Download

1 / 2

20 likes | 156 Views

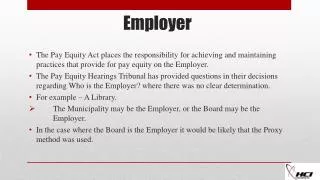

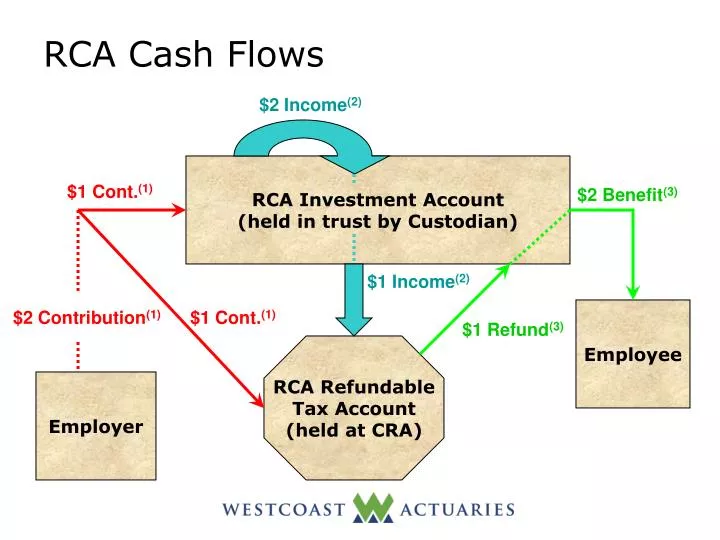

RCA Cash Flows. $2 Income (2). RCA Investment Account (held in trust by Custodian). $2 Benefit (3). $1 Cont. (1). $1 Income (2). Employee. $2 Contribution (1). $1 Cont. (1). $1 Refund (3). RCA Refundable Tax Account (held at CRA). Employer. RCA Cash Flows (Legend).

E N D

RCA Cash Flows $2 Income(2) RCA Investment Account (held in trust by Custodian) $2Benefit(3) $1 Cont.(1) $1 Income(2) Employee $2 Contribution(1) $1 Cont.(1) $1 Refund(3) RCA Refundable Tax Account (held at CRA) Employer

RCA Cash Flows (Legend) (1)When the Employer makes a $2 contribution to the RCA, they would deposit $1 (i.e. 50%) to the RCA Investment Account. They would remit $1 (i.e. the 50% refundable tax) to the RCA Refundable Tax Account held at CRA. (2)When the RCA Investment Account earns $2 of income (interest & dividends and realized capital gains net of realized capital losses) in a calendar year, the RCA Trust would remit the 50% refundable tax on realized investment income (e.g. $1) to the RCA Refundable Tax Account held at CRA upon the filing of the T3-RCA trust return for the calendar year. (3)When the RCA Trust pays $2 of benefits to the Employee on a taxable basis from the RCA Investment Account in a calendar year, CRA would issue a refund of $1 (i.e. the 50% refundable tax) from the RCA Refundable Tax Account to the RCA Trust after their assessment of the T3-RCA trust return for the calendar year.