Download

1 / 20

200 likes | 347 Views

Essential Health Benefits and QHP Selection Process Recommendations. Health Care Commission September 6, 2012. www.pcghealth.com. Agenda. Governance Model Revision Update: Exchange Timeline through January 2014 Essential Health Benefits Benchmark Recommendation

E N D

Essential Health Benefits and QHP Selection Process Recommendations Health Care Commission September 6, 2012 www.pcghealth.com

Agenda • Governance Model Revision • Update: Exchange Timeline through January 2014 • Essential Health Benefits Benchmark Recommendation • QHP Selection Process Recommendation

Governance Model Revision • In late 2011, the Federal government released new options for States to consider in establishing a Health Benefit Exchange (Exchange) • These new options, as clarified through federal rule making, allowed States to enter into a partnership with the Federal government. • States in a partnership could choose to retain Plan Management functions, Consumer Assistance functions, or both. The Federal government would administer all other functionality, most notably the large technical infrastructure to support Exchange operations. • Prior to the release of these new options, the Health Care Commission carried a motion to recommend a State-based Exchange for Delaware. • At the time of this vote, the alternatives were to cede all functionality to the Federally-Facilitated Exchange or find other States with which to create a regional Exchange. • Of these options, the most viable choice was to pursue a State-based model • Following the release of the Partnership model, DE re-assessed the financial viability of all available options and determined that the State-Federal Partnership is the most appropriate choice.

Update: Exchange Timeline September 2012: • Final recommendation on Essential Health Benefits benchmark submitted to HHS • Final recommendation on Qualified Health Plan (QHP) selection process October 2012: • Final recommendations on all QHP policies, including certification criteria and other standards related to plan management functionality • Final recommendations for Navigator and In-Person Consumer Assisters certification criteria and phased approach to Outreach and Education • Continue activities to engage Consumer Assistance and Outreach partners in planning process November 2012: • Finalize draft QHP process, rating criteria, and certification application • Finalize readiness checklists and training materials for Navigators and In-Person Assisters • Submit Declaration Letter confirming Exchange model to HHS

Update: Exchange Timeline December 2012 • Exchange readiness review conducted by Federal government January 2013 – March 2013 • Exchange readiness complete. • State moves forward with operational implementation of plan management and consumer assistance functionality March 2013 • Begin accepting QHP applications April 2013 – October 2013 • Launch full outreach and education campaign in preparation for open enrollment October 2013 • Open enrollment begins for QHP plans through the Exchange January 2014 • Plan coverage year commences

Essential Health Benefits • The Affordable Care Act requires that any health insurance plan offered to an individual or small business must meet certain standards. • These standards, known as essential health benefits, must cover the ten broad categories of services listed below. • This list applies to health insurance plans offered inside and outside of the Exchange and represents the minimum services that must be covered. Health insurance plans may cover additional services at their own discretion. • Essential Health Benefit (EHB) Service Categories 1. Ambulatory patient services 2. Emergency services 3. Hospitalization 4. Maternity and newborn care 5. Mental health and substance use disorder services, including behavioral health treatment 6. Prescription drugs 7. Rehabilitative and habilitative services and devices 8. Laboratory services 9. Preventive and wellness services and chronic disease management 10. Pediatric services, including oral and vision care

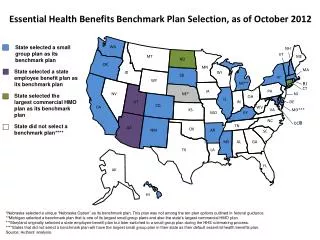

Essential Health Benefits The State has the option to choose an Essential Health Benefits benchmark from among several options • The three largest small group insurance products in Delaware: • Blue Cross Blue Shield (BCBS) Exclusive Provider Organization (EPO)* • Blue Cross Blue Shield (BCBS) Health Maintenance Organization (HMO) • Coventry Point of Service (POS) • The three largest state employee health benefit plans in Delaware: • Comprehensive Preferred Provider Organization (PPO) • HMO • Consumer Directed Health (CDH) Gold • The three largest federal employee health benefit plans: • Blue Cross/Blue Shield FEHP Standard Option • Blue Cross/Blue Shield FEHP Basic Option • Government Employees Health Association (GEHA) Plan *The BCBS Small Group EPO plan currently has the largest enrollment of the small group options

Essential Health Benefits To support this decision, the State conducted the following stakeholder data collection process: • Posted analysis of benchmark options along with supporting background material to the HCC website and issued press releases and email blasts to spread awareness of the process • 45 day public comment period started in June • 2 public forums hosted in Dover to answer questions and discuss options • 54 attendees total for the two forums • Received 45 written comments through the HBE Inbox and the Health Care Commission during the comment period • Comments received through this process are summarized on the following slides by category

Essential Health Benefits Cost, Affordability, and Design • Inclusion of only those benefits traditionally identified as necessary to compromise a group market-accepted program. Benefits other than those mandated by DE law, and those not included in most common DE employers plans should not be included. • Inclusion of quantitative limits (visit/day limits/per procedure limits) wherever appropriate • Additional benefits should utilize treatment limitations to maintain affordability • Plan should not have excessive cost-sharing requirements to protect consumers from unexpected financial obligations • Allow maximum flexibility regarding actuarially equivalent substitutions within benefit categories, and provide clarity indicating how and under what circumstances substitutions may be made • Ensure that plans do not utilize benefit design flexibility to discriminate against vulnerable, high-cost consumers • Allow flexibility in plan design and permit substitutions, continue to allow insurers to use appropriate care management and health promotion tools • Work with insurers to manage the product and rate filing process • Consistency in design through 2015 • Establish clear and meaningful standards for comparing QHPs to the benchmark plan

Essential Health Benefits Chronic Disease Cancer • Access to oral and IV administered chemotherapy, stem cell transplant and radiation therapy. • Equal treatment of patients receiving IV, injectable, and/or orally administered treatments • Coverage for treatment at National Cancer Institute (NCI) cancer centers • Prescription drug benefit that offers full coverage of 6 protected classes (>1 per class) • Balanced coverage and affordable access for all aspects of cancer treatment: preventive care to diagnostic tests to treatment options (targeted therapies, palliative care, hospice) • Monitor the use of tiered networks that may discriminate against specialty drug needs • Breast cancer screenings for women and men Multiple Sclerosis • Access to inpatient hospital services without caps for people with chronic illnesses • Protections from discrimination against specialty medications placed on a fourth, or specialty tier with different cost-share structure • Allow for the number of physical therapy visits to be determined by physical therapist or patient’s doctor, rather than having a predetermined limit

Essential Health Benefits Chronic Disease cont. Hemophilia • Access to specialists at federally recognized hemophilia treatment centers (HTCs) • Access to full range of FDA approved clotting factor products • Access to range of specialty pharmacy providers • “Medical necessity” should not be defined by insurers, but determined by physicians in conjunction with the patient. • Coverage for screening of von Willebrand Disease in cases of women with menorrhagia Cardiovascular Disease • Cardiac rehabilitation, diabetes screening and self management, nutrition counseling, and smoking cessation • Continued monitoring of adequacy and quality once EHB plan is implemented Disabilities • Coverage of assistive technology, home health and personal care services, and medical transport • Culturally sensitive outreach materials that meet the needs of those with specific disabilities • Consideration of medical expenses when determining income guidelines for health exchange • Easily accessible healthcare facilities, offices, and equipment for patients with disabilities (exam tables, scales and radiological machines, etc)

Essential Health Benefits Children • Early Periodic Screening Diagnosis and Treatment (EPSDT) is the most appropriate benefit package for children based on children’s clinical needs • Inclusion of oral and vision care in the Pediatric Services benefit • Inclusion of pediatric and dental benefits that are primarily preventive or screening services • Inclusion of non-cost considerations in establishing EHB – investments in children through preventive services, screenings, etc that reduce health care spending over long term • “Medical necessity” requirements found in the Medicaid program are most appropriate definition for children • Coverage for in-home personal care, mobility-related devices and other durable medical equipment • Age not to be used as basis for limiting services • Utilize small employer model for pediatric oral health services benchmark • Broad access to all dental plans offering the required benefits and meeting qualification standards inside the Exchange • Coverage for medical food and formula for children affected by Phenylketonuria (PKU) • No limits on visits to physical therapy, occupational therapy, speech therapy

Essential Health Benefits Women and Reproductive Health • Robust coverage of pregnancy and maternity benefits such as preconception care, prenatal, labor and delivery, postnatal, postpartum care, breastfeeding, and mental health for postpartum depression. • Coverage of habilitative services to cover early intervention services for premature infants and other children with special health care needs • Coverage for gynecological visits, lab testing, as well as indicated treatment for infections • Coverage of assisted reproductive technologies and voluntary sterilization for men and women • Screenings, counseling, and treatment for all STDs for men and women Hospice and Palliative Care • Coverage of hospice and palliative care Preventive Care • Coverage of tests and services needed to prevent, detect and treat the early onset of disease • Exclusion of expensive benefits that only impact a few

Essential Health Benefits Behavioral Health • Inclusion of strong mental health benefits – Mental Health Parity and Addiction Equity Act covers 8 diagnoses of serious mental illness (SMI), with addition of substance use disorders (SUDs) • Robust and routine outpatient benefits for mental health and substance abuse services • Support of inpatient hospital services for acute mental illness, medically supervised detox, psychotropic and addiction medications, behavioral therapy, habilitation and rehab services, screening, education and self management, intensive case management and ACT teams, peer support services, SBIRT: Screening, Brief Intervention and Referral to Treatment • Screening for mental disorders in primary health care, across the life span and in connection to treatment and support systems Prescription Drugs • Assure provider and patient choice of medicines • Do not impose “one drug per class” rule for it may not meet patient’s clinical needs, and is likely to lead to discriminatory benefit designs

Essential Health Benefits Chiropractic Services • Inclusion of chiropractic network and services found to increase the health of the general population, score high on patient satisfaction and proven cost effective. Dietician/Nutritional Services • Coverage of Medical Nutrition Therapy (MNT) by Registered Dietitians and Licensed Dietitian/ Nutritionists • Exclude pre-authorization or medical review requirement (beyond physical referral) for MNT • Inclusion of unlimited number of visits with a Registered Dietician for children and adults • Alternative: minimum of 6 visits with an RD/LDN per condition per year, with additional visits as needed with physician referral • Adequate nutrition coverage, allowing for proactive treatment of disease conditions such as diabetes, hypertension, and obesity • Coverage for home infusion including enteral nutrition support (tube feedings)

Essential Health Benefits Which plan is the best fit for stakeholders? • 6 stakeholders specified a plan option in their comments, the majority of which support the BCBS small group option: • Either BCBS option under Small Group Plans • BCBS Standard and the BCBS Basic Plans (federal plans) • BCBS small group • BCBS Small Group or State Employee Plans • Least expensive BCBS small group plan • BCBS Small Group HMO Plan + FEDVIP for pediatric • Some concerns mentioned are not possible under current guidance (requiring EPSDT, restricting cost sharing, broadening provider networks, requiring services that are not included in any benchmark) • The small group plans are also the least expensive options in terms of premium. Among the small group options, premiums are comparable. • Small group and State Employee benchmarks cover all insurance mandates passed before December 2011.

Essential Health Benefits Recommendation: Based on stakeholder feedback received, the BCBS Small Group EPO plan option should be Delaware’s benchmark plan for the individual and small group market in 2014 and 2015. This recommendation will be supplemented to provide EHB categories such as pediatric dental/vision and habilitative services once final guidance has been issued by HHS on supplement options.

QHP Selection Process The State has two options to select health plans for inclusion in the Exchange • Select health plans through a procurement-style process (otherwise known as selective contracting): • State issues an RFP. • Health plan issuers respond with their product and pricing details. • State chooses plans from the pool of applicants for inclusion in Exchange. • Select health plans through a certification process: • State sets certification standards for qualified health plans. • Health plan issuers submit product and pricing information for review. • State reviews plans to ensure that certification, pricing, and accreditation standards are met. • Plans that meet all criteria are included in the Exchange.

QHP Selection Process CCIIO has stated that, for States participating in the full FFE, the federal government will pursue a certification process using the federal minimum standards. • There will also be two multi-State plans chosen by the federal Office of Personnel Management (OPM) offered on every Exchange • OPM plans will be certified using the same process and criteria as the FFE Recommendation: The State pursue a certification process for the Exchange • Certification standards will likely include provisions that go beyond the federal minimum to ensure that Delaware’s insurance market is protected from adverse selection while contributing to the achievement of the State’s health care goals. • Final recommendations on certification standards will be presented during the October Health Care Commission meeting.

Public Consulting Group, Inc. 148 State Street, Tenth Floor, Boston, Massachusetts 02109 (617) 426-2026, www.publicconsultinggroup.com