Download

1 / 8

80 likes | 168 Views

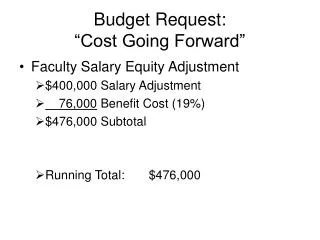

Indirect Cost Recovery Request for Supplementary Appropriation Program-Budget 2013. Secretariat for Administration and Finance. Background. AG/Res. 2756 (XLII-O/12) – General Standards were modified for purposes of determining annual budget ceiling of ICR Fund General Standards Article 80.i.i

E N D

Indirect Cost RecoveryRequest for Supplementary AppropriationProgram-Budget 2013 Secretariat for Administration and Finance

Background • AG/Res. 2756 (XLII-O/12) – General Standards were modified for purposes of determining annual budget ceiling of ICR Fund • General Standards Article 80.i.i • “…[ICR budget] proposal shall be based on projected revenue equivalent to 90% of the average ICR obtained in the three years immediately preceding the year in which the Program-Budget is adopted and shall be applied to the subsequent three years … The average shall be reviewed every three years…” • Therefore, budget ceiling for years 2013-2015 were calculated based on the ICR revenue obtained in 2009-2011

Background Calculation of ICR Budget Ceiling for Fiscal Years 2013-2015 (in thousands of USD) • AG/Res. 1 (XLIII-E/12) – Established overall budget ceiling for ICR fund expenditures at a level not to exceed USD 5,250,000.

Consideration 1 • Member States have made significant multiyear commitments for years 2013 – 2015 • In 2013 we estimate these projects may bring as much as USD 434K in additional ICR revenue

Consideration 1 • Additional Administrative Support Service • The General Secretariat will be required to provide additional administrative support services for these projects and incur extraordinary expenditures not previously contemplated in the Approved 2013 Program-Budget • Estimated expenditures to provide additional administrative support services for these projects in 2013 amount to approximately USD 67 thousand

Consideration 2 • Actual Personnel Cost Higher than Budgeted • Actual cost financed by ICR Fund during 2013 are projected to exceed the approved 2013 Program Budget, primarily due to required reclassifications, additional post, special duties assignments, required consultants, benefits and tax reimbursement. • Projected increase in 2013 actual personnel costs are approximately USD 559 thousand, plus the USD 67 thousand previously identified for additional administrative support services (a total of USD 626 thousand).

Proposal • The General Secretariat needs budgetary authorization to finance these expenses and requests a supplementary appropriation for the 2013 ICR budget of USD 390,500, equivalent to 90% of the projected additional ICR revenue to be received in 2013. • The General Secretariat will have to manage expenditures to not exceed budget ceiling and eliminate the amount of USD 235.5K, which is the difference between the increased amount of projected expenditures (USD 626K, which includes the additional administrative support services of USD 67K) and the supplementary appropriation amount requested (USD 390.5K). • Any unused appropriations shall be returned to the Reserve Subfund of the ICR fund. • The General Secretariat will continue to report periodically to the Permanent Council through the CAAP, the status of the ICR fund through the quarterly management reports.

ICR projection • ICR Projection for 2013 • ICR Collection based on average ICR collected in 2012 and 2011 plus additional projected income • Projected expenditures based on approved budget USD 5,250 + USD 390.5 • If General Secretariat executes budget at the new approved level, the ending balance of the ICR for 2013 is projected to be approximately USD 217.5K, similar to year 2012.