Download

1 / 33

330 likes | 505 Views

Tuba City Fund Balance Analysis & Expenditure Review. April 30, 2012. Current Budget and Practices. Fund Balance and Expense Trend without State Cash Flow Coverage. 5 Year Fund Balance Summary. Assumptions included in previous charts. All revenue received is expended

E N D

Tuba City Fund Balance Analysis & Expenditure Review April 30, 2012

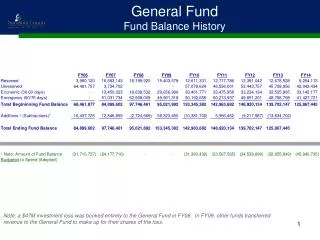

Fund Balance and Expense Trendwithout State Cash Flow Coverage

Assumptions included in previous charts • All revenue received is expended • Impact Aid funded at 85% • No State Aid Reductions • No enrollment decline • No additional expenses added • No additional capital expenses added ($2M continued) • No reductions in expenses • Successful Bond election in 2014 • First sale of Bond proceeds and payment in 2015

Fund Balance Change 2008-09 through 2011-12 • Increases in 2011-12 expenses include: • Additional teachers • Salary increases • Additional maintenance support • Teacherage capital improvements • Includes capital and contingency expenses

2011-12 M&O/impact Aid Budget by Function M&O Fund Impact Aid Fund M&O Total: $10,563,000 Impact Aid Total: $11,200,000

2011-12 Combined Budget by Function Grand Total: $21,763,000

2011-12 Combined Budget by Function GOAL: 50% Instruction Grand Total: $21,763,000

2011-12 M&O/impact Aid Budget by Object M&O Fund Impact Aid Fund M&O Total: $10,563,000 Impact Aid Total: $11,200,000

2011-12 Combined M&O and Impact Aid Budget by Object Grand Total: $21,763,000

Comparison Districts – % of Dollars in the Classroom Auditor General Classroom Spending Report, 2012

Comparison Districts Auditor General Classroom Spending Report, 2012

Comparison Districts Auditor General Classroom Spending Report, 2012

Student Enrollment History 23.7% Decline since 2006 Arizona Department of Education ADMS 46-1 Reports

Student Enrollment Growth Goal • Goal A – Grow Student Enrollment • Goal B – Stabilize/Level Enrollment • Goal C – Status Quo

Historical Review of Enrollment, Expenses and Staffing – 2007-08 through 2011-2012

Accountability Budget Process Approaches • Incremental, Zero-Based, and Program Budgeting • Incremental: compare previous year budget as a basis for incremental amounts to be added or reduced to the new year’s budget • Zero-Based: each line item of the budget is built from zero and must be approved rather than only approving changes to the line items • Program: review individual programs or functional activities independently of the overall budget to determine its fiscal needs

Budget Goals • Return on Investment – ROI • Marketing Schools • Student Achievement • Teacher/Staff Retention • Long Term vs. Short Term Funding Needs • State Reductions • Federal Reductions • Building Needs • Avoiding the Funding Cliff • Maintaining Fund Balance

Budget Accountability • Student Achievement • Increase student achievement • Resources (financial, human and capital) • Responsible budgeting • Effectiveness and Efficiencies • Improve productivity

5 Year Fund Balance Summary – Maintaining $4M Fund Balance, Bond Contingency

2012-13 Budget Variables • Cost Increases • Compensation Increases • State Retirement • Fuel Cost • Enrollment Decline • Federal Funding Decline • Cost Decreases • District Health Insurance • Integrate Alternative School with High School • Consolidate Primary, ENIS, JHS into K-8 • One principal over Gap and Cameron

Future Impact Aid Spending Policy • M&O Transfer – determined by State • Debt Service Payment • Override authorization (conceptual) • Reserves for future Bond – TBD • Current year expenses – TBD