Download

1 / 5

50 likes | 63 Views

This analysis explores the distribution of enrollment in Medicare Advantage plans, the projected growth of enrollment, the cost differences between Medicare Advantage and traditional Medicare, and the concentration of enrollment among a small number of firms.

E N D

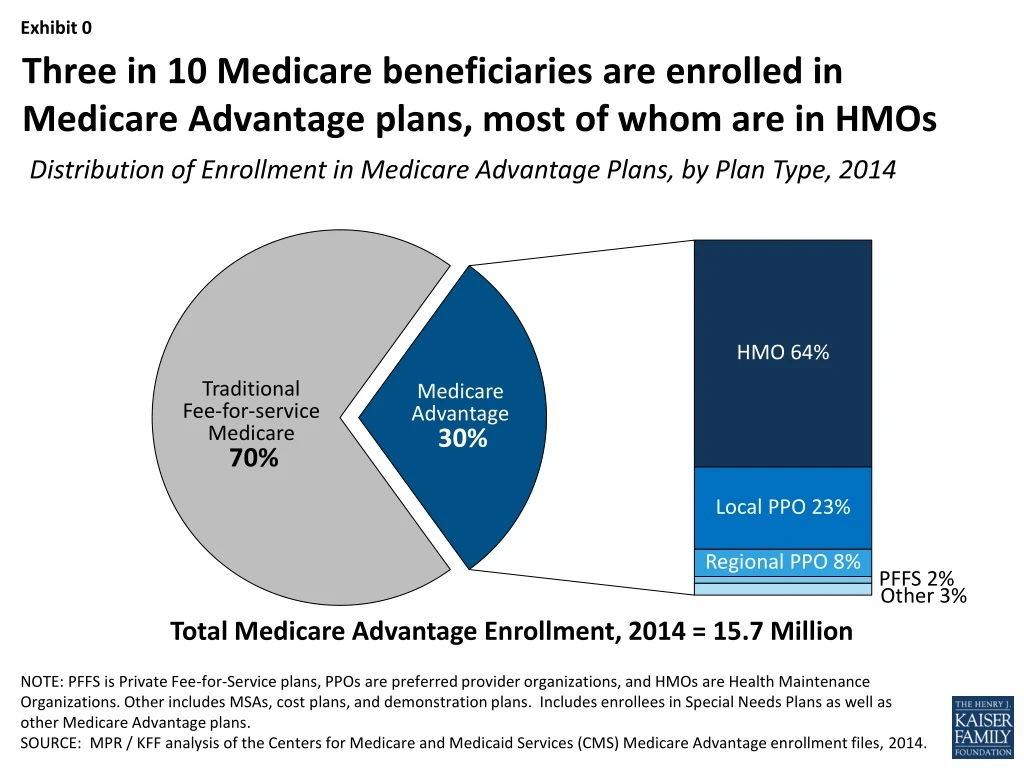

Three in 10 Medicare beneficiaries are enrolled in Medicare Advantage plans, most of whom are in HMOs Distribution of Enrollment in Medicare Advantage Plans, by Plan Type, 2014 Total Medicare Advantage Enrollment, 2014 = 15.7 Million NOTE: PFFS is Private Fee-for-Service plans, PPOs are preferred provider organizations, and HMOs are Health Maintenance Organizations. Other includes MSAs, cost plans, and demonstration plans. Includes enrollees in Special Needs Plans as well as other Medicare Advantage plans. SOURCE: MPR / KFF analysis of the Centers for Medicare and Medicaid Services (CMS) Medicare Advantage enrollment files, 2014.

Medicare Advantage enrollment has increased rapidly and is projected to continue to rise Medicare Advantage Enrollment (in millions), 2005-2024 Actual Enrollment Projected Enrollment NOTE: Includes cost plans, MSAs, demonstrations, and Special Needs Plans, as well as other Medicare Advantage Plans. SOURCE: KFF analysis of the Centers for Medicare and Medicaid Services (CMS) Medicare Advantage enrollment files, 2005-2014, and Congressional Budget Office, “Medicare Baseline,” April 2014.

The share of Medicare beneficiaries in Medicare Advantage plans varies greatly across the country U.S. Average Medicare Advantage Penetration= 30% Anchorage, 0% Portland, 24% Baltimore, 10% Miami, 59% Milwaukee, 34% Manhattan, 32% Idaho Falls, 21% Louisville, 27% Austin, 23% Topeka, 7% Portland, 56% Los Angeles, 43% Tucson, 48% Honolulu, 48% NOTE: Includes cost plans, MSAs, demonstrations, and Special Needs Plans, as well as other Medicare Advantage Plans. SOURCE: KFF analysis of the Centers for Medicare and Medicaid Services (CMS) Medicare Advantage enrollment files, 2014.

Medicare has been paying more for beneficiaries in Medicare Advantage plans than for those in traditional Medicare Average Medicare Advantage Payments as a Percentage of Traditional Medicare Spending Actual Projected Traditional Medicare Spending SOURCE: Medicare Payment Advisory Commission (MedPAC) Report to Congress, 2006-2014.

Medicare Advantage enrollment is concentrated within a small number of firms and affiliates, 2014 Other National Insurers5% Cigna3% Aetna7% Kaiser Permanente 8% Total Medicare Advantage Enrollment, 2014 = 15.7 Million NOTE: Other includes firms with less than 3% of total enrollment. BCBS are BlueCross BlueShield affiliates and includes Wellpoint BCBS plans that comprise 4% of all enrollment (approximately 600,000 enrollees) in Medicare Advantage plans. Other national insurers includes approximately 428,000 enrollees across the following firms: Wellcare, HealthNet, Universal American, Munich American Holding Corporation, and Wellpoint non-BCBS plans . Accounts for merger between Coventry and Aetna in 2013; Medicare Advantage plans offered by Coventry covered 306,000 beneficiaries and Aetna plans covered 615,000 in 2013. Percentages may not sum to 100% due to rounding. SOURCE: MPR/Kaiser Family Foundation analysis of CMS Enrollment files, 2014.