisoftheconsolidatedpositionofthegroup. Accordingtothisgeneralprovision,thecalculationofownfundsshould bebasedontherelevantaccountingframeworkfortheconsolidated accountsoftheconglomerateapplicabletothescopeoftheDirective. Theuseof“consolidatedaccounts”eliminatesallownfunds’intra-groupitems,inordertoavoiddoublecountingofcapitalinstruments. AccordingtotheDirectiveprovisions,theeligibilityrulesarethoseincludedinsectoralprovisions. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |23 Method2:“Deductionandaggregationmethod”. Thismethodcalculatesthesupplementarycapitaladequacyrequirementsofaconglomeratebasedontheaccountsofsoloentities. Itaggregatestheownfunds,deductsthebookvalueoftheparticipationsinotherentitiesofthegroupandspecifiestreatmentoftheproportionalshareapplicabletoownfundsandsolvencyrequirements. Allintra-groupcreationofownfundsshallbeeliminated. Method3:“Combinationofmethods1and2”. Theuseofcombinationofaccountingconsolidationmethod1and deductionandaggregationmethod2islimitedtothecaseswheretheuseofeithermethod1ormethod2wouldnotbeappropriateandissubjecttothepermissionbythecompetentauthorities. III.Backgroundandrationale ThesupplementarysupervisionoffinancialentitiesinafinancialconglomerateiscoveredbytheFinancialConglomeratesDirective2002/87/EC,hereafterknownastheDirective. ThisDirectiveprovidesforcompetentauthoritiestobeabletoassessatagroup-widelevelthefinancialsituationofcreditinstitutions,insuranceundertakingsandinvestmentfirmswhicharepartofafinancialconglomerate,inparticularasregardssolvency(includingtheeliminationofmultiplegearingofownfundsinstruments). ThenatureofRTSunderEUlaw DraftRTSareproducedinaccordancewithArticle10oftheESAsregulation. AccordingtoArticle10(4)oftheESAsregulation,theyshallbeadopted bymeansofRegulationsorDecisions. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |24 AccordingtoEUlaw,EUregulationsarebindingintheirentiretyanddirectlyapplicableinallMemberStates. Thismeansthat,onthedateoftheirentryintoforce,theybecomepartofthenationallawoftheMemberStatesandthattheirimplementationintonationallawisnotonlyunnecessarybutalsoprohibitedbyEUlaw,exceptinsofarasthisisexpresslyrequiredbythem. ShapingtheserulesintheformofaRegulationwouldensurealevel-playingfieldandwouldfacilitatethecross-borderprovisionofservices. BackgroundandregulatoryapproachfollowedinthedraftRTS ThesedraftRTSareproducedinaccordancewithCRDIV/CRRproposals,whichprovidethattheEBA,ESMAandEIOPA(hereaftertheESAs),throughtheJointCommittee,shalldevelopdraftregulatorytechnicalstandardswithregardtotheconditionsoftheapplicationofthecalculationmethodswithregardtoArticle6(2)oftheDirectiveandshallsubmitthosedraftregulatorytechnicalstandardstotheCommissionby1January2013. TheproposeddraftRTScoverstheuniformconditionsfortheuseofthemethodsforthedeterminationofcapitaladequacyofafinancialconglomerateundertheDirective. TheyelaborateonTechnicalprinciplesapplyingtoallofthethreemethodsprovidedforbyDirective;andalsocontainanAnnexprovidingfurtherdetailforMethod2. TherequirementscontainedinthedraftRTSaremainlydirectedatinstitutions,althoughsomeofthemaredirectedatcompetentauthorities. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |25 IV.DraftRegulatoryTechnicalStandardsontheuniformconditionsofapplicationofthecalculationmethodsunderArticle6.2oftheFinancialConglomeratesDirective CommissionDelegatedRegulation(EU)NoXX/2012 supplementingDirectivexx/XX/EU[CRD]oftheEuropeanParliamentandoftheCouncilof[date],Regulation(..)Noxx/XXXX[CRR]ofthe EuropeanParliamentandoftheCouncilof[date]andDirective 2002/87/EC[FinancialConglomeratesDirective]oftheEuropean ParliamentandoftheCouncilof[date]withregardtoregulatory technicalstandardsfortheuniformconditionsofapplicationofthecalculationmethodsunderArticle6.2oftheFinancialConglomerates DirectiveofXXMonth2012 THEEUROPEANCOMMISSION, HavingregardtotheTreatyontheFunctioningoftheEuropeanUnion,Havingregardtothe[proposalfora]Regulation(...)Noxx/xxxxofthe EuropeanParliamentandoftheCouncilofddmmyyyyonprudential requirementsforcreditinstitutionsandinvestmentfirmsRegulation xx/xxxx[CRR]andinparticularArticle46(4)thereof. Havingregardtothe[proposalfora]Directive(...)Noxx/xxxxoftheEuropeanParliamentandoftheCouncilofddmmyyyyontheaccesstotheactivityofcreditinstitutionsandtheprudentialsupervisionofcreditinstitutionsandinvestmentfirms[CRDIV]andinparticularArticle139thereof. HavingregardtotheDirective2002/87/EC,asamended,oftheEuropeanParliamentandoftheCouncilonthesupplementarysupervisionofcreditinstitutions,insuranceundertakingsandinvestmentfirmsinafinancialconglomerate(hereinafter“theDirective”)andinparticulartoArticle6(2)andAnnex1thereof. Whereas: InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |26 Directive2002/87/ECprovidesinChapterII,Section2,rulesoncapitaladequacyoffinancialconglomerates,suchthattheelementsofownfundsareavailableatthelevelofaFinancialConglomeratesarealwaysatleastequaltothecapitaladequacyrequirementsascalculatedinaccordancewithAnnexIoftheDirective. Regulation(...)Noxx/xxx(‘CRR’)providesinArticle46,withinPartII,Chapter2,Section3,Sub-Section2andinthecontextofcommonequity TierIrules,requirementsfordeductionwhereconsolidationorsupplementarysupervisionareapplied. ThissectionoftheCRRprovidesempowermentstotheEuropeanCommissiontoadoptdelegatedacts(regulatorytechnicalstandards)inaccordancewitharticles10-14oftheRegulation(EU)No1093/2010establishingtheEuropeanBankingAuthority(‘EBA’),Articles10-14oftheRegulation(EU)No1094/2010establishingtheEuropeanInsuranceandOccupationalPensionsAuthority(‘EIOPA),andArticles10-14oftheRegulation(EU)No1095/2010(‘ESMA),establishingtheEuropeanSecuritiesandMarketsAuthority. TheseactswillcompletetheEUsinglerulebookforinstitutionsintheareaofownfunds. Directive(...)Noxx/xxx(‘CRDIV’)providesinArticle139thattheDirective2002/87/ECshallbeamended,suchthattheEBA,EIOPAandESMAthroughtheJointCommittee,todevelopdraftRegulatoryTechnicalStandards(RTS)withregardtotheconditionsoftheapplicationoftheArticle6(2)oftheDirective. ForeffectivesupervisionofFinancialConglomerates,supplementarysupervisionshouldbeappliedtoallsuchconglomerates,the cross-sectoralfinancialactivitiesofwhicharesignificant,whichisthe casewhencertainthresholdsarereached,nomatterhowtheyarestructured. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |27 Supplementarysupervisionshouldcoverallfinancialactivitiesidentifiedbythesectoralfinanciallegislationandallentitiesprincipallyengagedinsuchactivitiesshouldbeincludedinthescopeofthesupplementarysupervision,includingassetmanagementcompaniesandalternativeinvestmentfundmanagementcompanies. Withoutprejudicetosectoralrules,supplementarysupervisionofthecapitaladequacyrulesisnecessarytobringmoreconvergenceintheapplicationofthecalculationmethodslistedinAnnex1oftheDirective. Forfinancialconglomerateswhichincludesignificantbankingorinvestmentbusinessandinsurancebusiness,multipleuseofelementseligibleforthecalculationofownfundsatthelevelofthefinancialconglomerate(multiplegearing)aswellasanyinappropriateintra-groupcreationofownfundsmustbeeliminated. Thefinancialconglomerateshouldseekanacceptabletimeframeforthetransferabilityoffundsacrossentitieswithinthefinancialconglomerate,whichshalldependonwhetherthespecificentityis subjecttotheDirective2009/138/ECortheCRDIV/CRR. MoreoverforanentitysubjecttotheCRDIV/CRRthistimeframeshould beexpediatedbasedonthefactthatduetothenatureoftheiractivities,theyaremorevulnerabletoarapiddeteriorationinconfidenceand/orsuddenresolutionsituation. Inadditionanynon-sector-specificownfunds,inexcessofsectoralrequirements,needtooriginatefromentitieswhicharenotsubjecttotransferability/availabilityimpediments. Itisimportanttoensurethatownfundsareonlyincludedatconglomerateleveliftherearenoimpedimentstothetransferofassetsorrepaymentofliabilitiesacrossdifferentconglomerateentities,includingacrosssectors. Ifthereisadeficitofownfundsatthelevelofthefinancialconglomerate,thefinancialconglomerateshouldinformthecoordinatoronthemeasurestakentocoverthisdeficit. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |28 Furtherconvergenceinthewaythatfinancialconglomeratesapplytheserulesshallensuretherobustandconsistentapplicationofthemethodsofcalculation. Forbank-ledconglomeratesitisnecessarytoapplythemostprudentmethodofcalculationforthetreatmentofinsuranceholdingstoavoidregulatoryarbitrage. Itisimportantthatsector-specificownfundscannotcoverrisksabovesectoralrequirements. Thefinancialconglomerateshouldfirstcountsector-specificownfundsagainsttheirrequirements(whilerespectingsectoralrulesandlimits)foreachrelevantentityorgroupofentities.Ifthereisanexcessof sector-specificownfunds,thisshouldnotberecognisedatconglomeratelevel. Whencalculatingsupplementarycapitaladequacyofafinancialconglomerate,inrespecttonon-regulatedfinancialentitieswithinthefinancialconglomerate,bothanotionalcapitalrequirementandanotionallevelofownfundsshoudbecalculated. UnderSolvencyII,method1isappliedonthebasisofconsolidateddatawhicharesetoutatLevel2andnotonthebasisofconsolidated accounts. FurtherchangestothecapitaladequacyrulesmaybeaddressedintheEuropeanCommission’sreviewofDirective2002/87/EC. ItisnecessarythatthenewregimefortreatmentofmethodsofconsolidationentersintoforcethesoonestpossiblefollowingtheentryintoforceoftheCRR/CRDIVandSolvencyII. ThisRegulationisbasedonthedraftregulatorytechnicalstandardssubmittedjointlybytheEBA,EIOPAandESMAtotheCommission. TheEBA,EIOPAandESMAhaveconductedopenpublicconsultationsonthedraftregulatorytechnicalstandardsonwhichthis InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |29 Regulationisbased,analysedthepotentialrelatedcostsandbenefits,inaccordancewithArticle10ofRegulation(EU)No1093/2010,Article10ofRegulation(EU)No1094/2010,Article10ofRegulation(EU)No1095/2010,andrequestedtheopinionoftheBankingStakeholderGroupestablishedinaccordancewithArticle37ofRegulation(EU)No1093/2010,InsuranceStakeholderGroupandtheOccupationalStakeholderGroupestablishedinaccordancewithArticle37ofRegulation(EU)No1094/2010,andtheEuropeanSecuritiesandMarketsStakeholderGroupestablishedinaccordancewithArticle37ofRegulation(EU)No1095/2010. HASADOPTEDTHISREGULATION: TITLEI Subjectmatteranddefinitions Article1Subjectmatter ThisRegulationlaysdownrulesoftheuniformconditionsofapplicationofthecalculationmethodsunderArticle6.2oftheDirective. Article2Definitions DefinitionsoftheCRDIV/CRR,Directive2002/87/ECandDirective 2009/138/ECshallapplytothisRegulation. CapitalinstrumentsarethosecapitalinstrumentseligibleunderCRR(Regulation2012/…./EC)andthosecapitalinstrumentsreferredtoas“ownfunds”inDirective2009/138/EC. Ultimateresponsibleentityistheentitywithinthefinancialconglomeratethatisresponsiblefordeterminingthecapitalforthefinancialconglomeratehavingregardtothefollowingminimumcriteria:control,thedominantentityfromthemarket’sperspective(marketlisted InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |30 entity)andtheabilitytofulfillspecificdutiestowardsitssubsidiariesanditssupervisor. ‘indirectholding’asdefinedunderdefinition17ofArticle22ofCRR[tobeaddedifnotinfinalCRRtext]. Insurance-ledfinancialconglomerateisafinancialconglomeratewhosemostimportantsectorisinsuranceasdefinedunderArticle3(2)oftheDirective. Bank-ledfinancialconglomerateisafinancialconglomeratewhosemostimportantsectorisbankingasdefinedunderArticle3(2)oftheDirective. Investmentfirm-ledfinancialconglomerateisafinancialconglomeratewhosemostimportantsectorisinvestmentservicesasdefinedunderArticle3(2)oftheDirective. TITLEII TechnicalPrinciples Article3 Eliminationofmultiplegearingandtheintra-groupcreationofownfunds Theultimateresponsibleentityshallensurethatownfunds,whichhavebeencreatedbyintra-grouptransactions,beitdirectorindirect,shallbeeliminatedforthepurposeofdeterminingtherequiredcapitalona consolidatedbasis. Article4 Transferabilityandavailabilityofownfunds 1.Forallentitiesofafinancialconglomerate,ownfunds,inexcessofsectoralsolvencyrequirements,shallbeconsideredavailabletoabsorblosseselsewhereinthefinancialconglomerateprovidedthatallofthefollowingconditionsarefulfilled: InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |31 Therearenopractical,legal,regulatory,contractualorstatutoryimpedimentstothetransferoffundsorrepaymentofliabilitiesacrossconglomerateentitiesinduecourse. Thisisthecasewhenthetransferofownfundsfromoneconglomerate entitytoanotherisnotbarredbyarestrictionofanykindandtherearenoclaimsofanykindfromthirdpartiesontheseassets. Theultimateresponsibleentityofthefinancialconglomerateshallconfirmtothesatisfactionofthecoordinatorthattheconditionssetoutinthispointaremet. Forthepurposeofassessingthetransferabilityoffundstoentitiessubjectto2009/138/EC,“induecourse”shallmeannolaterthan9months; forthepurposeofassessingthetransferabilityoffundstoentitiessubjectedtoCRR,“induecourse”shallmeannolaterthan,threecalendardayswithnoimpedimentsonthecoordinatorrequiringafastertransferifnecessary. Ownfunds,inexcessofsectoralsolvencyrequirements,whichdonotmeetthecriteriaunderpoint1shallbeexcludedfromtheconglomerate’sownfunds. Thefinancialconglomerateshalldemonstratethatmeasureshavebeentakentomitigatetheriskthattransferoffundswouldhaveamaterialeffectonthetransferor’ssolvency. EXPLANATORYTEXTforconsultationpurposes ThistextisconsistentwithAnnex1oftheDirectivewhichstates“whencalculatingownfundsatthelevelofthefinancialconglomerate,competentauthoritiesshallalsotakeintoaccounttheeffectivenessofthetransferabilityandavailabilityoftheownfundsacrossthedifferentlegal entitiesinthegroup,giventheobjectivesofthecapitaladequacyrules”. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |32 Point1(a)aimstoensurethatownfundsareonlyincludedatconglomerateleveliftherearenotimpedimentstothetransferofassetsor repaymentofliabilitiesacrossdifferentconglomerateentities,includingacrosssectors. Iftheconglomeratecannotconfirmtothesatisfactionofthecoordinatorthattherearenoinherentimpedimentsinrelationtoagivenentity,thatentity’sownfundsinexcessofitssectoralrequirementscannotbeincludedatconglomeratelevel. Theimpedimentstobeconsideredincludepractical,regulatory,contractualorstatutoryones. Point1(b)establishesanacceptabletimeframeforthetransferabilityoffundsacrossconglomerateentities. ThereisadifferentiationbasedonthefactthatentitiessubjecttoCRR,duetothenatureoftheiractivities,aremorevulnerabletoarapiddeteriorationinconfidenceand/orsuddenresolutionsituation. Article5 Deficitofownfundsatthefinancialconglomeratelevel Whenthedifferencecalculatedaccordingtomethod1,2or3asdetailedinAnnex1oftheDirectiveisnegative,thefinancialconglomerateshallensurethatthedeficitisremediedwithcross-sectorownfundselementsasdefinedinpoint2below. Whencalculatingownfundsatthelevelofthefinancialconglomerate,crosssectorownfundsareelementseligiblefor: CommonEquityTier1inaccordancewithRegulation…/2012/EC[orTier1UnrestrictedBasicOwnFundsinaccordancewithDirective 2009/138/EC],or ElementsthatmeetbothsetsofrulesforAdditionalTier1inaccordancewithRegulation…/2012/ECandTier1[RestrictedBasicOwnFundsinaccordancewithDirective2009/138/EC],or InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |33 (c)elementsthatmeetbothsetsofrulesforTier2inaccordancewithRegulation…/2012/ECandforTier2inaccordancewithDirective2009/138/EC. 3.Cross-sectorownfundselementsmentionedinpoint2shallonlybetakenintoaccountiftheirtransferabilityandavailabilityacrossthedifferentlegalentitiesinthefinancialconglomeratemeettheconditionssetoutinArticle4. EXPLANATORYTEXTforconsultationpurposes ThetextisbasedontheTechnicalprinciplesinAnnex1oftheDirective“Whichevermethodisused,whentheentityisasubsidiaryundertaking andhasasolvencydeficit,or,inthecaseofanon-regulatedfinancialsectorentity,anotionalsolvencydeficit,thetotalsolvencydeficitofthesubsidiaryhastobetakenintoaccount. Whereinthiscase,intheopinionofthecoordinator,theresponsibilityoftheparentundertakingowningashareofthecapitalislimitedstrictlyand unambiguouslytothatshareofthecapital,thecoordinatormaygivepermissionforthesolvencydeficitofthesubsidiaryundertakingtobetakenintoaccountonaproportionalbasis.” InlinewiththeDirectiveonlycross-sectorownfundsareallowedasaremedytoaconglomeratedeficit. Thatis,fromthepointatwhichaconglomeratedeficitisobserved,thatshortfallamountshallbecoveredbytheissuanceofcross-sectorown funds,regardlessofthecauseoftheconglomeratedeficit. Thefinancialconglomerateshallinformthecoordinatoraboutthedeficitandthemeasurestocoverthisdeficitwithoutdelay. Article6Consistency 1.TheMethodofCalculationselectedfromthosemethodsdefinedinAnnex1oftheDirectiveshallbeappliedinaconsistentmannerovertime. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |34 2.ForthepurposeofArticle6(2)andAnnex1oftheDirective,forabankingledconglomerate,whereArticle46(1)oftheCRRisapplied,thecoordinator,afterconsultingwithothercompetentauthoritiesconcerned,shalldecidethemostprudentmethodtobeappliedbythefinancialconglomerate. Article7Consolidation ForthepurposeofArt6(2)andAnnex1oftheDirective,Method1oftheDirective2009/138/ECshallbeconsideredasequivalenttotheconsolidationasdefinedunderMethod1oftheDirective,for insurance-ledfinancialconglomerate. Theequivalenceassessmentisvalidprovidedthatthescopeofthegroup underSolvencyIIisthesameundertheDirectiveorthedifferenceinthescopeisnotmaterial. EXPLANATORYTEXTforconsultationpurposes ThistextisbasedontheDirective2009/138/EC,Article230inconnectionwithArticles220ss. TheSolvencyIIImplementationmeasureswillneedtobeconsideredoncetheyhavebeenpublished. AccordingtoDirective2009/138/EC,forthecalculationofgroupownfundsallthemultipleuseofeligibleownfundsandintra-groupcreationofcapitalshouldbeeliminated. Moreover,ownfundsofotherfinancialsectorsshouldbecalculatedaccordingtotherelevantsectorrules. Asaresult,bothMethod1oftheDirective2009/138/ECandMethod1oftheDirectiveareconsistentwiththemainobjectivesofthesupplementarysupervisionsincetheyensurethat:alldouble-countingis InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |35 removed;ownfundsarecalculatedinaccordancewiththedefinitionsandlimitsestablishedintherelevantsectoralrules. Theequivalenceassessmentisvalidprovidedthatthescopeofthegroup underSolvencyIIisthesameundertheDirectiveorthedifferenceinthescopeisnotmaterial. Article8 Solvencyrequirement 1.Forthepurposeofthecalculationofthesupplementarycapital adequacyrequirementsoftheregulatedentitiesinafinancialconglomerate,asolvencyrequirementshallsatisfyeitherofthepointslaiddownin(a)and(b): Wheretherulesfortheinsurancesectoraretobeapplied,solvencyrequirementmeanstheSolvencyCapitalRequirementasdefinedbyArticle100or218ofDirective2009/138/ECasapplicable,includinganycapitaladd-onappliedinaccordancewithArticles37,231(7)or232ofthesamedirectiveasapplicable,andanyothercapitalorownfundsrequirementapplicableunderUnionlegislation. Wheretherulesforthebankingorinvestmentservicessectoraretobeapplied,solvencyrequirementmeansthesumofownfundsrequirementsasdefinedbyArticles87to93ofCRR,combinedbufferrequirementsasdefinedbyArticle122ofCRDIV,andspecificownfundsrequirementsasdefinedbyArticle100of[CRDIV],andanyotherrequirementapplicableunderEuropeanUnionlaw. Article9 Thefinancialconglomerate'sownfundsandcapitalrequirements 1.ExceptwhereexpresslystatedinthisRegulatoryTechnicalStandard,thefinancialconglomerate'sownfundsandcapitalrequirementsshallbecalculatedinaccordancewiththedefinitionsandlimitsestablishedintherelevantsectoralrules. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |36 TheownfundsofassetmanagementcompaniesshallbecalculatedaccordingtoArticle2(l)ofDirective2009/65/EC;thecapitalrequirementsarecalculatedaccordingtoArticle7(1)(a)ofDirective 2009/65/EC. Theownfundsofalternativeinvestmentfundmanagersshallbe calculatedaccordingtoArticle9ofDirective2011/61/EU. Article10 Sectorspecificownfunds 1.Sectorspecificownfunds,arerecognisedforthecoverageofrisksatthesectorallevelonlyandcannotbeusedtocoverrisksofanothersectorandshallnotbeincluded(aboveor)beyondthesectorallevel. Sectorspecificownfundsareownfundsrecognisedundersectoralrulesthatdonotfallwithinoneofthefollowingcategories: CommonEquityTier1,AdditionalTier1andTier2ownfundsunder[CRR];or Tier1unrestrictedbasicownfunds,Tier1restrictedbasicownfunds,andTier2basicownfundsunderDirective2009/138/EC. 2.Risksoriginatingfromtheothersectorshallnotbecoveredbysectorspecificownfunds. EXPLANATORYTEXTforconsultationpurposes Article10setsoutthatsector-specificownfundscannotcoverrisksabovesectoralrequirements. Inpractice,thismeansthat,foreachrelevantentityorgroupofentities,conglomeratesneedtofirstcountsector-specificownfundsagainsttheir requirements(whilerespectingsectoralrulesandlimits). Ifthereisanexcessofsector-specificownfunds,thisshallnotbe InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |37 recognisedatconglomeratelevel. Inaddition,asstatedinArticle4,anynon-sector-specificownfundsinexcessofsectoralrequirementsneedtooriginatefromentitieswhicharenotsubjecttotransferability/availabilityimpediments. Article11 Treatmentofcrosssectorholdingsforthecalculationofcapitalrequirements Whereaninsuranceholdingofabank-ledfinancialconglomerateoraninvestmentfirm-ledfinancialconglomerateiseliminatedpursuanttoArticles14.3and14.4orArticle15.2ortheapplicationoftheseArticlesaspartofMethod3,nocapitalchargeforthatholdingshallbeappliedatthefinancialconglomeratelevelforthepurposeofsupplementarysupervision,evenifacapitalchargeisappliedatsectorallevel. EXPLANATORYTEXTforconsultationpurposes Atsectorallevel,holdingsmayreceiveariskweightorcapitalcharge. Atthefinancialconglomeratelevel,thesameholdingmaybedeductedoreliminatedfromownfundsthroughconsolidation,makingtheriskweightorcapitalchargesuperfluous. Thiscapitalchargeshallthusnotbeappliedforthepurposesofthecalculationoftheconglomeratessolvencyrequirements. Article12 Non-regulatedfinancialentities 1.Foranon-regulatedmixedfinancialholdingcompanyandfora non-regulatedentityheldbyamixedfinancialholdingcompany,theown fundsandthecapitalrequirementsattributabletothenon-regulated financialsectorentitiesshallbecalculatedaccordingtothemostimportantsectorinthefinancialconglomerateinaccordancewithArticle3(2)oftheDirective. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |38 2.Theownfundsandthesolvencyrequirementsattributabletoothernon-regulatedfinancialentitiesshallbecalculatedaccordingtothesectoralrulesofthesector(insuranceorbanking)towhichthenonregulatedentityisdesignated. EXPLANATORYTEXTforconsultationpurposes A“mixedfinancialholdingcompany”isdefinedunderArticle2(15)oftheDirective. Whichevermethodisused,forthepurposeofthecalculationofthesupplementarycapitaladequacyofafinancialconglomerate,bothanotionalcapitalrequirementandnotionallevelofownfundsshouldbecalculatedfornon-regulatedfinancialentities. Theseshouldbecalculatedaccordingtotherulesofthesectortowhichthenonregulatedentitybelongs,oraccordingtothemostimportantsectorintheconglomerate,havingregardtoAnnex1oftheDirective“Inthecaseofanon-regulatedfinancialsectorentity,anotionalsolvencyrequirementiscalculatedinaccordancewithsectionIIofthisAnnex,notionalsolvencyrequirementmeansthecapitalrequirementwithwhichsuchanentitywouldhavetocomplyundertherelevantsectoralrulesasifitwerearegulatedentityofthatparticularfinancialsector;thenotionalsolvencyrequirementofamixedfinancialholdingcompanyshallbe calculatedaccordingtothesectoralrulesofthemostimportantfinancialsectorinthefinancialconglomerate”. Article13 Transitionalandgrandfatheringarrangements Thesectoralrulesappliedinthecalculationofconglomerateownfundsandsolvencyrequirementsshalltakeintoaccountanytransitionalorgrandfatheringarrangementsinforceatsectorallevel. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |39 TITLEIII Technicalcalculationmethods Article14 Method1Calculationcriteria Theownfundsofafinancialconglomerateshallbecalculatedonthebasisoftheconsolidatedaccounts(accordingtotherelevantaccountingframework)appliedtothescopeofsupplementarysupervisionoftheDirective. Thecalculationofownfundsshalltakeintoaccounttheremovalofintragroupbalances,transactionsandincomeandexpensesrelatedtotheprocessofaccountingconsolidation. Forbank-ledandinvestmentfirm-ledconglomerates,unconsolidatedsignificantinvestmentsinafinancialsectorentitypursuanttoArticle40oftheCRRshallbefullydeducted,iftheentitybelongstotheinsurancesectorasdefinedinArticle2(8)oftheDirective. UnconsolidatednonsignificantinvestmentsaredeductedinaccordancewiththetreatmentdescribedinArticle43ofCRR. Forbank-ledandinvestmentfirm-ledconglomerates,thesectoraltreatmentinPart2,TitleIIoftheCRRshallapplytoallunconsolidatedinvestments,participationsandholdingsofaconglomerateentity,providedthat: Theconglomerateentityisacreditinstitutionoraninvestmentfirm;and Theinvestment,participationorholdingisinacreditinstitutionorinaninvestmentfirm. 6.Withoutprejudicetopoints3and4,anyotherownfundsissuedbyoneconglomerateentityandheldbyanother,ifnotalreadyeliminatedintheaccountingconsolidationprocess,shallbededucted. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |40 Jointcontrolledentitiesshallbetreatedinaccordancewithsectoralrules. ThevaluationofassetsandliabilitiescalculatedforthepurposesofDirective2009/138/ECshallbeusedatthelevelofthefinancialconglomerate. WhereassetorliabilityvaluesaresubjecttothecalculationofprudentialfiltersanddeductionsinaccordancewiththoserequiredunderCRR,theassetorliabilityvaluesusedshallbethoseattributabletotherelevantentitiesunderCRR,excludingassetsandliabilitiesattributabletootherentitiesofthefinancialconglomerate. Wherecalculationofathresholdorlimitisrequiredinordertorespectsectoralrules,thethresholdorlimitshallbecalculatedonthebasisoftheconsolidateddataofthefinancialconglomerateandaftertheremovalofholdingscalledforbythesestandards. Wherecreditinstitutions/investmentfirmsandrelatedentitiesare consolidatedunderCRR,thesameentitiesshallbeconsideredtogether. WhereinsuranceandrelatedentitiesareconsolidatedunderDirective 2009/138/EC,thesameentitiesshallbeconsideredtogether. ConglomerateentitiesthatarenotconsolidatedunderCRRorDirective2009/138/ECshallbetreatedseparately. Forthepurposeofthecalculationofsolvencyrequirements,eachsectorshallrespecttherequirementsascalculatedundertherelevantsectoralrules. WhensummingtherelevantsectoralsolvencyrequirementsthereshallbenoadjustmentotherthanasforeseenbyArticle11ofTitleIIorascausedbyadjustmentstosectoralthresholdsandlimitspursuanttopoint9ofthisArticle14. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |41 EXPLANATORYTEXTforconsultationpurposesACCOUNTINGCONSOLIDATIONANDJOINT CONTROLLEDENTITIES(Points1,2and7) UnderMethod1,theDirectiverequiresthecalculationoftheownfundsoftheconglomerateonthebasisoftheconsolidatedpositionofthegroup. Inaddition,anyinappropriateintra-groupcreationofownfundsmustbeeliminated. Inordertoensuretheseprovisionsarerespected,points1and2ofArticle14requirestheconglomeratetouseconsolidatedaccounts(appliedtothescopeoftheconglomerate)asthestartingpointforthecalculationoftheownfunds. Indoingso,theconglomeratemustallowalleliminationsofownfundsarisingfromtheprocessofaccountingconsolidationtotakeplace. Joint-controlledentitiesaretobeproportionallyconsolidatedinlinewith point6. OTHERINTRA-GROUPCREATIONOFOWNFUNDS (Point6) InlinewiththeDirective’sprinciples,Article3ofthisRegulationcallsfortheeliminationofallownfundsthathavebeencreatedbyintra-grouptransactions,beitdirectorindirect. FortheavoidanceofdoubtinthecontextofMethod1,point5furtherspecifiesthatallintra-groupcreationofownfundsshouldbeeliminatedontopofaccountingconsolidation,ifnotalreadyeliminatedaspartoftheaccountingconsolidationprocess. SuchadditionaleliminationmayberequiredinparticularwherethetreatmentoftheparticipationcalledforbytheDirectiveisdifferentfromthatprovidedforbyaccountingrules,consideredthataccountingrules InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |42 doesn’tconsiderthemultiplegearingissue. CROSSSECTORHOLDINGSANDOTHERHOLDINGS (Points3,4and5) Forbank-ledandinvestmentfirm-ledconglomerates,thecalculationofownfundsattheleveloftheconglomerateshouldalsotakeintoaccount thatthesectoralrulesallowinstitutionstoriskweightandnotdeductsomecross-sectorholdings. Forthisreason,inordertoensuretheeliminationofmultiplegearingatthelevelofconglomerate,point3ofArticle14requiresthedeductionofholdingsthatareneitherconsolidatednoreliminated(bydeduction)atsectorallevel,wherethoseholdingsareinentitiesbelongingtotheinsurancesector. Point4describesthetreatmentofunconsolidatednon-significantinvestmentholdingswherethoseholdingsareinentitiesbelongingtoinsuranceentities. Point5describesthetreatmentofotherholdings,specifyingthatotherholdingsaretreatedaccordingtosectoralrules(seethetableinAnnexII). SOLVENCY2VALUATIONCRITERIA(Points8) Forinsurancepartsoftheconglomerate,giventhatArticle75ofDirective 2009/138/EUsetsoutspecificvaluationrulesforassetsandliabilities,point8ofArticle14specifiesthatassetsandliabilitiesforthoseentitieswithintheconglomerateshouldfollowthevaluationscalculatedforthepurposeofDirective2009/138/EU. Thispointisaimedatensuringthatthecalculationoftheelementsofownfundsatthelevelofconglomerateisconsistentwithsectoralrules. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |43 RECALCULATIONOFLIMITSANDTHRESHOLDS,TAKINGINTOACCOUNTREMOVALOFHOLDINGS (Points9) Oncetheaccountingconsolidationhasbeencarriedout,aswellastheotherprovisionsalreadymentioned,amountsofCET1attributabletoconglomerateentitiesthataresubjecttoCRRatsectorallevel,aswellasamountsofholdingsbelongingtosuchentitiesthatareneitherdeducted norconsolidated,willchange. SothecalculationsbasedonCET1inArticle45ofCRR,whichmeasurethethresholdforthedeductionofdeferredtaxassetsandsignificant investments,shouldberecalculated. TherecalculationshouldtakeintoaccounttheeffectonCET1oftheconglomerateaccountingconsolidationprocess,proportionalconsolidationinaccordancewithpoint7,theremovalofholdingsinpoint3,andanyotherfactorsstemmingfromtheconglomeratecalculationthathaveledtoachangeinCET1. InthecalculationaccordingtoArticle45ofCRRforanentityorgroupofentities,thedeferredtaxassetsandsignificantinvestmentstobetakenintoaccountareonlythosebelongingtothatentityorgroupofentitieswithintheconglomerate. Theserulesareprovidedforinpoint9. MULTI-LAYERCONGLOMERATES(Points10,11and12) ThisRegulationrecognisesthatfinancialconglomeratestructuresmaybeverycomplexandinvolvedifferentlayers(seegraphexamplebelow). InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |44 Incaseslikethis,whereabankinggroupcontrolsaninsurancegroup,which–inturn–controlsabank,inordertocalculatethelimitsorthresholdsprovidedatsectorallevel,thedataofthebankinggroupatthetopofthegroupshallnotbecalculatedjointlywiththedatabelongingtothebank(B)controlledbytheinsurancegroup. Inthiscase,bank(B)calculatesathresholdonitsDeferredTaxAssets.BearinginmindthattheDirectivestatestheelementseligibleforthe calculationoftheownfundsarethosethatqualifyinaccordancewiththe relevantsectoralrules,point10callsfortherelevantgroupingsatsectoralleveltobemaintainedalsoattheconglomeratelevelforthepurposesof calculatinglimitsandthresholds. SOLVENCYREQUIREMENTS(Point13) Finally,point13specifiesthatthecalculationofsolvencyrequirementsisbasedonthesumofsectoralandnotionalrequirements,exceptfortheprovisionincludedinArticle11(nocapitalchargeforholdingsthatareconsolidatedordeductedattheconglomeratelevel). InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |45 SeealsotheAnnex-Summaryofthetreatmentofholdingsand participationsforthepurposeofthecalculationoftheownfundsoftheconglomerate. Article15 Method2Calculationcriteria 1.ForthepurposeofcalculatingMethod2assetoutinAnnexIpartIIoftheDirective: Theproportionalshareapplicabletoownfundsandsolvencyrequirementsshallrelatetotheproportionofthesubscribedcapitalwhichisdirectlyorindirectlyheldbytheparentundertakingorundertakingwhichholdsaparticipationinanotherentityofthegroup; Thebookvalueofparticipationsinotherentitiesofthegroupshallbethebookaccountingvaluefortheparentundertakingorfortheundertakingthatholdsaparticipationinanotherentityofthegroup; Wheretheownfundsofaholdingissubjecttoaprudentialfilter,thefilteredamountsshallbe: Addedtothebookvaluementionedinb),ifthefilteredamount increasesregulatorycapital;or Deductedfromthebookvaluementionedinb),iffilteredamountdecreasesregulatorycapital. (d)Forthepurposeofpoint(c),thefilteredamountspertainstothenetamountaffectingownfundsoftheholding. 2.Forbank-ledandinvestmentfirm-ledconglomerates,significant investmentsinafinancialsectorentitypursuanttoArticle40oftheCRR,iftheentitybelongstotheinsurancesectorasdefinedinArticle2(8)oftheDirective,shallbe: (a)Fullydeducted,wheretheholdingisnotaparticipationasdefinedinArticle2(11)oftheDirective,and InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |46 (b)TreatedaccordingtoMethod2,wheretheholdingisaparticipationasdefinedinArticle2(11). Forinsurance-ledconglomerates,participationasdefinedinArticle2(11)oftheDirectiveshallbeconsideredfortheapplicationofpoint1. Forthepurposeofthefirstpoint,toeliminatetheintra-groupcreationofownfunds,theeligibleamountofintra-groupinvestmentsinanycapitalinstrumentsthatareeligibleasregulatorycapital,respectingrelevantsectorallimits,shallbeeliminated. EXPLANATORYTEXTforconsultationpurposes Point1(c)addressescaseswhereprudentialfiltersaffecttheownfundsofaparticipationforprudentialpurposesbyaddingbackunrealisedlossesorsubtractingunrealisedgains,forexampleinthecaseofaholdingheldintheAvailableForSalecategory. Ifthisisthecase,theeffectoftheprudentialfiltershouldbereversed[byadjustingthebookvalueoftheparticipationtobededucted]. Withoutthisreversalthefilteringofunrealisedgainswouldundulyreduceownfundsafterdeductionofaccountingbookvalue,whilethefilteringofunrealisedlosseswouldundulyflatterownfundsafterthedeductionofaccountingbookvalue. ReferringtotheformulaintheAnnex:if,becauseoftheapplicationofaprudentialfiltertheOwnFundstermxi(OFi-REQi)changes,thenitseffectshouldbeneutralizedbyanoffsettingadjustmentinthebookvalueterm:BVi. SeealsotheAnnex-Summaryofthetreatmentofholdingsand participationsforthepurposeofthecalculationoftheownfundsoftheconglomerate. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |47 Article16 Method3Calculationcriteria 1.Thecompetentauthoritiesmaypermitthefinancialconglomeratetouseacombinationofmethods1and2,onlywherethefinancialconglomeratecandemonstratetothecompetentauthoritiesthatitsrequesthasbeenmade: Furthertoitsbestefforttoapplyeither,Methods1or2;and HavingregardtothecasesinArticle6(5)oftheDirective. Ifseveralentitiesarecollectivelyofnonneglibleinterest,thecompetentauthoritiesshalltakethisintoaccountinassessingtherequesttouseMethod3. TheapplicationofthespecificcombinationofMethods1and2toentitieswithinthefinancialconglomeratethatwaspermittedbycompetentauthoritiesshallbeappliedinaconsistentmannerovertime. Thecoordinatorshallconsulttheotherrelevantcompetentauthoritiesbeforetakingadecisiononwhethertopermittheuseofthecombinationofmethods1and2. EXPLANATORYTEXTforconsultationpurposes Article6(5)(a)(b)and(c)oftheDirectivestates: “(a)Iftheentityissituatedinathirdcountrywheretherearelegalimpedimentstothetransferofthenecessaryinformation,withoutprejudicetothesectoralrulesregardingtheobligationofcompetentauthoritiestorefuseauthorisationwheretheeffectiveexerciseoftheirsupervisoryfunctionsisprevented; (b)Iftheentityisofnegligibleinterestwithrespecttotheobjectivesofthesupplementarysupervisionofregulatedentitiesinafinancialconglomerate; InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |48 (c)Iftheinclusionoftheentitywouldbeinappropriateormisleading withrespecttotheobjectivesofsupplementarysupervision. However,ifseveralentitiesaretobeexcludedpursuantto(b)ofthefirstsubparagraph,theymustneverthelessbeincludedwhencollectivelytheyareofnon-negligibleinterest.” TITLEIV Finalprovisions Article17 ThisRegulationshallenterintoforceonthetwentiethdayfollowingthatofitspublicationintheOfficialJournaloftheEuropeanUnion. ThisRegulationshallbebindinginitsentiretyanddirectlyapplicableinallMemberStates. DoneatBrussels,FortheCommissionThePresident [FortheCommission OnbehalfofthePresident[Position] InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |49 ANNEXI CalculationmethodologyforMethod2–Deductionandaggregationmethod 1.Generalprinciples Thecalculationofmethod2shallbecarriedoutonthebasisoftheregulatoryreportingrequiredundertheapplicableaccountingframeworkofeachoftheentitiesinthegroupfollowingtheformulaicexpression below: whereownfunds(OFi)excludeintra-groupcapitalinstruments. Thesupplementarycapitaladequacyrequirements(scar)shallthusbecalculatedasthedifferencebetween: Thesumoftheownfunds(OFi)ofeachregulatedandnon-regulated financialsectorentity(i)inthefinancialconglomerate;theelementseligiblearethosewhichqualifyinaccordancewiththerelevantsectoralrules;and Thesumofthesolvencyrequirements(REQi)foreachregulatedand non-regulatedfinancialsectorentity(i)inthegroup(G);thesolvencyrequirementsshallbecalculatedinaccordancewiththerelevantsectoralrules;andthebookvalue(BVi)oftheparticipationsinotherentities(i)ofthegroup. Inthecaseofnon-regulatedfinancialsectorentities,anotionalsolvencyrequirementshallbecalculatedaccordingtoArticle11.Ownfundsandsolvencyrequirementsshallbetakenintoaccountfortheirproportionalshare(x)asprovidedforinArticle6(4)andinaccordancewithAnnexI. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |50 Thedifferenceshallnotbenegative. ANNEXII-Summaryofthetreatmentofholdingsandparticipationsforthepurposeofthecalculationoftheownfundsoftheconglomerate InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com