Download

1 / 34

340 likes | 351 Views

This analysis examines the subprime mortgage crisis and its impact on the global financial system, discussing the causes, consequences, and risk management strategies.

E N D

MPI Collective Goods Martin Hellwig Systemic Risk in the Financial Sector An Analysis of the Subprime Mortgage Financial Crisis http://www.coll.mpg.de/pdf_dat/2008_43online.pdf

A Puzzle • Non-Prime Mortgages in the US: 1.1 Trillion US $ • IMF Estimate of Losses in Subprime Mortgage-Backed Securities: 500 Billion US $ • Actual Foreclosure Rate: 3 % • What Explains the Size of the Losses?

Another Puzzle - Why Could Something So Small Overthrow the World Financial System? • So small? • US Mortgages: ca. 13 tr. $, US Residential Real Estate: 20-30 tr. $ World Stock Markets: 40 – 60 tr. $ • S&L‘s ca. 1990: 600 – 800 bn. $ of losses expected • NASDAQ: 1999-2000: 1.6 tr. $, 1999-2002: 3.2 tr. $ NYSE 2000/01: 500 bn. $, 2000/02: 2.5 tr. $ of losses

A Back-of-the Envelope Calculation • 500 bn. out of 1.1 tr. Corresponds to a loss rate of 45 % • With an average equity contribution of 5 %, this corresponds to a loss of 50 % on the property value • Actual Declines 2006 – 2008: 19%

A Back-of-the Envelope Calculation • Role of correlations? • Declines in the most affected metropolitan area: 33 % • Average down payments on subprime: 6 %, on alt-A: 12 % • 2/3 of mortgages date from before the peak. • Panic? Market Malfunctioning? • The S&L experience: 600 – 800 bn. versus 160 bn.

Some Basics: Risk in Real Estate • Real Estate: Large (20 - 30 tr.), long-lived • Subject to valuation risks, dependent on • Interest rates (high rates ~ low values) • Business cycle • Regional risks (Texas 1985!) • Individual property risks

Who Should Bear These Risks? • Intermediary? 1980/81 Experience of S&L’s suggests that this is a bad idea • Borrowers? Experience with Adjustable Rates in late 80’s suggests that this is a bad idea • Third Parties? Yes, but how?

Securitization of Real Estate Risk • Diamond 1984/Hellwig 1994: Have the intermediary issue debt of comparable maturity • Investors bear interest rate risk • Intermediary bears asset-specific risk, retains liability • Example: Pfandbrief in Germany

Mortgage-Backed Securities • Mortgage Brokers provide link between clients and mortgage banks (originators) • Mortgage banks deliver mortgages to a securitization institution • Special purpose vehicle (SPV) creates a package of mortgages • SPV issues claims on package: Senior, Mezzanine, Equity in declining order of priority of claims

Analysis of MBS • Originator has no liability, unless he buys equity claims • SPV/sponsor has no liability unless it provides a guarantee or retains equity • Fannie Mae and Freddie Mac did provide guarantees and imposed quality standards • Packaging provides for standardization (Gale 1992) • Tranching provides for securitization of interest rate risk without strong incentive effects, if the SPV or its sponsor retains equity (Franke&Krahnen 2005).

Practice • Since 2003, Private Investment Banks entered the market, went into subprime lending, GSE retrenched • No guarantees, no liability of SPV • Equity went to Hedge Funds and Investment Banks in search of highly-yielding securities • Mezzanine went to …. SPV’s !!!

MBS CDO‘s • SPV‘s collect portfolios of BBB/unrated mezzanine MBS • Package and tranch them, so that senior tranches get AAA ratings, mezzanine tranches … • Equity tranches held by… see above • Mezzanine tranches go into MBS CDO2 …

Flaws in the Process • Moral Hazard in Origination: Lack of Quality Control, Fraud… 15 fold increase in fraud from 1996 to 2006. • Moral Hazard in Securitization: Lack of Risk Control (UBS Report to Shareholders) • Failure of Internal Controls and „Market Discipline“, Lack of Control by Final Investors/Hedge Funds/Landesbanken… • Yield Mania and Yield Panic

Role of Real Estate Prices • 1999 – 2003: ca. + 10 % p.a. • 2003 – 2005: ca. + 15 % p.a. • 2005 – 2006: + 7 % • 2006 – 2007: - 4 % • 2007 – 2008: - 15 % • Until 2006, the price increases hid • the declines in mortgage quality. [1] Source: Standard & Poors, see Indices at http://www.standardandpoors.com.

Rating Agencies • Neglect of Borrower Creditworthiness • Neglect of Correlations (Common Factors) • Failure to Understand Reasons for Real-Estate Price Increases • Conflict of Interest: Consulting - Rating

Systemic Effects • Maturity Transformation: Conduits, SIVs as vehicles to hold ABS, Refinanced by Asset-Backed Commercial Paper • Motivated by Steep US Yield Curves in 2002 – 2004 (Fed. Funds Rate: 1 – 1.5, 10 year Treasuries 4 – 5)? • Responsibility of Monetary Policy?

Systemic Breakdown in August • Rating Downgrades by several grades at once • Immediate Price Adjustments • Refinancing Breakdown of SIVs/Conduits • Liquidity Assistance Promises of Sponsors come due – and cannot all be met Not one shock, but two: • Extent of Downgrades • Extent of maturity transformation at SIVs (ca. 1000 bn $)

Market Malfunctioning • Market valuations of MBS plummet • Lemons Problems • Changes in Risk Perceptions • Changes in Perceptions of Vulnerability • Changes in Maturity Premia/Risk Premia/Liquidity Premia • A Downward Bubble? • IMF: Market values probably significantly below pdv‘s of debt service

Impact of Fair-Value Accounting • Fair Value Accounting of Market Risks as Prerequisite for a Models Based Approach to Capital Regulation • Mark-to-Market … in non-functioning markets • Large Writedowns…. to be ever increased… • Reduce Bank equity

Insuffiency of Bank Equity I • Buffers in excess of required capital practically nonexistent • Write-downs under fair-value accounting lead directly to an insufficiency of regulatory capital. • Corrective actions: - Recapitalization (UBS = United Bank of Singapore) - Deleveraging

Systemic Implications • Deleveraging exerts pressure on markets, • Further depresses asset prices • Induces other banks to write down assets • So that they have to engage in further deleveraging

Insufficiency of Bank EquityII • Under the 1996 Amendment to Basel I (as well as Basel II), required capital had also been much reduced • „10 % core capital“ really means 2 % equity share in the balance sheet • Write-downs raise questions about bank solvency • Market Mistrust, Lack of Refinancing, Breakdowns of interbank markets

Central Bank Interventions • Since August 2007, central banks have repeated stepped in to provide liquidity when interbank markets broke down • Salvages of Northern Rock, Bear Stearns, Fannie and Freddie • Have raised questions about the appropriateness of central bank interventions to save insolvent/illiquid institutions

Insolvencies and Contagion • The US Treasury thought it could restore a sense of orderly procedure and save money by letting Lehman Brothers go under and have the European creditors of Lehman bear the costs. • Lehman Brothers Insolvency has direct domino effects (AIG, KfW) • Lehman Brothers Insolvency also induces information contagion leading to worldwide market breakdowns and implosions • more costly to the US taxpayer than a rescue of Lehman would have been.

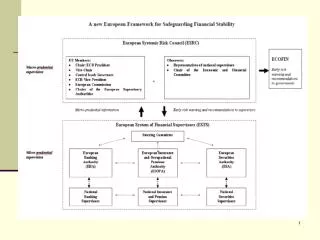

Systemic Risk • Concepts of Systemic Risk: - Dominos through contracts - Dominos through asset prices - Information contagion all relevant in the present context • Systemic Risk: Generated by macro risk or generating the macro risk? • Role of Monetary Policy? 2002 – 2004, 2005 - 2007

Role of Regulation • Distinction On-Balance Sheet/ Off-Balance Sheet, unregulated nature of Conduits, SIVs and Hedge Funds led to intransparency: As late as June 2007, regulators had no idea of what was coming

Role of Regulation • Models Based Approach (to Market Risk) permitted banks to run down their equity/expand their activities: UBS equity less than 3 % of balance sheet • Models did not take account of correlations in US real estate markets • Models did not take into account systemic risk from maturity transformation

Role of Regulation • Deleveraging to meet regulatory requirements was a major element in the unholy trias of market malfunctioning, fair-value accounting, and deleveraging • Procyclical effects in terms of stock variables much more dangerous than procyclical effects in terms of flow variables (Blum-Hellwig 1995, 1996)

Role of Regulation • Regulators do not think in systemic terms, only institution by institution • Miss the role of correlations between underlying and counterparty risks (Hellwig 1995, 1998) • Miss the systemic implications of regulation-mandated corrective actions (Blum-Hellwig 1995, 1996)

Towards Regulatory Reform • Add a notion of protecting markets/the system to the notion of protecting investors – eliminate unregulated institutions

Towards Regulatory Reform • Add an element of capital regulation that is independent of whether the bank‘s model is right or not • Leverage Ratios? • Procyclical, but if the requirement is at 30 % of the balance sheet, the multiplier is much smaller!

Towards Regulatory Reform • Differentiate regulation across institutions so that institutions with long maturities of liabilities are less dependent on short-term market developments and can step in to counteract downward bubbles • Don‘t (!!!) go ahead with Solvency II

Towards Regulatory Reform • Introduce Measures to reduce the procyclical effects of fair-value accounting and capital regulation (Blum - Hellwig 1995, 1996)

Towards Regulatory Reform • Think about what you want the capital regulation to do: - provide a buffer - provide incentives against excessive risk taking - provide a space before insolvency where the supervisor can intervene • The three objectives have very different implications for standards for assessing required capital.