Download

1 / 100

1.01k likes | 1.26k Views

Alternative Thinking About Investments December 2009. Words of Wisdom. “Any plan conceived in moderation, must fail when circumstances are set in extremes” Prince Metternich “You must unlearn, what you have learned…” Yoda.

E N D

Words of Wisdom “Any plan conceived in moderation, must fail when circumstances are set in extremes” Prince Metternich “You must unlearn, what you have learned…” Yoda

“Old Plan” Produced Poor Returns For Over a Decade GOLD Buffet S&P NASDAQ 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Source: Bigcharts.com 3

We “Know” Stocks Beat HF, Except Past Two Decades Hedge Funds and S&P 500 – Historical Performance 2009 For 20 Year Period, S&P 500 returned 6.5%, Hedge Funds returned 13.2% Source: Bloomberg, HFRI 4

The Endowment Model is Broken?? Says Who? Source: Barron’s November 2008

Endowments Crushed Traditional Funds Past Decade Source: Barron’s November 2008 6

12 Months, Does Not a Trend Make: 0-10-1 Not Good… Even With Unrealistic Assumptions, Best They Can Get is a TIE for Fiscal Year 2009…. Source: Barron’s November 2008, July 2009 7

Endowments Outperform Traditional Portfolios -Why? Comparative Performance vs. NACUBO Endowment Universe UNC Investment Fund Portfolio Strategic Investment Policy Portfolio (Blended Benchmark of Endowment Asset Classes) 70/30 Index (S&P 500 / Barclays Bond) Source: NACUBO Endowment Study 2008Data as of 06/30/08 8

Large Endowments Outperform Small Endowments – Why? Source: Commonfund Benchmarks Study 2008Data as of 06/30/08 UNC Portfolio

Large Endowments Win for Three Primary Reasons Source: Commonfund Benchmarks Study 2008Data as of 06/30/08 UNC Portfolio

Large Endowments Focus on Highest Impact Areas Contributors to Long-Term Portfolio Returns ActivityImpact Asset Allocation Largest Value Added Manager Selection Time & Resource Intensive Portfolio Construction Most Overlooked Opportunity Security Selection Most Overvalued Activity Academic literature shows that 85-90% of portfolio return comes from first three areas, yet bulk of investment industry focuses on #4

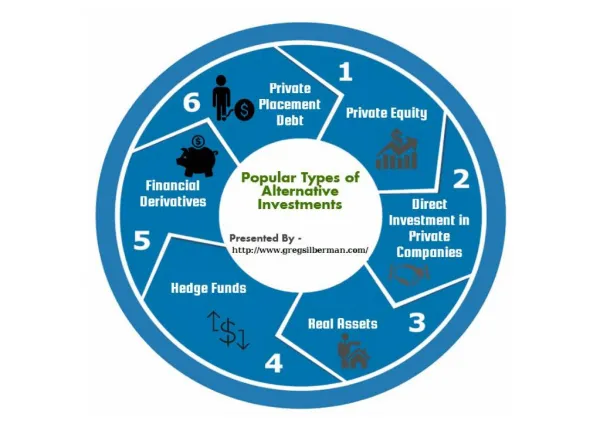

Traditional Portfolios Are Too U.S. Equity-Centric Target DE LV DE LG DE MV DE MG DE SV DE SG 50% International Equity Value International Equity Growth International Equity Emerging Markets 15% 5% Absolute Return Hedge Funds 5% Private Equity Venture Capital Private Equity Buyouts Private Equity International 5% Inflation Hedge Real Estate - REITs Inflation Hedge Real Estate - Private Fixed Income Domestic Fixed Income Global 20%

Large Endowments Integrate Alternatives into Portfolio Target 10% 30% Domestic Equity Long International Equity - Developed Long International Equity - Emerging Markets Long Domestic Equity Long/Short International Equity - Developed Long/Short International Equity – Emerging Markets Long/Short Absolute Return Event Driven Absolute Return Event Driven 10% Absolute Return Relative Value Absolute Return Relative Value Global Opportunistic Long/Short & Macro 10% Private Equity Domestic Private Equity International 15% Real Estate – REITs Global Real Estate – Private Global 15% Energy & Natural Resources Global Fixed Income Domestic Fixed Income Global Fixed Income Enhanced & Distressed 10%

Best Portfolios Focus on Consistent Compounding From 1950 to 2008, the arithmetic average annual return of the S&P 500 has been 8.1% with a standard deviation of 17%.1 $125mm $65mm Over that time period, an investment with the same return but half the volatility creates over 90% more wealth.2 The above information is hypothetical and is meant as an illustration only. Unmanaged indices are for illustrative purposes only. An investor cannot invest directly in an index. Past performance is no guarantee of future results. Source: 1. Standard & Poor’s and Bloomberg 2. Morgan Creek Capital Management, LLC. 14

The Real Return Challenge Will a Traditional portfolio of public equities and bonds generate enough return over the next decade to meet spending requirements without reducing the real value of the underlying assets? Where will returns come from? Alternative Investments? Maybe 15

The Real Return Challenge Will a Traditional portfolio of public equities and bonds generate enough return over the next decade to meet spending requirements without reducing the real value of the underlying assets? Where will returns come from? Alternative Thinking? Definitely 16

Current Trends Suggest Lower Future Returns May be difficult to match long-term domestic equity performance going forward. Source of Equity Returns Current Environment Source of Equity Returns S&P 500 1926-2008* 10.8% • Price Earnings Multiples remain above long term average levels • Real Earnings Growth is expected to be below normal for some time • Dividends remain at below average levels • Inflation is currently much lower than the historical average P/E Expansion (1.3%) Real Earnings Growth (2.1%) 5.0% P/E Expansion (0%) At Best Dividends (4.3%) Real Earnings Growth (1.1%) Dividends (2.9%) CPI / Inflation (3.1%) CPI / Inflation (1.0%) Source: Research Study conducted by Ibbotson & Chen. Research Report dated 2000. Study has not been replicated since 2000. Statistics above may not reflect current market statistics. Dividends represent dividend yield of Standard & Poor’s 500 as of 12/31/08. Inflation rate reflects CPI as of 12/31/08 (information from Labor of Bureau Statistics). Source: Hatteras Investment Partners

Traditional Portfolios Will Struggle to Meet Objectives In the past, a traditional portfolio of equities and bonds generated enough return to meet your investment objectives. However, this may not be the case in the near future. 12% 100% Equities 10% Investment Objective: > 10% 60%/40% Mix 8% 100% Fixed Income 6% Rate of Return 100% Cash 100% Equities 4% 60%/40% Mix Historic Performance 1926-20031 2% 100% Fixed Income Efficient Frontier – Current Environment2 100% Cash 0% 0% 3% 6% 9% 12% 15% 18% 1Ibbotson 2004 Yearbook 2 GMO Expected Returns, 60/40 Mix = 60% S&P 500, 40% LGCI Risk Source: Hatteras Investment Partners

Making the Case for Building a Different CORE Portfolio Adding Uncorrelated Investments to the Traditional Portfolio can boost expected returns, while reducing portfolio volatility. 12% 100% HFRI FoF Index 10% 8% 40% FoF Added Rate of Return 6% 20% FoF Added 100% Equities 4% 100% Fixed Income 60%/40% Mix 2% Efficient Frontier of Traditional Asset Classes – Current Environment1 Efficient Frontier with HFRI Fund of Funds Added – Current Environment1,2 Incremental Addition of HFRI Fund of Funds to 60%/40% Stock/Bond Mix 100% Cash 0% 0% 3% 6% 9% 12% 15% 18% 1 GMO Expected Returns, 60/40 Mix = 60% S&P 500, 40% LGCI 2 PerTrac Model Risk Source: Hatteras Investment Partners 19

Click to edit Master title style How Did We Get Here?

Words of Wisdom “And you may ask yourself, well, how did I get here?” David ByrneTalking Heads “A surplus of cash led to a shortage of sense” Marc FaberGloom, Doom & Boom Report

How We Got Here: 6 Decades of Increasing Leverage • Massive build-up of corporate and consumer leverage supported by falling interest rates, declining underwriting standards and reduced regulatory oversight. Source: Federal Reserve, U.S. Commerce Dept., Ned Davis Research

Credit Markets Warned of Depression Scenario HY Spread at end of ’08: 1350 bps HY Avg: 433 bps IG Spread at end of 08: 250 bps IG Avg: 75 bps • Spreads on Investment Grade and High Yield debt pushed to historic highs. Source: Bloomberg

Deflation Hit Equities Hard in 2008, Just Like 1930’s • The S&P experienced its 2nd largest decline ever from its all-time high in Oct ‘07 (almost 52%), second only to the drop in ’32 (over 80%). • S&P 500’s 2008 loss of 37% was second worst annual loss (largest was 1931 decline of 43%) Source: Bloomberg

Federal Reserve balance sheet increased by over 100% in last year TARP legislation includes huge investments, loans, guarantees AIG/Fannie/Freddie/Citi bailouts requiring massive $ commitments Huge Government Policy Response to Deflation Threat Federal Reserve Assets $B Federal Reserve Liabilities $B Source: Federal Reserve Release H.4.1.

Fed “Writing Checks Their Body Can’t Cash” ?? Source: TIS Group

Click to edit Master title style Where Do We Go From Here?

Demographics Points to Deflationary Shake-Out Source: HS Dent Foundation

Headlines Warn of Inflation, Data Says DEFLATION Source: TIS Group

Deflation & Deleveraging: A Lethal Combination Source: UBS

Worse Than Normal Recession, not Depression, Yet… • Annual GDP Growth (Recession): Range -2% to -5% • 4Q 2008: -6.2% • 1Q 2009: -6.5% • 2Q 2009: -4.5% • 3Q 2009: +3.5%?? • Average: 3.5% (1930-present) • Unemployment (Repession): • 8% to 15% • September: 10.2% • GS forecasts well over 10% by the end of 2011 • Average (Post-WW II): 5.6% Source: Bloomberg 32

Government Stimulus Having Desired Effect, For Now “First Time” Homebuyer Tax Credit When Tax Incentive Expired in September, Sales Fell Back to Depressed Levels “Cash for Clunkers” Incentive Source: Bridgewater

Bernanke Avoiding Policy Mistakes of 1928-33, So Far… • Monetary tightening in the spring of 1928 leads to economic slowdown and October’s stock market crash • Fed has reduced rates dramatically and quickly • Fed hikes rates to stop the loss of gold reserves and protect the dollar vs. stopping panic in the banking system • No gold standard, flexible exchange rates, coordinated global easing vs. transmission of the crisis through gold standard • Fed finally engages in expansionary monetary policy in 1932, but does not account for the impact of deflation on real interest rates • Bernanke not only cut rates, but is engaging in unconventional easing policies • Neglect of problems in the banking sector, leading to further contraction in monetary supply • Health of the financial system is at the center of U.S. policy. Source: Summary of Friedman/Schwartz arguments in A Monetary History of the United States as presented by Bernanke in “Money, Gold, and the Great Depression” (4/2/2004)

Net Worth Collapsing, Need SAVINGS to Deleverage Source: Bloomberg, Merrill Lynch

Warren Says….Relax (and buy Stocks) Source: Bershire Hathaway

But, Deflation Cycles Can Last LONG Time… Source: GMO 37

Developed World Deep in Debt, Race to Become Japan Source: CLSA 38

Seen This Movie Before; More Debt, Stocks & Yields Fall Source: Hoisington Capital Management 39

Click to edit Master title style We’re Turning Japanese, I Think We’re Turning Japanese, I Really Think So….

What Can We Learn From the Japanese Lost Decades Source: GMO

Deflation: Many Decades For Equities to Catch Bonds Source: BCA

GDP Growth Stagnated as Banks Had to Delever Source: BCA

GDP Growth Slowed as Population Aged, Hmmm Source: GMO

JGB Yields Collapsed, Then Fairly Stable for a Decade Will Next Decade Look the Same Too? Source: Salient

Japan Equity Markets “Bouncing” Down Stairs Down 50% Over a Decade Then Down Another 50%... Will Next Decade Look the Same Too? Source: Salient

Japan RE Down 70% & Then Dead for Decade Will Next Decade Look the Same Too? Source: Salient

Japan/US: Debt to GDP Peaks Look Eerily Similar… Source: CLSA

US Consumers in Worse Shape Than Japanese Were Source: CLSA

Japan “Equity Culture” Died in ’89, US Rolling Over Source: CLSA