Download

1 / 35

350 likes | 612 Views

Costs. IMBA Managerial Economics Jack Wu. Costs. Introduction. Cost and economies of scale Cost and economies of scope Experience Curve Relevant / Opportunity costs Transfer Pricing Irrelevant Costs/ Sunk costs. Economies of scale.

E N D

Costs IMBA Managerial Economics Jack Wu

Introduction • Cost and economies of scale • Cost and economies of scope • Experience Curve • Relevant / Opportunity costs • Transfer Pricing • Irrelevant Costs/ Sunk costs

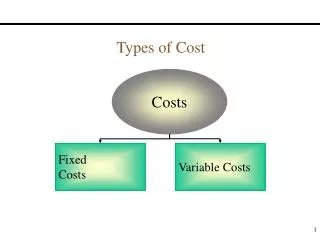

Economies of scale • Fixed cost: cost of inputs that do not change with production rate • Variable cost: cost of inputs that change with the production rate • Fixed/variable costs concepts apply in • Short run • Long run

Economies of scale • Economies of scale (increasing returns to scale): average cost decreases with scale of production

Scale Economies: Sources • large fixed costs • research, development, and design • information technology • falling average variable costs • distribution of gas and water • container ships

Diseconomies of scale • Definition: Diseconomies of scale (decreasing returns to scale) – average cost increases with scale of production

Economies of scale: Strategic implications • Either produce on large scale or outsource • Seller side – monopoly/oligopoly • Buyer side – monopsony/oligopsony

Economies of scale:Google vis-à-vis library • Which link(s) in service chain are scaleable? • Compilation of information • Providing service: servers and network • Responding to enquiries

Economies of scale:Credit card processing • First Data, 44% • National Processing, 13% • Nova, 8% “This is a scale business, and by adding PMT’s volume to our operating platform there is a tremendous advantage” • Nova Chairman Edward Grzedzinski

Economies of scope • Economies of scope: total cost of production is lower with joint than with separate production • Diseconomies of scope: total cost of production is higher with joint than with separate production

Economies of Scope • source -- joint cost: cost of inputs that do not change with scope of production • examples: • cable television + telephone banking + insurance manufacturing: refrigerator + air-conditioner • strategic implication -- produce/deliver multiple products

Economies of scope:Core competence • Technology – apply common technology to multiple products • LCDs – watches, PDAs • Manufacturing – apply same process to multiple products • LCDs, semiconductors • Marketing – brand extensions • spread promotional costs over multiple products/businesses

Diseconomies of scope?Time Warner • Carl Icahn and Bruce Wasserstein: Time Warner should break up into • cable television systems • film and television (including Warner Brothers, HBO and CNN) • Time Inc. and magazines • America Online

HORIZONTAL BOUNDARIES • Economies of scale • Should bank merge with competitor? • Should trucking company acquire smaller rivals? • Economies of scope • Should airline run catering service? • Should bank sell insurance? • Should university open a medical school?

Experience curve: Airbus A350 vs Boeing 787 • April 2004 • Boeing launched 7E7 Dreamliner jet with 50 firm orders from All Nippon Airways. • Aimed to secure 200 orders by December.

Experience curve: Airbus A350 vs Boeing 787 • December 2004 • Boeing achieved 52 firm orders. • Airbus launched A350. • Airbus Chief Commercial Officer John Leahy: A350 would attract a substantial number of Boeing customers and “put a hole in Boeing's Christmas stocking”. • Richard Aboulafia, Teal Group: Airbus had succeeded in its goal of “disrupt[ing] the business case for the 7E7”.

Experience curve • Incremental cost falls with cumulative production run over time • Unit cost falls with cumulative production run • Distinguish from economies of scale within one production period

EXPERIENCE CURVE • Conditions • Relatively large human resources input per unit of production • Relatively small production runs • Industries/processes (learning percentage) • Aerospace (85%) • Shipbuilding (80-85%) • Complex machine tools for new models (75-85%) • Repetitive electronics manufacturing (90-95%) • Repetitive machining or punch-press operations (90-95%)

Experience curve:Strategic implication • Must accurately predict cumulative production • Then set price accordingly • Challenge – quantity demanded depends on competition and price. • Example: Airbus A350 vs Boeing 787.

Relevance • consider only relevant costs and ignore all other costs • which costs are relevant depends on course of action • relevant costs may be hidden • irrelevant costs may be shown in accounts

Opportunity Cost • definition -- net revenue from best alternative course of action • two approaches • show alternatives • report opportunity costs

Example • Williams bought a warehouse and paid $300,000 for it. She used her own money $200,000 and made a bank loan of $100,000. • A developer were willing to buy warehouse for 2 million. • If Williams sells warehouse, she could invest proceeds in government bonds and get a secure income $160,000 (2 million*8%). • She could work elsewhere for salary $400,000.

INCOME STATEMENT SHOWING ALTERNATIVES Income statement reporting opportunity costs

Transfer pricing • Generally, for internal economic efficiency, set transfer price = marginal cost • Special cases • Perfectly competitive market: transfer price = market price • Production subject to full capacity: transfer price = highest marginal benefit from internal use • Compare marginal benefit across internal users

Sunk Cost • definition -- cost that has been committed and cannot be avoided • alternative courses of action • prior commitments • planning horizon • Fewer commitments fewer sunk costs; • longer planning horizon fewer sunk costs.

Example • Jupiter Athletic is about to launch a line of new athletic shoes. Some month ago, management prepared an ad campaign with total budget of $310,000. • They forecast the ad would generate sales of 20,000 units. Each sale’s unit contribution margin (price- average variable cost) is $20. The total contribution margin is $20*20000=$400,000. Their expected profit generated from ad is $400,000-310,000=$90,000.

Example: continued • Recently, a major competitor launch a new shoe. Jupiter estimates sales fall to 15,000 units. The contribution margin becomes $20*15,000=$300,000. • Should Jupiter cancel the launch?

INCOME STATEMENT SHOWING ALTERNATIVES Income statement omitting sunk costs

Sunk vis-à-vis Fixed Costs • Not all sunk costs are fixed • Not all fixed costs are sunk