Download

1 / 19

190 likes | 259 Views

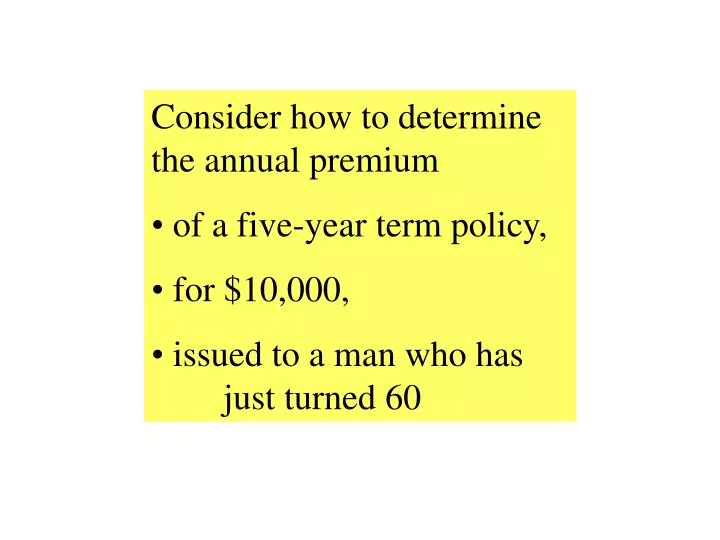

Consider how to determine the annual premium of a five-year term policy, for $10,000, issued to a man who has just turned 60. Year 1. Year 2. Year 3. Year 4. Year 5. Year 6. Age 60. Age 61. Age 62. Age 63. Age 64. Age 65. -10,000. D.

E N D

Consider how to determine the annual premium • of a five-year term policy, • for $10,000, • issued to a man who has just turned 60

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 -10,000 D The insured pays the first premium at the beginning of Year 1. During Year 1, one of two things will happen. Either the insured dies (D), in which case the company pays $10,000 at the end of the year, or the insured survives (S), in which case he pays the second premium at the start of Year 2. +P S +P Year 1

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 -10,000 D During Year 2, again one of two things will happen. Either the insured dies, in which case the company pays $10,000, or the insured survives, in which case he pays the third premium at the start of Year 3. -10,000 +P D S +P S +P Year 2

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 -10,000 D ... and so on during Year 3 ... -10,000 +P D S -10,000 D +P S +P S +P Year 3

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 -10,000 D ...and Year 4... -10,000 +P D S -10,000 D +P S -10,000 +P D S +P S +P Year 4

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 -10,000 The contract ends at the end of Year 5. D -10,000 +P D S -10,000 D +P S -10,000 +P D S -10,000 D +P S +P Year 5 S 0

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 1,558 ... 1,558 are expected to die at age 60... D 1,667 ... 1,667 at age 61 ... 77,861 D S 1,777 ... and so on ... D S 1,885 D S 1,990 D According to the mortality table, of 77,861 men aged 60... S S 70,794 ... while 70,794 are expected to survive age 64.

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 1,558 D 0.0200 1,667 77,861 D S 1,777 D S 1,885 D S 1,990 Therefore, the probability of death at age 60 is 1,558/77,861, or 0.0200. D S S 70,794

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 1,558 D 0.0200 1,667 77,861 D S 0.0214 1,777 D S 1,885 D S 1,990 ... the probability of death at age 61 is 1,667/77,861, or 0.0214. D S S 70,794

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 1,558 D 0.0200 1,667 77,861 D S 0.0214 1,777 D S 0.0228 1,885 D S 0.0242 1,990 ... and so on ... D S 0.0256 S 70,794

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 1,558 D 0.0200 1,667 77,861 D S 0.0214 1,777 D S 0.0228 1,885 D S 0.0242 1,990 D S 0.0256 The probability of surviving age 64 is 70,794/77,861, or 0.8860. S 70,794 0.8860

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 -10,000 D (0.0200) -10,000 +P D S (0.0214) -10,000 D +P S (0.0228) -10,000 +P D S (0.0242) -10,000 D +P S (0.0256) +P S 0 (0.8860)

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 -10,000 ... the company’s net revenue is P-10,000. D (0.0200) -10,000 +P D S (0.0214) -10,000 D +P S (0.0228) -10,000 +P D S (0.0242) -10,000 D +P S (0.0256) If the insured dies at age 60 (and the probability of this event is 0.0200) ... +P S 0 (0.8860)

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 -10,000 ... the company’s net revenue is 2P-10,000. D (0.0200) -10,000 +P D S (0.0214) -10,000 D +P S (0.0228) -10,000 +P D S (0.0242) -10,000 D +P S (0.0256) If the insured dies at age 61 (and the probability of this event is 0.0214) ... +P S 0 (0.8860)

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 -10,000 ... the company’s net revenue is 3P-10,000. D (0.0200) -10,000 +P D S (0.0214) -10,000 D +P S (0.0228) -10,000 +P D S (0.0242) -10,000 D +P S (0.0256) If the insured dies at age 62 (and the probability of this event is 0.0228) ... +P S 0 (0.8860)

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 -10,000 ... the company’s net revenue is 4P-10,000. D (0.0200) -10,000 +P D S (0.0214) -10,000 D +P S (0.0228) -10,000 +P D S (0.0242) -10,000 D +P S (0.0256) If the insured dies at age 63 (and the probability of this event is 0.0242) ... +P S 0 (0.8860)

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 -10,000 ... the company’s net revenue is 5P-10,000. D (0.0200) -10,000 +P D S (0.0214) -10,000 D +P S (0.0228) -10,000 +P D S (0.0242) -10,000 D +P S (0.0256) If the insured dies at age 64 (and the probability of this event is 0.0256) ... +P S 0 (0.8860)

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Age 60 Age 61 Age 62 Age 63 Age 64 Age 65 -10,000 ... the company’s net revenue is 5P. D (0.0200) -10,000 +P D S (0.0214) -10,000 D +P S (0.0228) -10,000 +P D S (0.0242) -10,000 D +P S (0.0256) While if the insured survives age 64 (and the probability of this event is 0.8860) ... +P S 0 (0.8860)