Download

1 / 29

290 likes | 409 Views

Balanced Scorecard. Financial Performance Measures. Some monetary measurement of income is used by virtually all businesses to assess performance Financial measures do not address issues of competitive reality Typical financial measures: 1) Cash flow 2) Return on Investment

E N D

Financial Performance Measures • Some monetary measurement of income is used by virtually all businesses to assess performance • Financial measures do not address issues of competitive reality • Typical financial measures: • 1) Cash flow • 2) Return on Investment • 3) Residual Income • 4) Economic Value Added

Problems with Financial Measures • 1) Overly aggregate • 2) Not Timely • 3) Backward looking (lagging) • 4) Promote dysfunctional behavior in the short term. • 5) Difficulties in placing a reliable financial link to the value of intangible assets have prevented them from being recognized on a company’s balance sheet • To achieve success in the information era intangible assets are critical for success • Traditional performance measures are insufficient to measure intangibles and future oriented measures

Nonfinancial Performance Measures • Because what gets measured gets improved, non- performance measure are critical for success • Challenged to develop a set of measures that capture critical success factors • A larger scope of nonfinancial performance measures relate to critical success factors. • Non financial performance measures • create shareholder wealth • better predict future cash flows (leading) • are being used increasingly instead of traditional systems

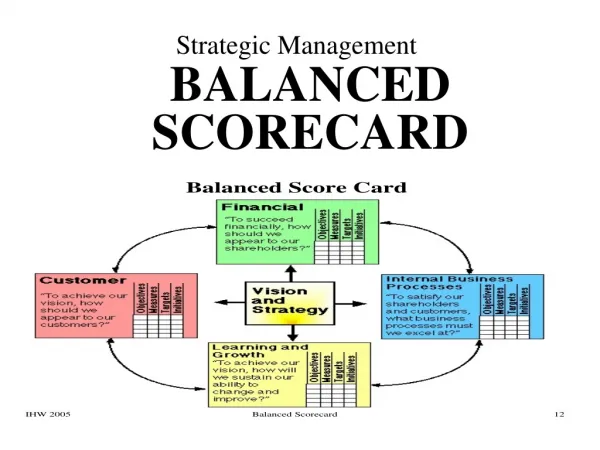

The Balanced Scorecard • The Balanced Scorecard (BSC) provides a system for measuring and managing all aspects of a company’s performance • The scorecard balances traditional financial measures of success, such as profits and return on capital, with non-financial measures of the drivers of future financial performance

The Balanced Scorecard Financial Perspective How do we lookto the firm’s owners? Internal OperationsPerspective In which activities must we excel? Customer Perspective How do our customers see us? Innovation andLearning PerspectiveHow can we continuallyimprove and create value?

1. Financial Perspective • Financial performance measures indicate whether the company's strategy, implementation, and execution are contributing to bottom-line improvement (profitability) • A company’s financial performance can be improved in two ways: • 1. Companies generate revenue growth by: • Selling new products • Selling to new customers • Selling in new markets • 2. Increased productivity occurs by: • Lowering direct and indirect expenses • Utilizing their financial and physical assets more efficiently

Business andproduction processefficiency Customervalue Lead Lead Lead Financial performance1. New interest margin2. Revenue growth3. Customer profitability4. Overall return on assets Financial Perspective Organizationallearning andgrowth

1. Financial Perspective “Empire Company Limited is committed to creating sustainable value through cash flow and income growth, and equity appreciation. “ What are possible financial performance measures for Sobeys?

2. Customer Perspective • Successful organizations satisfy customers’ expectations. • Customer value reflects the degree to which product satisfy customers expectations about price, function and quality. • Customer satisfaction • Customer retention and loyalty • Market share • Customer risk

Customer value 1. Customer satisfaction2. Customer retention and loyalty3. Market share 4. Customer risk Business andproduction processefficiency Lead Lead Lead Financialperformance 2. Customer Perspective Organizationallearning andgrowth

2. Customer Perspective “The management and employees of both our food retailing and real estate divisions are working in collaboration to support Sobeys’ goal of becoming widely recognized as the best food retailer in Canada.“ What are possible customer performance measures for Sobeys?

3. Business and Production Process Perspective • Business and production process perspective focus on internal business and production processes • Operating processes • Customer management processes • Innovation processes • Supplier relations • Employee productivity

Business and production process efficiency 1. New service development2. Employee productivity and error rates3. Service costs 4. Process improvements5. Supplier relations Customervalue Lead Lead Lead Financialperformance 3. Business and Production Process Perspective Organizationallearning andgrowth

3. Business and Process Perspective “Since becoming a public company in 1982, we have done that by focusing on businesses that we know and understand. These businesses – food retailing, real estate and corporate investments – will continue to be our foundation and focus.“ What are possible business and production process performance measures for Sobeys?

4. Learning & Growth Perspective • “Improvements in operating performance result largely form enhancing the capabilities of the organization’s employees and motivating them to use those capabilities so that the organization can learn and improve its processes and products.” • Determine the factors that enable that process to be performed in an outstanding manner so that it can contribute to the success of the company’s strategy: • The employee capabilities: knowledge and skills • The information systems and databases • Employee culture, alignment, and knowledge-sharing

Learning & Growth Perspective Business andproductionprocessefficiency Customervalue Lead Lead Lead Financialperformance Organizationallearning and growth 1. Employee training2. Employee satisfaction3. Employee turnover4. Innovativeness5. Opportunities for improvement

4. Learning & Growth Perspective “With so many job and career options, you are bound to find one that fits your lifestyle and life stage. Here are some of the perks – in case you need more convincing that Sobeys is a great place to work.“ What are possible learning and growth performance measures for Sobeys?

Financial Perspective "To succeed financially, how should we appear to our stakeholders?” Customer Perspective "To achieve our vision, how should we appear to our customers?” Internal Process Perspective "To satisfy customers, and stakeholders, which internal business processes are critical?” People and Knowledge Perspective "To achieve our vision, how will we sustain our ability to change and improve?” Connecting the Four Perspectives Outcomes Drivers

Connecting the Four Perspectives Strategic Theme: Revenue Growth Financial To succeed financially, howshould we appear to ourstakeholders? Improve Returns Broaden Revenue Mix Customer To achieve our vision, howshould we appear to ourcustomers? Increase Customer Confidence in Our Advice Internal Business Process To satisfy our stakeholders and customers in what business processes must we excel? Understand Customer Segments Develop New Products Cross-Sell the Product Line People and Knowledge To achieve our vision, howwill we sustain our abilityto change and improve? Increase Employee Productivity Develop Strategic Skills Access to Strategic Information Align Personal Goals

Implementation: Vision Implementation: Vision • Before determining the objectives and measures, an organization should already have a vision • A concise statement that defines the mid to long-term (3 - 10 year) goals of the organization • The vision should be external and market-oriented and should express, often in colorful or “visionary” terms, how the organization wants to be perceived by the world

Implementation: Mission Statement • A concise, internally-focused statement of how the organization expects to compete and deliver value to customers • It often states the reason for the organization’s existence, the basic purpose towards which its activities are directed, and the values that guide employee’s activities • These statements are far too vague to guide day-to-day actions and resource allocation decisions

Implementation: Objectives • Are concise statements that articulate what the organization hopes to accomplish • Tell the story of the strategy through the cause-and-effect relationships in each of the four balanced scorecard perspectives • The company’s balanced scorecard would typically contain an extensive (3-5 sentence) description of each objective

Implementation: Measures • Measures describe how success in achieving an objective will be determined • Provide specificity and reduce the ambiguity that is inherent in word statements • Specifying exactly how an objective is measured will give employees a clear focus for their improvement efforts

Implementation: Targets • Once the objectives have been translated into measures, managers select targets for each measure • Targets establish the level of performance or rate of improvement required for a measure • Should be set to represent excellent performance • Should, if achieved, place the company as one of the best performers in its industry • Even more important would be to choose targets that create distinctive value for customers and shareholders

Grow Revenue from new products • Annual Revenue Growth • Percent Revenues from New Products +25% 30% • xx • xx Revenue Growth • Satisfy Customer Needs for State-of-Art Capabilities • Customer Retention • Share of Account 80% 40% • Relationship Management Program • Gain Sharing Program Innovative Products • Accelerate New Product Development • Product Functionality • Time to Market #1 in indy. 9 mos. • University Liaison/ Technology Transfer • Development Cycle Time Reengineering World Class Internal Product Development • Acquire, Develop and Retain Strategic Skills • Specialized Competency Availability • Key Staff Retention 100% 95% • Competency Model • New Hiring Program • Supervisory Training • Benefits Program Stable High-Talent Workforce Balanced Scorecard Illustrative Strategy Map Objective Measure Target Initiative Strategic Theme: Internal Product Development Financial Customer Internal People & Knowledge

BSC: Benefits • Expresses an organization's mission and strategy • Captures both leading and lagging measures • Communicate strategy to employees • Impact at individual level • Motivate and evaluate performance

BSC: Pitfalls • As with any new technology or management tool, not all BSC implementations have been successful • Several design factors can lead to problems and disappointment when applying the BSC • Too few measures in the scorecard • Too many measures • Attention is diffused, and insufficient attention is given to those few measures that make the greatest impact • The drivers in the Internal and Learning & Growth perspectives don't link to the desired outcomes in the Financial and Customer perspective

BSC: Pitfalls (cont’d) • Senior management is not committed, and the BSC project is delegated to middle management • One senior manager builds the scorecard alone • Senior executives feel that only they need to know and understand the strategy, and BSC responsibilities don't filter down • The BSC is treated as a one-time event that requires the perfect scorecard for implementation • The BSC is treated as a systems project rather than as a management project