Download

1 / 15

150 likes | 276 Views

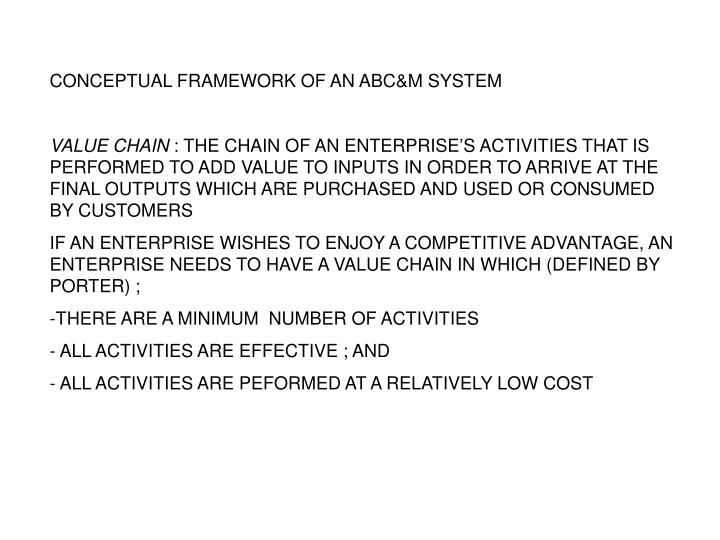

CONCEPTUAL FRAMEWORK OF AN ABC&M SYSTEM VALUE CHAIN : THE CHAIN OF AN ENTERPRISE’S ACTIVITIES THAT IS PERFORMED TO ADD VALUE TO INPUTS IN ORDER TO ARRIVE AT THE FINAL OUTPUTS WHICH ARE PURCHASED AND USED OR CONSUMED BY CUSTOMERS

E N D

CONCEPTUAL FRAMEWORK OF AN ABC&M SYSTEM • VALUE CHAIN : THE CHAIN OF AN ENTERPRISE’S ACTIVITIES THAT IS PERFORMED TO ADD VALUE TO INPUTS IN ORDER TO ARRIVE AT THE FINAL OUTPUTS WHICH ARE PURCHASED AND USED OR CONSUMED BY CUSTOMERS • IF AN ENTERPRISE WISHES TO ENJOY A COMPETITIVE ADVANTAGE, AN ENTERPRISE NEEDS TO HAVE A VALUE CHAIN IN WHICH (DEFINED BY PORTER) ; • THERE ARE A MINIMUM NUMBER OF ACTIVITIES • ALL ACTIVITIES ARE EFFECTIVE ; AND • ALL ACTIVITIES ARE PEFORMED AT A RELATIVELY LOW COST

Figure 2.1 : Porter’s value chain FIRM INFRASTRUCTURE HUMAN RESOURCE MANAGEMENT SUPPORT ACTIVITIES MARGIN TECHNOLOGY DEVELOPMENT PROCUREMENT SERVICE MARKETING AND SALES OUTBOUND LOGISTICS OPERATIONS OUTBOUND LOGISTICS MARGIN PRIMARY ACTIVITIES

FIGURE 2.2 REFLECTS A FEW PROCESSES AND INDICATES WHERE THE ACTIVITIES RELATING TO THEM ARE PERFORMED. PROCUREMENT OF RAW MATERIALS COULD REQUIRE THE FOLLOWING ACTIVITIES : REQUISTIONING, ORDERING, INSPECTION (OF GOODS ON RECEIPT), ISUING OF GOODS RECEIVED NOTES, CONVEYING TO STORES, STORING, CHECKING OF CREDITORS’ INVOICES, AND SETLING CREDITORS’ ACCOUNT. PROCESS : A LOGICAL SERIES ACTIVITIES WHICH CAN BE LINKED TO PRODUCE A RESONABLY HOMOGENOUS OUTPUT OR A SIGNIFICANT AND COMPLETE OUTPUT (NOT NECESSARILY A PRODUCT) PROCESS

FIGURE 2.3 ILLUSTRATES HOW THE SELLING PROCESS IS DEDUCED FROM THE STRUCTURE BY UTILISING THE UNDERLYING ACTIVITIES. ACTIVITY ; ALL THE ACTIONS OR TASKS TO CARRY OUT A CERTAIN WORK ( THE ACTIVITY TO PACK FINISHED GOODS IS CALLED PACKING). ACTIVITY IS USED AS BASIS OF MEASUREMENT OF COST AND PERFORMANCE IN ABC SYSTEM ( ACTIVITY IS THE FOCAL POINT OF TOTAL COST MANAGEMENT) EXAMPLES OF ACTIVITIES : BUYING, RECEIVING, STORING, PACKING, SELLING, INVOICING, DISTRIBUTION, DEBT COLLECTION, CUSTOMER SERVICING. ACTIVITIES CONSUME RESOURCES; IN OTHER WORDS , ACTIVITIES CAUSE COSTS. IN TURN PRODUCTS CONSUME ACTIVITIES

Fugure 2.3 : “Process” in a traditional functional organisation structure MANAGING DIRECTOR SALES DIRECTOR ADMIN DIRECTOR PROCDUCTION DIRECTOR SALES ADMIN CONTROLLER CREDIT MANAGER SALES MANAGER WAREHOUSE MANAGER TRANSPORT MANAGER O R G N I S A T I O N CREDIT CONTROLLER SALES ORDER CLERK INVENTORY CONTROLLER CESPATCH CLERK SALESMAN

A C T I V I T Y OBTAIN ORDER APPROVE ORDER RECORD ORDER APPROVE CREDIT DETERMINE STOCK AVAILABILITY SCHEDULE DELIVERY INITIATE SALE DELIVER GOODS CHARGE CUSTOMER RECEIVE CASH P R O C E S S SELL

FIGURE 2.4 : STRUCTURAL ANALYSIS OF A BUSINESS Primary processes are performed to design, produce, market, deliver, and support products and services Secondary processes enhance the efficiency and effectiveness of the primary processes VALUE CHAIN PROCESS BUSINESS PROCESS A group of interdependent activities which are activated by an event What the business does Activities consume resources Products or services consume activities ACTIVITY TASK How an activity is performed

AFTER HAVING IDENTIFIED THE ACTIVITIES THAT INCUR COSTS AND HAVING ASSIGNED THE COSTS TO THE RELEVANT ACTIVITIES, THE NEXT STEP IS TO DETERMINE THE JUSTIFIED BASES ON WHICH THE COSTS APPROPRIATED TO THE ACTIVITY CENTRES ARE TO BE TRACED TO THE ORGANIZATION’S PRODUCTS. HENCE, IN TERMS OF ABC, THE COST OF A PRODUCT COMPRISES THE COST OF THE RAW MATERIALS PLUS THE COST OF ALL THE ACTIVITIES REQUIRED TO PRODUCE THE PRODUCT. RESOURCES OR COST ELEMENTS ARE ECONOMIC ELEMENTS DIRECTED TOWARDS THE PERFORMANCE OF ACTIVITIES. RESOURCES ARE TRACED TO ACTIVITIES UTILISING THE RESOURCE COST DRIVER. EXAMPLES OF RESOURCES ARE LABOR, POWER AND DEPRECIATION. THE COST DRIVERS COULD BE TIME (FOR LABOR), KILOWATTS CONSUMED (FOR POWER) AND VALUE OF EQUIPMENT EMPLOYED (FOR DEPRECIATION).

PRFORMANCE MEASUREMENT (QUALITY, TIME, COST AND FLEXIBILITY) IS CONSIDERED MORE USEFUL THAN PURE FINANCIAL EVALUATION TO EVALUATE OVERALL ORGANISATIONAL PERFORMANCE. QUALITY MANAGEMENT, PRODUCTIVITY MANAGEMENT SYSTEMS AND CAPACITY MANAGEMENT SYSTEMS CAN THUS BE INTEGRAL PARTS OF AN ACTIVITY-BASED MANAGEMENT SYSTEM • COST DRIVERS CAN BE DEFINED AS THOSE FACTORS OR TRANSACTIONS THAT ARE SIGNIFICANT DETERMINANTS OF COST (THE OUTPUT OF AN ACTIVITY). • EXAMPLE COST DRIVERS : • THE NUMBER OF PURCHASE ORDERS DRIVES THE COSTS OF THE PURCHASING DEPARTMENT. • THE NUMBER OF GOODS RECEIVED NOTES DRIVES THE COSTS OF THE RECEIVING DEPARTMENT. • THE NUMBER OF ITEMS IN STOCK DRIVES THE COSTS OF WAREHOUSING

Figure 2.5 : Activity-based costing (CAM-I) COST ASSIGNTMENT VIEW RESOURCES PROCESS VIEW COST DRIVERS ACTIVITIES PERFORMANCE MEASURES COST OBJECTS

COST OBJECTS : THE FOLLOWING COST OBJECTS, OTHER THAN PRODUCTS, ARE TYPICALLY FOUND IN BUSINESS : • SERVICES • MARKETING CHANNELS • DISTRIBUTION CHANNELS • CUSTOMERS • PROCESSES • ACTIVITIES. • PROJECTS • CONTRACTS OR OTHER WORK UNITS

BILL OF ACTIVITIES (BOA) : DESCRIPTION OF THE ROUTING THE PRODUCT (OR OTHER COST OBJECT) TAKES THROUGH THE ACTIVITIES IN ITS PATH TOWARD COMPLETION. • TABLE 2.2 ILLUSTRATES THAT COST OF A SUBASSEMBLY BY THE ABOVE ACTIVITIES. THE ASSEMBLY TYPICALLY CONSUMES : • TWO UNITS OF PRODUCTION PLANNING • SIX UNITS OF BUYING (MAYBE THE NUMBER OF ORDERS) • TWELVE UNITS OF RECEIVING (MAYBE THE NUMBER OF GRNs • FOUR UNITS OF COMPONENT INSPECTION • EIGHTS UNITS OF ASSEMBLING • THREE UNITS OF FINAL QUALITY INSPECTION; AND • TWNTY UNITS OF STORAGE (MAYBE SQUARE METRES OR DAYS)