Download

1 / 9

90 likes | 295 Views

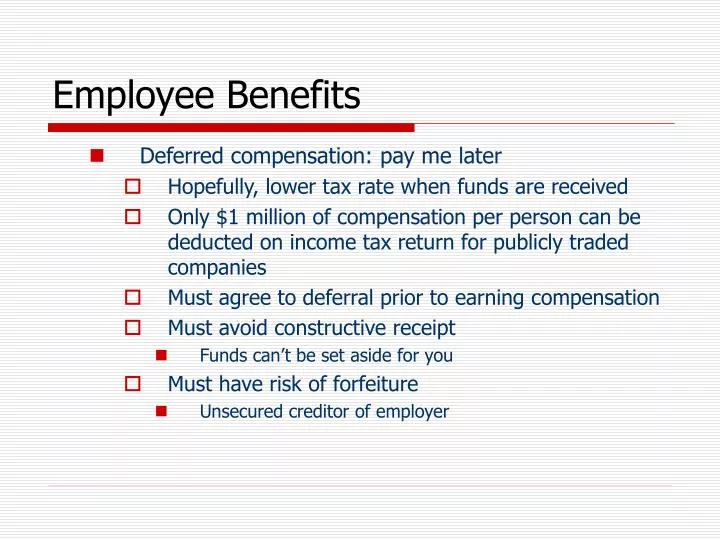

Employee Benefits. Deferred compensation: pay me later Hopefully, lower tax rate when funds are received Only $1 million of compensation per person can be deducted on income tax return for publicly traded companies Must agree to deferral prior to earning compensation

E N D

Employee Benefits • Deferred compensation: pay me later • Hopefully, lower tax rate when funds are received • Only $1 million of compensation per person can be deducted on income tax return for publicly traded companies • Must agree to deferral prior to earning compensation • Must avoid constructive receipt • Funds can’t be set aside for you • Must have risk of forfeiture • Unsecured creditor of employer

Employee Benefits • Deferred compensation: pay me later • Secular trusts: hold funds for paying deferred comp • Not subject to creditors’ claims • Consequently, employees are taxed as soon as funds are transferred to trust • Employer also gets deduction at that time • Rabbi trust • Subject to creditor’s claims • Consequently, not taxed until employee receives funds

Employee Benefits • Phantom stock • Units representing company’s common stock shares • Receive payment in 5, 10, 15 years or at retirement based on increase in stock price • Payment is ordinary income subject to FICA and company gets deduction • Reduces downside risk to executive if stock price falls

Employee Benefits • Nonqualified stock options (NQSOs) • Generally granted with exercise price = stock price at date of grant • Typically can exercise over next 10 years by paying cash or tendering shares owned • If can determine FMV of options at date of grant and no restrictions on options • Ordinary income at date of grant = value of options

Employee Benefits • Nonqualified stock options (NSOs) • Generally restrict transfer of options so no income at time of grant • Then, ordinary income at date of exercise • FMV of stock date of exercise – option price • No AMT preference item

Employee Benefits • Stock Appreciation Rights (SARs) • Receive payment for increase in value of stock • Ordinary income and subject to FICA tax • Company gets deduction for same amount • Don’t actually buy stock • May be paid in cash or stock

Employee Benefits • Restricted Stock • Exec loses stock if doesn’t work for company until a certain date • Shares not vested until that date • Ordinary income when vested • Unless make IRC Sec 83 election to include FMV stock – Purchase price • Then subsequent increase is capital gains • Company gets deduction for that amount

Employee Benefits • Employee Stock Purchase Plans (ESPPs) • Must meet nondiscrimination coverage tests for qualified plans • Gives employees chance to buy stock at a discount (no more than 15%) • Limited to $25,000 stock per year • Similar to ISOs • Long-term capital gains (15% maximum rate) if: • Stock sold more than two years after option was granted and • Stock sold more than one year after option was exercised • Always ordinary income for “discount” amount

Employee Benefits • Junior Stock • Restricted stock exec can convert into common stock if goals are met • Buys junior stock at a discount since value is less doe to risk won’t be able to convert • Capital gains = sales price – purchase price