Download

1 / 18

180 likes | 313 Views

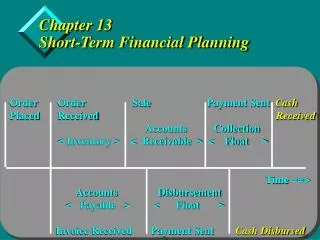

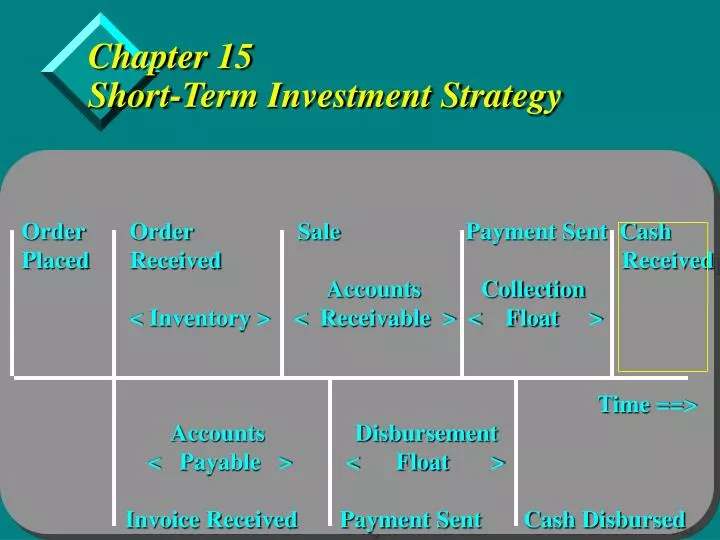

Chapter 15 Short-Term Investment Strategy. Order Order Sale Payment Sent Cash Placed Received Received Accounts Collection

E N D

Chapter 15Short-Term Investment Strategy • Order Order Sale Payment Sent Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • Time ==> • Accounts Disbursement • < Payable > < Float > • Invoice Received Payment Sent Cash Disbursed

Objectives • Define an investment policy and indicate what inputs are used to develop the policy. • Describe the cash and securities allocation decision. • Describe the investment decision-making process. • Calculate portfolio return for the purpose of evaluating portfolio performance. • Indicate how a portfolio manager might assess risk and return tradeoffs.

Short-Term Investment Policy • Defines company’s posture toward risk and return and specifies how it is to be implemented • Possible elements include: • minimal acceptable security ratings • allocation percentage constraints • strategy limitations • maturity limits • authorization and approvals • portfolio performance evaluation

Cash and Securities Allocation Decision • Aggregate investment in cash and securities • Cash and securities mix

Investment Decision-Making Process • Outside management • Selecting portfolio manager • Evaluating portfolio performance • Internal portfolio management

Assembling the Portfolio • General risk-return factors • GNP • Industry-specific events • Interest rate trends • Risk factors revisited • Interrelationships among risk types • Uncertainty of risk estimates • Portfolio risk and the risk-return tradeoff • Assessing the risk-return tradeoff • Short-term investment strategies

Short-Term Investment Strategies • Passive strategies • buy-and-hold • Active strategies • historical yield spread analysis • riding the yield curve • dividend capture strategy • maturity extension swap • yield spread swap

Survey Evidence on Strategies • 47% were aggressive • 34% moderate • 17% conservative • 2% passive

Survey Evidence, continued • 74% of aggressive managers had 75% of excess cash invested. • Passive managers only had 50% invested.

Survey Evidence, continued • Aggressive managers ranked rate of return as most important attribute. • Moderate and conservative managers ranked default risk as most important attribute.

Survey Evidence, continued • Aggressive managers used riding the yield curve much more often (30% usage rate) than did moderate (24% usage rate) or conservative (9% usage rate) managers. • Most popular instruments used were Eurodollar certificates first followed by repurchase agreements and commercial paper.

Summary • Begin investment process by considering the cash forecast, the company’s financial position, and the investment policy. • Decide whether or not to use an outside manager. • The chapter concluded with profiles of passive and active investment strategies.

Cash & Securities Mix Decisions • Baumol • Miller-Orr • Stone

$ Z Time Baumol • Company receives funds periodically, but must disburse monies at a continuous steady rate • Cash needs are perfectly anticipated • Cash balances are replenished by a sale of securities • Similar to the EOQ model Z = (2*F*TCN / k)1/2

Miller-Orr • Assumes cash flow is unpredictable • Permits both upward and downward movements in the cash balance UCL $ Z = (3F2/4i)1/3 UCL = 3Z + LCL LCL + Z LCL Time

Stone • Allows for the cash manager’s knowledge of imminent cash flows to override model directives. • Similar to Miller-Orr in that it has UCL and LCL • ...but before a transaction is made, the expected cash balance is compared to the UCL and LCL and a transaction is made ONLY if the EXPECTED cash balance is beyond these trigger points.

I f the daily cash balance hits UCL or LCL then estimate the cash balance in k days. Stone, continued Then, if the expected cash balance in k days is > adjusted UCL buy secs. If < adjusted LCL then sell secs. $ U C L L C L • T i m e