Download

1 / 14

140 likes | 297 Views

The Arbitrage Pricing Model. Lecture XXVI. A Single Factor Model. Abstracting away from the specific form of the CAPM model, we posit a single factor model written as

E N D

The Arbitrage Pricing Model Lecture XXVI

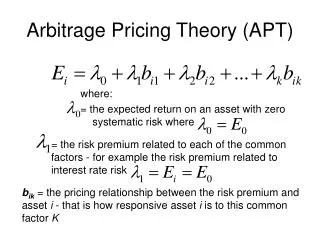

A Single Factor Model • Abstracting away from the specific form of the CAPM model, we posit a single factor model written as • In this model, the random return on an investment zi is a linear function of some random factor fi and an idiosyncratic term i.

Abstracting away from the idiosyncratic risk • If the bis of two assets are the same, then the ais must be the same for an arbitrage free model. • Suppose we are interested in forming a portfolio of two assets with different bis, bi bj , bi 0, bj 0

Holding the variance of the portfolio equal to zero, we find

Multifactor Models: • Suppose that asset returns are generated by a two factor linear model: • A portfolio of these assets then yields

Again to minimize systematic risk • If the portfolio is riskless, then it yields zero profit

The matrix must be singular, or the first row must be a linear combination of the last two rows