Download

1 / 12

140 likes | 269 Views

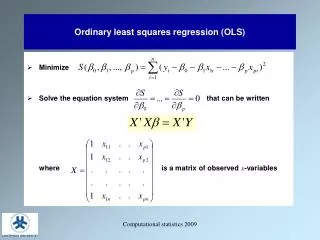

Lecture 8: Ordinary Least Squares Estimation. BUEC 333 Summer 2009 Simon Woodcock. From Last Day. Recall our population regression function: Because the coefficients ( β ) and the errors ( ε i ) are population quantities, we don’t observe them.

E N D

Lecture 8: Ordinary Least Squares Estimation BUEC 333 Summer 2009 Simon Woodcock

From Last Day • Recall our population regression function: • Because the coefficients (β) and the errors (εi) are population quantities, we don’t observe them. • Sometimes our primary interest is the coefficients themselves • βk measures the marginal effect of variable Xkion the dependent variable Yi. • Sometimes we’re more interested in predicting Yi. • if we have sample estimates of the coefficients, we can calculate predicted values: • In either case, we need a way to estimate the unknown β’s. • That is, we need a way to compute from a sample of data • It turns out there are lots of ways to estimate the β’s (compute ). • By far the most common method is called ordinary least squares (OLS).

What OLS does • Recall that we can write:where eiare the residuals. • these are the sample counterpart to the population errors εi • they measure how far our predicted values ( ) are from the true Yi • think of them as prediction mistakes • We want to estimate the β’s in a way that makes the residuals as small as possible. • we want the predicted values as close to the truth as possible • OLS minimizes thesum of squared residuals:

Why OLS? • OLS is “easy” • computers do it routinely • if you had to do OLS by hand, you could • Minimizing squared residuals is better than just minimizing residuals: • we could minimize the sum (or average) of residuals, but the positive and negative residuals would cancel out – and we might end up with really bad predicted values (huge positive and negative “mistakes” that cancel out – draw a picture) • squaring penalizes “big” mistakes (big ei) more than “little” mistakes (small ei) • by minimizing the sum of squared residuals, we get a zero average residual (mistake) as a bonus • OLS estimates are unbiased, and are most efficient in the class of (linear) unbiased estimators (more about this later).

How OLS works • Suppose we have a linear regression model with one independent variable: • The OLS estimates of β0and β1are the values that minimize: • you all know how to solve for the OLS estimates. We just differentiate this expression with respect to β0 andβ1, set the derivatives equal to zero, and solve. • The solutions to this minimization problem are (look familiar?):

OLS in practice • Knowing the summation formulas for OLS estimates is useful for understanding how OLS estimation works. • once we add more than one independent variable, these summation formulas become cumbersome • In practice, we never do least squares calculations by hand (that’s what computers are for) • In fact, doing least squares regression in EViews is a piece of cake – time for an example.

An example • Suppose we are interested in how an NHL hockey player’s salary varies with the number of points they score. • it’s natural to think variation in salary is related to variation in points scored • our dependent variable (Yi) will be SALARY_USD • our independent variable (Xi) will be POINTS • After opening the EViews workfile, there are two ways to set up the equation:1. select SALARY_USD and then POINTS (the order is important), then right-click one of the selected objects, and OPEN -> AS EQUATION or2. QUICK -> ESTIMATE EQUATION and then in the EQUATION SPECIFICATION dialog box, type:salary_usd points c(the first variable in the list is the dependent variable, the remaining variables are the independent variables including the intercept c) • You’ll see a drop down box for the estimation METHOD, and notice that least squares (LS) is the default. Click OK. • It’s as easy as that. Your results should look like the next slide ...

What the results mean • The column labeled “Coefficient” gives the least squares estimates of the regression coefficients. • So our estimated model is:USD_SALARY = 335602 + (41801.42)*POINTS • That is, players who scored zero points earned $335,602 on average • For each point scored, players were paid an additional $41,801 on average • So the “average” 100-point player was paid $4,515,702 • The column labeled “Std. Error” gives the standard error (square root of the sampling variance) of the regression coefficients • the OLS estimates are functions of the sample data, and hence are RVs – more on their sampling distribution later • The column labeled “t-Statistic” is a test statistic for the null hypothesis that the corresponding regression coefficient is zero (more about this later) • The column labeled “Prob.” is the p-value associated with this test • Ignore the rest for now • Now let’s see if anything changes when we add a player’s age & years of NHL experience to our model

What’s Changed: The Intercept • You’ll notice that the estimated coefficient on POINTS and the intercept have changed. • This is because they now measure different things. • In our original model (without AGE and YEARS_EXP among the independent variables), the intercept (c) measured the average USD_SALARY when POINTS was zero ($335,602) • That is, the intercept estimated E(USD_SALARY | POINTS=0) • This quantity puts no restriction on the value of AGE and YEARS_EXP • In the new model (including AGE and YEARS_EXP among the independent variables), the intercept measures the average USD_SALARY when POINTS, AGE, and YEARS_EXP are all zero ($419,897.8) • That is, the new intercept estimates E(USD_SALARY | POINTS = 0, AGE = 0, YEARS_EXP = 0)

What’s Changed: The Slope • In our original model (excluding AGE and YEARS_EXP), the coefficient on POINTS was an estimate of the marginal effect of POINTS on USD_SALARY, i.e., • This quantity puts no restriction on the values of AGE and YEARS_EXP (implicitly, we are allowing them to vary along with POINTS) – it’s a total derivative • In the new model (which includes AGE and YEARS_EXP), the coefficient on POINTS measures the marginal effect of POINTS on USD_SALARY holding AGE and YEARS_EXP constant, i.e., • That is, it’s a partial derivative • The point: what your estimated regression coefficients measure depends on what is (and isn’t) in your model!