Download

1 / 21

210 likes | 317 Views

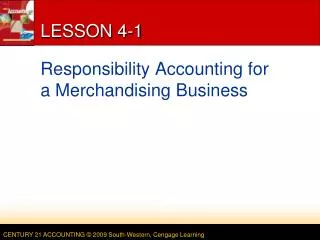

LESSON 4-1. Preparing a Chart of Accounts. TERMS REVIEW. page 95. Ledger – a group of accounts general ledger – ledger that contains all accounts needed to prepare financial statements account number – the number assigned to an account

E N D

LESSON 4-1 Preparing a Chart of Accounts

TERMS REVIEW page 95 • Ledger – a group of accounts • general ledger – ledger that contains all accounts needed to prepare financial statements • account number – the number assigned to an account • file maintenance – Procedure for arranging accounts in a general ledger, assigning account numbers and keeping records current • opening an account – writing an account number and title on the heading of an account LESSON 4-1

Balance columns RELATIONSHIP OF A T ACCOUNT TO AN ACCOUNT FORM page 91 LESSON 4-1

CHART OF ACCOUNTS page 92 LESSON 4-1

ACCOUNT NUMBERS page 92 LESSON 4-1

OPENING AN ACCOUNT IN A GENERAL LEDGER page 94 1 2 1. Write the account title. 2. Write the account number. LESSON 4-1

LESSON 4-2 Posting Separate Amountsfrom a Journal to aGeneral Ledger

TERM REVIEW page 99 • Posting – transferring information from a journal to a ledger LESSON 4-2

1 5 3 2 4 POSTING AN AMOUNT FROM A GENERAL DEBIT COLUMN page 96 1. Write the date. 4. Write the new account balance. 2. Write the journal page number. 5. Return to the journal and write the account number. 3. Write the debit amount. LESSON 4-2

1 5 2 3 4 POSTING A SECOND AMOUNT TO AN ACCOUNT page 97 1. Write the date. 4. Write the new account balance. 2. Write the journal page number. 5. Return to the journal and write the account number. 3. Write the debit amount. LESSON 4-2

5 1 3 2 4 POSTING AN AMOUNT FROM A GENERAL CREDIT COLUMN page 98 1. Write the date. 4. Write the new account balance. 2. Write the journal page number. 5. Return to the journal and write the account number. 3. Write the credit amount. LESSON 4-2

LESSON 4-3 Posting Column Totalsfrom a Journal to aGeneral Ledger

Check mark indicates that amounts ARE NOT posted individually. Check mark indicates that general amount column totals ARE NOT posted. CHECK MARKS SHOW THAT AMOUNTS ARE NOT POSTED page 100 LESSON 4-3

3 5 1 2 4 POSTING THE TOTAL OF THE SALES CREDIT COLUMN page 101 1. Write the date. 4. Write the new account balance. 2. Write the journal page number. 5. Return to the journal and write the account number. 3. Write the column total. LESSON 4-3

1 2 3 5 4 POSTING THE TOTAL OF THE CASH DEBIT COLUMN page 102 1. Write the date. 4. Write the new account balance. 2. Write the journal page number. 5. Return to the journal and write the account number. 3. Write the column total. LESSON 4-3

3 1 5 2 POSTING THE TOTAL OF THE CASH CREDIT COLUMN page 103 4 1. Write the date. 4. Write the new account balance. 2. Write the journal page number. 5. Return to the journal and write the account number. 3. Write the column total. LESSON 4-3

LESSON 4-4 Completed Accounting Forms and Making Correcting Entries

JOURNAL PAGE WITH POSTING COMPLETED page 105 LESSON 4-4

MEMORANDUM FOR A CORRECTING ENTRY page 108 LESSON 4-4

November 13. Discovered that a payment of cash for advertising in October was journalized and posted in error as a debit to Miscellaneous Expense instead of Advertising Expense, $140.00. Memorandum No. 15. 1 Date 2 Debit 4 Source Document 3 Credit JOURNAL ENTRY TO RECORD A CORRECTING ENTRY page 108 LESSON 4-4

TERM REVIEW page 109 • correcting entry – journal entry used to correct a previously incorrect entry LESSON 4-4