Download

1 / 28

280 likes | 396 Views

Scarcity, Production Possibilities, Trade. Key Concepts (all elaborated on in lecture). Absolute and comparative advantage Economic systems Distinguishing characteristics Who owns resources? Who makes economic decisions? Command vs. Laissez-faire systems (& price incentives) Production

E N D

Key Concepts(all elaborated on in lecture) • Absolute and comparative advantage • Economic systems • Distinguishing characteristics • Who owns resources? • Who makes economic decisions? • Command vs. Laissez-faire systems (& price incentives) • Production • Production decisions • What to produce? • For whom to produce (consumer sovereignty)? • How to produce?

Key Concepts (cont’d) • Production possibilities • Production possibility curve (or frontier) • Marginal rate of (product) transformation • Gains from specialization and trade • Inefficiency • Capital (& investment) vs. consumer goods and economic growth 6. Scarcity

Objectives Upon completion of this chapter, you should understand and be able to answer these key questions: • What are the 3 basic economic questions that every society must answer? • What do economists mean by scarcity and how is scarcity related to choice? • What are the opportunity costs of the choices you make? • How does a production possibility frontier (ppf) illustrate opportunity cost, specialization of resources, inefficiency, and economic growth? • What are the differences between command economies, free market economies, and mixed economies in terms of the ways they address the 3 basic economic questions? • Why do we observe specialization in production and trade.

Production decisions: • Suppose Joe is a grain farmer who operates a farm between Ames and Story City. What ‘production’ decisions must Joe make that other business firms (and countries as well) also have to make?

Basic production decisions: • WHAT? • HOW? • FOR WHOM?

Scarcity • Resources are insufficient (i.e. limited, constraining) to meet all goals or wants.

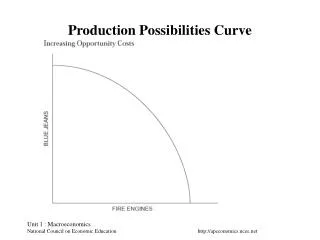

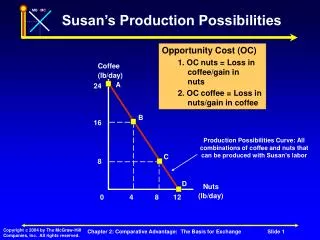

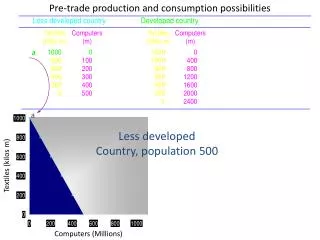

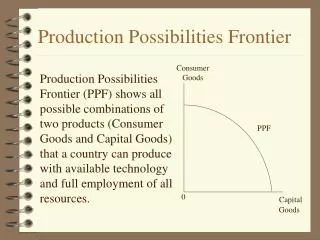

The Production Possibility Frontier • The production possibility frontier (ppf) is a graph that shows all of the combinations of goods and services that can be produced if all of society’s resources are used efficiently.

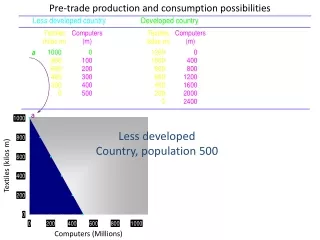

PPF Example #1 • Assume 10 workers in the U.S. can produce 60 (max) units of pharmaceutical products or 30 (max) units of electronic products per day. Draw the PPF for these workers for a day.

PPF Example #2 • Assume 30 workers in Korea can produce 30 (max) units of pharmaceutical products or 60 (max) units of electronic products per day. Draw the PPF for these workers for a day.

Absolute Advantage • A producer has an absolute advantage over another in the production of a good or service if it can produce that product using fewer resources.

Comparative Advantage • A producer has a comparative advantage in the production of a good or service over another if it can produce that product at a lower opportunity cost.

PPF Opportunity Cost • Given by slope of PPF for U.S. and Korea (called MRT = marginal rate of transformation) U.S. Korea

Willingness to Trade • Assume U.S. and Korea agree to: • Have U.S. specialize in producing P • Have Korea specialize in producing E • Trade at rate of 1P for 1E

Gains from each specializing and trading (1P for 1E) Q. Can you draw PPFs for each country?

Increasing Opportunity Cost What are the implications for the shape of a PPF if the opportunity cost is ‘increasing’?

Assume a PPF w/Y on vertical axis, X on horizontal axis. Slope = ΔY / ΔX Opport. Cost of 1 more X = numerator of slope with ΔX = +1 Opport. Cost of 1 more Y = denominator of slope with ΔY = +1

Opportunity Cost in Production = rate at which one should be willing to trade with another

Other PPF Topics • Inefficiency • Consumer vs capital goods and economic growth

Economic Systems = alternative arrangements by which societies resolve production questions Distinguishing characteristics: • Who owns/controls resources? • Gov’t • Individuals • How is economic activity planned/coordinated? • Gov’t (centralized) • Markets (decentralized, laissez-faire, free enterprise)

Central Planning Socialism Communism 100% Sweden UK Japan U.S. Capitalism Gov’t Owns Resources 100% 0

The Coordinating Role (signals) of Market Prices • Hi prices producers & inputs buy less producers & goods sell more consumers & inputs sell more consumers & goods buy less • Lo prices send opposite signals

Consumer Sovereignty • Consumers ultimately dictate what will be produced (or not produced) by choosing what to purchase (and what not to purchase). They ‘vote’ with their pocket books.

Why Government Intervention in Markets? • Since markets are not perfect, governments intervene and often play a major role in the economy. Some of the goals of government are to: • Minimize market inefficiencies • Provide public goods • Redistribute income • Stabilize the macroeconomy: • Promote low levels of unemployment • Promote low levels of inflation

Barriers to Trade (Specialization) • Tariffs (= duties, taxes) • Quotas (= specific quantity limit) • Embargo (= complete ban) • Others (e.g. inspection requirements)

Arguments for Trade Barriers • Protect ‘infant’ industry • Protect national security • Protect human health • Protect domestic producers against ‘unfair’ trade practices of other countries • Protect domestic price support programs