Download

1 / 27

790 likes | 1.55k Views

The Income Statement, and Comprehensive Income. Chapter 4. LEARNING OBJECTIVES 1. Discuss the importance of income from continuing operations and describe its components. 2. Describe earnings quality and how it is impacted by management practices to manipulate earnings.

E N D

LEARNING OBJECTIVES 1. Discuss the importance of income from continuing operations and describe its components. 2. Describe earnings quality and how it is impacted by management practices to manipulate earnings. 3.Discuss the components of operating and non-operating income and their relationship to earnings quality. 4.Define what constitutes discontinued operations and describe the appropriate income statement presentation for these transactions. 5.Define extraordinary items and describe the appropriate income statement presentation for these transactions. 6. Define earnings per share (EPS) and explain required disclosures of EPS for certain income statement components. 7. Explain the difference between net income and comprehensive income and how we report components of the difference. NOT COVERED 8. Describe the purpose of the statement of cash flows. 9. Identify and describe the various classifications of cash flows presented in a| statement of cash flows. 10. Discuss the primary differences between U.S. GAAP and IFRS with respect to the income statement.

An income statement for a hypothetical manufacturing company that you can refer to as we proceed through the chapter.

Income from Continuing Operations Revenues Inflows of resources resulting from providing goods or services to customers. Expenses Outflows of resources incurred in generating revenues. Gains and Losses Increases or decreases in equity from peripheral or incidental transactions of an entity. Income Tax Expense Because of its importance and size, income tax expense is a separate item.

Operating versus Nonoperating Income Operating Income Nonoperating Income Includes certain gains and losses and revenues and expenses related to peripheral or incidental activities of the company Includes revenues and expenses directly related to the principal revenue-generating activities of the company

Proper Heading Revenues & Gains Expenses & Losses Income Stmt. (Single-Step) NOT COVERED

Gross Profit Operating Expenses Non- operating Items Income Statement (Multiple-Step) Proper Heading

U. S. GAAP vs. IFRS There are more similarities than differences between income statements prepared according to U.S. GAAP and those prepared applying IFRS. Some differences are highlighted below. Has no minimum requirements. SEC requires that expenses be classified by function. “Bottom line” called net income or net loss. Report extraordinary items separately. • Specifies certain minimum information to be reported on the face of the income statement. • Allows expenses classified by function or natural description. • “Bottom line” called profit or loss. • Prohibits reporting extraordinary items.

Earnings Quality Earnings quality refers to the ability of reported earnings to predict a company’s future earnings. Transitory Earnings versus Permanent Earnings

Manipulating Income and Income Smoothing “Most executives prefer to report earnings that follow a smooth, regular, upward path.” ~Ford S. Worthy, “Manipulating Profits: How It’s Done,” Fortune Two ways to manipulate income: • Income shifting • Income statement classification

Goodwill Impairment and Long-lived Asset Impairment Involves asset impairment losses or charges. Operating Income and Earnings Quality Restructuring Costs Costs associated with shutdown or relocation of facilities or downsizing of operations are recognized in the period incurred.

Nonoperating Income and Earnings Quality Gains and losses generated from the sale of investments often can significantly inflate or deflate current earnings. How should those gains be interpreted in terms of their relationship to future earnings? Are they transitory or permanent? ExampleAs the stock market boom reached its height late in the year 2000, many companies recorded large gains from sale of investments that had appreciated significantly in value.

Separately Reported Items Reported separately, net of taxes: Discontinued operations Extraordinary items

Intraperiod Income Tax Allocation Income Tax Expense must be associated with each component of income that causes it. Show Income Tax Expense related to Income from Continuing Operations. Report effects of Discontinued Operations and Extraordinary Items net of related income tax effect.

Extraordinary Items An extraordinary item is a material event or transaction that is both: • Unusual in nature, and • Infrequent in occurrence Extraordinary items are reported net of related taxes

U. S. GAAP vs. IFRS Report extraordinary items separately in the income statement. The scarcity of extraordinary gains and losses reported in corporate income statements and the desire to converge U.S. and international accounting standards could guide the FASB to the elimination of the extraordinary item classification. • Prohibits reporting extraordinary items in the income statement or notes.

Unusual or Infrequent Items Items that are material and are either unusual or infrequent—but not both—are included as separate items in continuing operations.

Discontinued Operations As part of the continuing process to converge U.S. GAAP and international standards, the FASB and IASB have been working together to develop a common definition and a common set of disclosures for discontinued operations. The proposed ASU defines a discontinued operation as a “component” that either (a) has been disposed of or (b) is classified as held for sale, and represents one of the following: a separate major line of business or major geographical area of operations, part of a single coordinated plan to dispose of a separate major line of business or geographical area of operations, or a business that meets the criteria to be classified as held for sale on acquisition.

Reporting for Components Sold Income or loss from operations of the component from the beginning of the reporting period to the disposal date. Gain or loss on the disposal of the component’s assets. Reporting for Components Held For Sale Income or loss from operations of the component from the beginning of the reporting period to the end of the reporting period. An “impairment loss” if the carrying value of the assets of the component is more than the fair value minus cost to sell. Reporting Discontinued Operations

BE 7, 8 and 9 Ex 5, 6, 7, and 8

Basic EPS Diluted EPS Net income less preferred dividends Weighted-average number of common shares outstanding for the period Reflects the potential dilution that could occur for companies that have certain securities outstanding that are convertible into common shares or stock options that could create additional common shares if the options were exercised. Earnings Per Share Disclosure One of the most widely used ratios is earnings per share (EPS), which shows the amount of income earned by a company expressed on a per share basis.

Earnings Per Share Disclosure Report EPS data separately for: • Income or Loss from Continuing Operations • Separately Reported Items • discontinued operations • extraordinary Items • Net Income or Loss

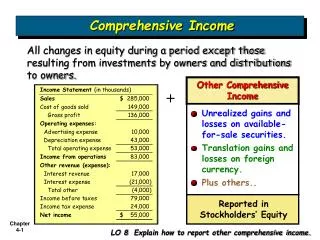

Comprehensive Income An expanded version of income that includes four types of gains and losses that traditionally have not been included in income statements.

Other Comprehensive Income (OCI) Comprehensive income includes traditional net income as well as four additional gains and losses that change shareholders’ equity. • Changes in the market value of certain investments (described in chapter 12). • Gains and losses due to revising assumptions or market returns differing from expectations and prior service cost from amending the plan (described in chapter 17). • When a derivative designated as a cash flow hedge is adjusted to fair value, the gain or loss is deferred as a component of comprehensive income and included in earnings later, at the same time as earnings are affected by the hedged transaction (described in the Derivatives Appendix to the text). • Gains or losses from changes in foreign currency exchange rates. The amount could be an addition to or reduction in shareholders’ equity. (This item is discussed elsewhere in your accounting curriculum).

Includes four possible Other Comprehensive Income items. Includes same four. Includes a fifth possible item, changes in revaluation surplus, from the optional revaluation of property, plant, and equipment and intangible assets. U. S. GAAP vs. IFRS Both U.S. GAAP and IFRS allow companies to report comprehensive income in either a single statement of comprehensive income or in two separate statements. Other comprehensive income items are similar under the two sets of standards.

Accumulated Other Comprehensive Income In addition to reporting comprehensive income that occurs in the current period, we must also report these amounts on a cumulative basis in the balance sheet as an additional component of shareholders’ equity.