Download

1 / 37

370 likes | 552 Views

The Hague and UNIDROIT Conventions. Anayansy Rojas Chan. Conventions. The Hague Conference on Private International Law Convention on the law applicable to certain rights with respect to securities held with an intermediary . (2006)

E N D

TheHague and UNIDROIT Conventions Anayansy Rojas Chan

Conventions • TheHagueConferenceonPrivate International Law • Convention on the law applicable to certain rightswithrespecttosecurities held with an intermediary.(2006) • International Institutefortheunification of PrivateLaw. UNIDROIT • The UNIDROIT convention on substantive rules applicable to intermediated securities. (2009)

Nature ofInstitutions • TheHagueConferenceonPrivateLaw and UNIDROIT. • Intergovernmentalorganizationsthatdevelop multilateral legal instrumentsthatrespondtocontemporaryneeds of privatelaw. • Progressiveunification of the rules of privateinternationallaw.

Environment • Fundamental changes over the last decades of the holding system and representation of securities: • Dematerialization of securitytitle • Book-entryor Global Certificate. • International Expansion of theindirect holding systemormultilevel. • Sets off thedirect link betweenissuer and investor. Substitutedbydealer. (Intermediatedsecurities)

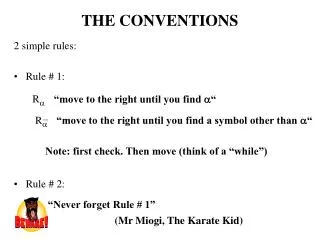

IndirectHolding System • InvestorsmaintaininvestmentswithdealerA), (banksorbrokeragefirms). • Dealer A) mantainstheiraccounts with another dealer B). • Dealer B)- mantainstheiraccountswith a global custodianor international central securities depository. • Eachlevelislocated in a differentjurisdiction.

ICSD Dealer /Participant Issuer - Deposits issue Custodian / participant Dealer Dealer Dealer Clients Clients

Characteristics ofIndirect Holding • There is no identifiable legal relationship between the investor and the issuing agent. • It presents a plurality of legallyindependent relationships that arise at every stage of the holding. • It is common that the dealers hold the securities in fungible omnibus accounts. In the higher level the end investor is not identifiable.

LegalChallenges • What type of rightsdoes the investor have? • Isit a proportionalrighton a fungible mass of securitiesheldwiththedealerwithwhomitwascontracted? • What right doestheyhave if the dealer holds the securities through another dealer?

LegalChallenges • Theright of theendinvestor, isit of propertyorobligation? • Theroman civil jurisdictions and common law, presentdifferent legal treatment. Notalways compatible. • Acquisition of property of securities. • Insolvencyorbankruptcy of thedealer. • Constitution of collateral. • Extendingthe concept of security.

ConventionObjectives • Unifythe legal treatment in thedescribedchanges. • THE HAGUE- purpose to determine certainty onthe law that applies to the constitution and perfection of the collateral in cross-border transactions. • UNIDROIT- aspects of substantive rules of theintermediatedsecurities.

TheHagueConvention Onthelawapplicabletocertainrights in respect of securitiesheldwithanintermediary.

Conflict ofLaws • PURPOSE • To determine thelawapplicableto a loan withcollateralonaninternational portfolio of securities and shares. • Securities are heldbytheborrowerthrough: • Differentlevels of participants: dealers, custodians and central depositories. • Domiciled in different jurisdictions.

ToConsider: • Traditionally, propertyrightsinvolved, are defined in accordancetothe legal system of each country, no contractapplies. • PrincipleLex Rei Sitae o Lex Situs (Lawwherethesecurityislocated) • Theissuers of thesecurities of the portfolio are scatteredaroundtheworld.

TraditionalTreatment • It is called theLooking Through approach • A traditionalanalysisconsiderstherange of securitiesthatformthe portfolio granted in guarantee and willanalyzetheconflict of laws, in accordancewitheachgroup of securities.

Howdoesitapply? • For securities incorporated inphysical form, the local law of the physical location of the title applies. • Securitiesrepresentedbyelectronicbook-entry. To find the security look for the issuer registration because it is where the security is immobilized. • Involves searching through the different levels and registrations of the dealers until reaching the issuer. • Once registration is located, the Lex Rei Sitae applies.

Disadvantages of theApproach • Ina multi-jurisdictional portfolio of securities,if the operator wants to ensure the real jurisdictional extent of the transactiontheymust comply with the legal requirements demanded by the registration law of the issuer. • Thereisuncertainty in countriesontheapplicablelaw: • Law of the place of theissuer. • Law of the place of theregistration of theissuer. • Law of the place of thesecuritiesdeposit.

The HagueProposal • It proposes a legal solution based on the dealer´sregistrations of the intermediary. • PRIMA (Place of the relevant intermediary approach) • Principle seeks to reflect the reality of the indirect holding system of securities.

PRIMA • Basic Principle: • When the securities are held through an intermediarydealer, the law that applies to the rights derived from electronic book-entries is the one established in the agreement between the investor and the dealer intermediary. • Lexcontractusapplies Law designated by the account holder and the dealerintermediary in the contract of the securities account. (Art. 4)

Reality Test • TheConventionestablishescertain rules to determine theapplicablelawwhenit has notbeenestablished in thecontract. • The law of the country where the office of the financial entity with which the contract was perfected is located. • Otherwise the law of the country where the dealerintermediary is constituted or operates.

Conclusions Signedby: • Switzerland(ratified) • USA (not ratified) • Mauritius(ratified) • Whatistheimpact of thisConventionfromtheperspective of the central securitiesdepository?

UNIDROIT Convention On substantive rules applicabletointermediatedsecurities.

Purposes of theConvention • Modernization and creation of uniform rules onsubstantive aspects of thelawapplicabletothe holding and transfer of cross-bordersecurities. • Search of compatibilitywhenappliedtodifferent legal holding systems. • Functional approach: use of neutral language and formulation of rules based on facts and effects, not on legal concepts.

UNIDROIT Convention • Chapter I-Definitions, sphere of application and interpretation. • Chapter II- Rights of theaccountholder. • Chapter III-Transfer of intermediatedsecurities. • Chapter IV-Integrity of theintermediated holding system. • Chapter V-Specialprovisions in relationtocollateraltransactions. • Chapters VI y VII- Transitional and final provisions.

MainConcepts of the Convention • Intermediatedsecurities • Securitiesaccountand • Dealer Intermediary • Thesethreeconceptsestablishthemainsphere of application of theConvention.

IntermediatedSecurities • Itisthemainfocus of theConvention. • Intermediatedsecurity holding presents a change in the concept of legal and real ownership of theinvestor: • The representation of the rights comes from the book-entries administered in a decentralized form by dealersintermediaries in one or more levels of intermediation.

IntermediationRisk Management • What right does the participant have of a in anintermediated structure? • Applytraditionalright of securitytitle: • Investor may lose thesecurities in case of insolvency of thedealer in control of them. • Theapplicablelawconsidersthattheendinvestordoesnotholdthephysicalsecurity, theinvestordoesnotappear in theregistrations of theissuer.

IntermediatedSecurity Concept • Article 1.b)- • Intermediatedsecurities: • means securities credited to a securities account or rights or interests in securities resulting from their book-entry to a securities account • SECURITIES • RIGHTS or • INTERESTS

SecuritiesAccount • c)- securities account: refers to an account maintained by andealer intermediaryto which securities may be credited or debited; • Thisdefinitionmayapplyto: • Account of an intermediary on behalf of a non-intermediary. • Account of anintermediaryon behalf of anotherintermediary. • Account of a centralized depositcentral securities depository on behalf of anintermediary.

Intermediary • d)-intermediary: means a person (including a central securities depository) who in the course of a business or other regular activity maintains securities accounts for others or on behalf of others and on their own and is acting in said capacity; • The application of the Convention requires that at least oneintermediaryis involved.

Intermediary • Who are consideredintermediaries? • Providers of securitiesaccounts. • Brokerage firms, central banks and similar that keep accounts for their clients. • Custodians. • CentralSecurities Depositories. • Only in relationtotheirparticipantswho are clients, notwithissuers. • Issuer and Depositoryare not linked through a securities account for credits and debits.

Prohibition of upper-tierattachment .- Art. 22 • 1. Subject to paragraph 3, no attachment of intermediated securities of an account holder shall be made against, or so as to affect: • a)- a securities account of any person other than that account holder; • b)-the issuer of any securities credited to a securities account of that account holder; or • c)- a person other than the account holder and the relevant dealer. 2. (…) “Attachment of intermediated securities of an account holder” means any judicial, administrative or other act or process to freeze, restrict or impound intermediated securities of that account holder in order to enforce or satisfy a judgment, award or other judicial, arbitral, administrative or other decision or in order to ensure the availability of such intermediated securities to enforce or satisfy any future judgment, award or decision (…)

Securities A deposited in CSD, omnibus fungible account CSD CSD attachmentfreezesallsecuritiesregistrations A of B IntermediaryB Bank Attachmentaccount A in B Bank loan collateralwiththesecuritiesaccount A Holder Y account AwithintermediaryB

ProhibitionFoundation • The encumbrance should not be allowed in circumstances that impair the ability of theintermediaryto perform histheir functions. • The encumbrance in higher level is not compatible with the capacity of a securities account holder of a lower level to trust in histheir position as it appears in the account.

General Rule • Theencumbranceorattachment of securitiesoperates in the precise location of theintermediationchain. • Itbuildsontheassumptionthatthere are threepartsinvolved: • Debtor • Creditor • Recipient of the obligation (intermediary)

Bank B fungible securitiesaccount of allitsclients Bank C Bank C Global Custodian Creditor of X tries toencumbertheaccount of Bank B in C. Bank B Client X withsecuritiesaccountbank B

Othertopicson substantive rules • Protection of aninnocentperson. • Integrity of thesystem. • Protection of theholder of theaccount in case of insolvency of therelevantdealer. • Transmission of securities. Final and irrevocable. • Grantingcollaterals.

Conclusion • The holder of a securities account requiresneeds to trust that histheir holding represented in account is effective against: • The dealer intermediary • Thirdparties • Includesinsolvencyorbankruptcy. • Applicable to any level ofin the chain of intermediatedsecurities.