Download

1 / 20

200 likes | 341 Views

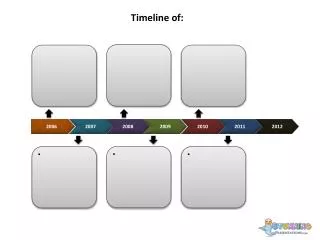

Fiscal Institutions in New Zealand: The question of spending caps and spending reviews John Janssen February 2011. A timeline of budget management. From 2011: Fiscal Management Approach +. From 1989: Fixed Nominal Baselines. From 1997: Fiscal Provisions. From 2002: Fiscal

E N D

Fiscal Institutions in New Zealand: The question of spending caps and spending reviewsJohn JanssenFebruary 2011

A timeline of budget management From 2011: Fiscal Management Approach+ From 1989: Fixed Nominal Baselines From 1997: Fiscal Provisions From 2002: Fiscal Management Approach For details and fit with overall fiscal legislation refer: Fiscal Institutions in New Zealand and the Question of a Spending Cap http://www.treasury.govt.nz/publications/research-policy/wp/2010/10-07

Fixed Nominal Baselines • Prior to 1989 the budget process involved regular adjustments to personnel costs • Operating and capital adjusted annually with 1-year ahead forecasts only • Early 1990s – fixed nominal baseline over a 3-year forecast period that changed only with specific policy decisions • Formula-driven indexation to non-departmental spending (eg, inflation indexation of transfers; volume changes)

Fiscal Provisions • 1997 Budget introduced a $5 billion (cumulative) spending cap on new initiatives over fiscal years 1998 – 2000 • Spending cap sat on top of fixed nominal baselines and formula-driven indexed items • Rules established to determine what counted against the spending cap • Spending cap re-labeled as fiscal provisions – for both operating and capital • Included as line items in fiscal forecasts (3 years ahead)

Fiscal Management Approach • 2002 Budget re-labeled the fiscal provisions as operating allowances and capital allowances • Shifted the focus to the paths of operating balance and debt rather than just the nominal allowance • Fiscal allowances reviewed twice a year with reference to updated forecasts and progress against fiscal objectives (especially debt-to-GDP)

Sources of spending change • Anticipated price and volume effects for formula driven items built into forecasts (eg, rising cost of pensions from population ageing) • Discretionary initiatives as part of the fiscal allowance. Expectation that allowances adjusted only in response to structural changes in the fiscal outlook • Changes in forecast costs due to revisions of initial forecast (eg, higher than anticipated take-up)

Aims of proposed spending cap • Increase transparency around the total level of spending with more focus on baselines, relative to discretionary allowances • Provide some inertia in response to revenue surprises • Looked at experiences of Sweden, Netherlands and Finland

Key features of proposed cap • Absolute dollar figure for operating expenses • Exclude unemployment expenses and finance costs • Set for three years with the third year set on a rolling basis • Margin of 1% to act as a buffer for unforeseen events • Cap set by current administration rather than prescribed in legislation • Transparency around potential breaches and policy reaction

Selected approach – FMA+ • Risks around spending cap: complexity; flexibility; target rather than upper limit; still cycle versus trend identification challenge (especially in rolling third year) • Current system places a cap on discretionary spending via the operating and capital allowances – which have been set at much lower levels than mid-2000s • Increase the range of expenses subject to scrutiny – to improve control over higher-than-expected increases in expenses • Set aside a portion of the existing allowance to deal with these

Other changes • Shift resources to frontline services (headcount cap for core government administration) • Improve balance sheet management (publication of detailed investment statement) • Investigate mixed ownership model for some commercial assets • Alternatives to public provision (eg, PPPs) • Better administrative and support services • Drawing on skills beyond the core public services (eg, Defence Review; Review of Expenditure on Policy Advice)

Future developments? • Recent Taskforce suggestion that Public Finance Act be amended to require the Minister of Finance to specify a five-to-ten year target for future operating expenses (capacity exits in Act but not typically used) • Independent Fiscal Council • Taxpayer Bill of Rights – limit spending growth to inflation rate and population growth, with any higher spending subject to a referendum

A timeline of budget management From 1989: Fixed Nominal Baselines From 1997: Fiscal Provisions From 2002: Fiscal Management Approach From 2011: Fiscal Management Approach+

Main lessons • Classification – discretionary/other; cycle/trend • Context – surplus environment (pressure to revise a cap upwards); deficit environment (shift to other tools such as reviews) • Change – some change is inevitable as people learn the rules • Continuity – credibility and understanding of broad approach – with adjustments at the margin

Changes in Core Crown operating expenses relative to 2009/10 year