Download

1 / 20

200 likes | 350 Views

A Transaction Cost Approach to Make-or-Buy Decisions. Gordon Walker and David Weber. Presenter: Wen ZHENG. Research Question. Apply transaction cost framework to investigate make-or-buy decisions for relative simple components in a manufacturing division of a large U.S. automobile company .

E N D

A Transaction Cost Approach to Make-or-Buy Decisions Gordon Walker and David Weber Presenter: Wen ZHENG

Research Question • Apply transaction cost framework to investigate make-or-buy decisions for relative simple components in a manufacturing division of a large U.S. automobile company. • Transaction cost • Production Cost

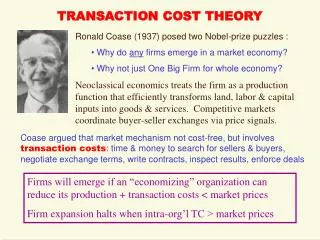

Theory and Hypothesis • Williamson (1981) • Production cost (ΔPC) • Buyers’ production Cost -Supplier’s production cost • Transaction cost • Transaction cost of buy -Transaction cost of make

Theory and Hypothesis • Williamson (1981) • Make or buy=f(asset specificity * uncertainty) • Walker and Weber (1984) • Make or buy= f(asset specificity, uncertainty)

Theory and Hypothesis • Williamson (1981) • Make or buy=f(asset specificity * uncertainty) • Walker and Weber (1984) • Make or buy= f(asset specificity, uncertainty) Supplier Market Competition Volume uncertainty Technological Uncertainty

Theory and Hypothesis H1 H2 H3 H4 H5 H7 H6 H8

Empirical Test • Sample • 60 decisions made in a component division of a large U.S. automobile manufacture over a period of three years • Method • Structure Equation Model (SEM) • Unweighted Least Squares (ULS)

Variables Supplier Competition Buyer Experience Volume Uncertainty Supplier Advantage Technological Uncertainty

Results H3 H5 H7 H2 H1

Results H4

Results H6 H8

Result • H1, H3, H4, H5 and H8 are corroborated • Transaction cost (TC) > Production Cost (PC) • Market Competition TC make/buy > PC make/buy • Volume Uncertainty TC > Technological Uncertainty TC • Buyer Experience PC • Buyer Experience make/buy • Technological Uncertainty make/buy

Result • H1, H3, H4, H5 and H8 are corroborated • Transaction cost (TC) > Production Cost (PC) • Simplicity • Division outcomes > Functional outcomes

Result • H1, H3, H4, H5 and H8 are corroborated • Transaction cost (TC) > Production Cost (PC) • Market Competition TC make/buy > PC make/buy • Method bias • Implicit Assumption: the cost of administrating interfunctionalcoordination within the firm were virtually independent of the transaction cost associated with contracting in the market

Result • H1, H3, H4, H5 and H8 are corroborated • Transaction cost (TC) > Production Cost (PC) • Market Competition TC make/buy > PC make/buy • Volume Uncertainty TC > Technological Uncertainty TC • Simplicity • Buyer pay retooling and both parties pay the changes in volume • Scale economies may be crucial for suppliers

Result • H1, H3, H4, H5 and H8 are corroborated • Transaction cost (TC) > Production Cost (PC) • Market Competition TC make/buy > PC make/buy • Volume Uncertainty TC > Technological Uncertainty TC • Buyer Experience PC • Simplicity

Result • H1, H3, H4, H5 and H8 are corroborated • Transaction cost (TC) > Production Cost (PC) • Market Competition TC make/buy > PC make/buy • Volume Uncertainty TC > Technological Uncertainty TC • Buyer Experience PC • Buyer Experience make/buy • Technological Uncertainty make/buy Poor communication within the division of important information for contracting with suppliers

Discussion • Weakness • Small sample size drawn from a single corporate division limit the generalizability of the empirical findings • Relative simplicity of the components studied may explain to some extent the failure of part of the model • Method Bias: The component manager answers questions about both supplier market competition and supplier production cost advantage • Future Research • Other forms of buyer-supplier relationships (e.g. tapered integration, joint venture, and the type of coordination and dedicated supply called “kanban” by the Japanese)