Download

1 / 14

150 likes | 172 Views

Explore the background and successful implementation of GST in India, including milestones, benefits, and its impact on the economy and stakeholders.

E N D

The Journey of GST • In 2003, Kelkar Task Force on IDT suggested comprehensive GST based on VAT principle • The FM Chidambaram declared in 2006-07 Budget speech that GST will be applicable by 01/04/2010. • As the proposal involved reforming of IDT by both CG and SG, the responsibility of preparing a design and road map was assigned to EC of SFMs (EC). • A joint WG of officers from CG and SG was formed in Sep 2009 • EC released its First Discussion Paper on GST in Nov 2009.

115th Amendment Bill was introduced in LS in March 2011 and referred to parliament for examination and report. • Nov 2012, A committee on GST Design was formed • Based on this, a report was submitted on Jan 2013. • EC in Bhubaneswar meeting decided to constitute 3 committees on GST such as a. Place of supply rules & revenue neutral rates. b. Dual control, Threshold & exemptions. c. IGST and GST on imports. • PSC submitted its report in Aug 2013 to LS. • Recommendations were accepted and draft amendment bill was revised.

Final draft CA Bill were sent to EC and again with recommendations came to Ministry. Then came back to EC in March 2014. • 115th CA bill lapsed with LS dissolution on May 2014. • June 2014 , draft bill sent to EC after approval by Modi Govt. • Dec 2014, 122nd Amendment Bill was introduced in LS on 19.12.2014 and passed on 6.5.2015. • Then referred to RS that submitted report on july 2015 • Aug 2016 bill with fresh amendments passed by RS. • March 2017, GST Council finalizes CGST & IGST bills.

April 2017, parliament passes all 4 GST bills • May 17 council fixed rates on Goods and services except J&K promulgate SGST Act. • 1.7.2017 GST takes effect in India except J&K

Benefits of GST GST is a win-win situation for the entire country. It brings benefits to all the stakeholders of industry, Government and the consumer. It will lower the cost of goods and services give a boost to the economy and make the products and services globally competitive. The significant benefits of GST are discussed hereunder: 1. Creation of unified national market GST aims to make India a common market with common tax rates and procedures and remove the economic barriers thus paving the way for an integrated economy at the national level. 2. Mitigation of ill effects of cascading By subsuming most of the Central and State taxes into a single tax and by allowing a set-off of prior-stage taxes for the transactions across the entire value chain, it would mitigate the ill effects of

cascading, improve competitiveness and improve liquidity of the businesses. Eradication of "tax on tax" & allows cross utilization of input tax credits by making the entire supply chain tax neutral- benefit to industry sector . Elimination of multiple taxes and double taxation: GST will subsume majority of existing indirect tax levies both at Central and State level into one tax i.e., GST which will be leviable goods and services. This will make doing business easier and will also tackle the highly disputed issues relating to double taxation of a transaction as both goods and services. Boost to ‘Make in India' initiative GST will give a major boost to the ‘Make in India' initiative of the Government of India by making goods and services produced in India competitive in the national as well as international market. Buoyancy to the Government Revenue GST is expected to bring buoyancy to the Government Revenue by widening the tax base and improving the taxpayer compliance

1. For overall business sector Easy in compliance process:- As its technology driven. There will be simplified & automated procedure for various processes, such as registration, returns, tax payment etc. 2. Speedy decisions:- As reduced human interface between the tax payer and tax administration though a common portal GSTN 3.More transparency & accountability:- Online electronic verification, matching of input tax credit across India will lead to encourage culture of compliance 4. Harmonized laws, procedures & rates of tax:- This will make compliance easier & simple also lead to greater certainty to taxation system. • .

Reduced compliance cost:- removal of multiple taxation of same transaction will alleviate the need for multiple record keeping for variety of taxes, thus lesser manpower in maintaining records. Gain to manufacturers & exporters As majority of central & state taxes are subsumed in GST with full set off of input goods & services, and complete phase out of central sales tax would reduce the cost of locally manufactured goods. • This will increase the competitiveness of Indian goods and services in the international market and give boost to Indian exports.

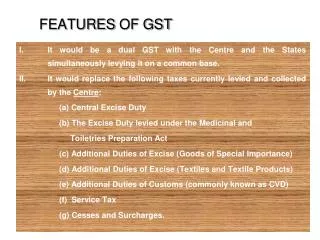

Taxes subsumed under GST • State Levies • VAT/Sales tax • Central Sales Tax (CST) • Entertainment tax (other than levied by local bodies) • Octroi and Entry tax • Purchase tax • Luxury tax • Taxes on lottery, betting, gambling • State surcharges, cesses relating to supply of goods and services • Central Levies • Central excise duty • Additional excise duties • ED under the Medicinal & Toiletries Preparation Act • Service tax • Additional Customs Duty s(CVD) • Special additional duty (SAD) • Surcharges and cesses relating to supply of goods and services.

Taxes - NOT subsumed under GST • Basic Customs Duty • Excise Duty / VAT on Petroleum Products for five years • Excise Duty on Tobacco Products • Electricity Duty by state • Entertainment tax levied by local bodies • State excise on Alcoholic Beverages • Property tax, Stamp Duty and taxes on immovable properties • Royalty on minerals, Environmental / regulatory taxes- e.g. vehicles tax

Overview of GST Service Tax Goods & Service Tax (GST) State Excise Duty Excise Duty Entertainment Tax VAT CST Luxury Tax Octroi Duty Features of GST. GST Council One Nation & One Tax & One Market Events are based on Concept of Supply. Streamlining & Cross Utilization of Input Tax Credits. Revolutionary Invoice Matching Concept. GST Governing Body with power to take decision on rates, exemption, threshold exemptions, etc with 33.33% voting power of Union Government & 66.66% power lies with the State Government.