Download

1 / 8

120 likes | 421 Views

Statement of Income and Comprehensive Income. Chapter 3. What Does the Term “Income” Mean? . “Income” may refer to only revenues; or “Income” may refer to ancillary sources of revenue such as “interest income”; or

E N D

What Does the Term “Income” Mean? • “Income” may refer to only revenues; or • “Income” may refer to ancillary sources of revenue such as “interest income”; or • “Income” or “net income” may refer to profit or loss for the period which might also be referred to as “earnings” • Be careful to understand how the term is being used LO 3-1

Economic Income vs. Accounting Income • Economic Income:an increase in the wealth of a corporation; a measureof income based on events rather than transactions. • Accounting income:Using the historical cost measurement principle, accounting income is an increase in the reported wealth of a corporation based on actual transactions completed. LO 3-1

Economic Income vs. Accounting Income (cont’d) • IFRS standards are moving towards the concept of economic income since some “value changes” are recognized, even though no transaction has occurred: • Financial assets and liabilities are reported at fair value at each reporting period • Companies may choose to fair value PP&E and investment properties • Biological assets are measured at fair value less costs to sell LO 3-1

Comprehensive Income • Defined as all changes to owner’s equity that are not the result of transactions with owners • Includes: • Periodic profit or loss; and • Other comprehensive income (OCI) LO 3-1

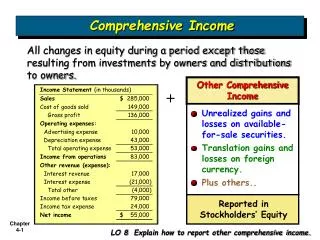

Comprehensive Income Statement • These amounts may be presented as: • a single continuous statement called the Statement of Comprehensive Income (preferred presentation format); or • two separate statements - called the Income Statement and the Statement of Comprehensive Income (which starts with the profit of loss) LO 3-1

Other Comprehensive Income (OCI) • OCI includes changes in values that have not been realized which might represent: • Items that will be recognized in income once realized (i.e. fair value changes in financial assets) • Items that will be matched by an offsetting gain or loss in a future period (i.e. a qualifying hedge of a future transaction) • Items that will impact retained earnings directly and not “recycle” through to net earnings (i.e. revaluation surpluses on property, plant and equipment) LO 3-1