Download

1 / 33

• 330 likes • 443 Views

BPA Debt Optimization Presentation to the Energy Northwest Board Audit, Legal, and Finance Committee June 21, 2000. Objectives Background Program Proposal Maintenance of Capital Programs Summary Next Steps. Objectives. Program Objectives.

E N D

BPA Debt Optimization Presentationto theEnergy Northwest BoardAudit, Legal, and Finance CommitteeJune 21, 2000

Objectives Background Program Proposal Maintenance of Capital Programs Summary Next Steps ENW6_15_00IF ppt

Objectives ENW6_15_00IF ppt

Program Objectives BPA is proposing to undertake a program of prudent debt management that: 1) reduces total debt service costs of BPA and lowers rates to ratepayers, 2) sustains delivery capability of capital programs, and 3) allows more variable rate debt as recommended by Energy Northwest ENW6_15_00IF ppt

Today’s Objectives To provide information supporting your fiduciary responsibility to conduct due diligence of refinancing proposals To provide the information you requested about BPA’s debt optimization strategy To respond to your further questions and concerns ENW6_15_00IF ppt

Background ENW6_15_00IF ppt

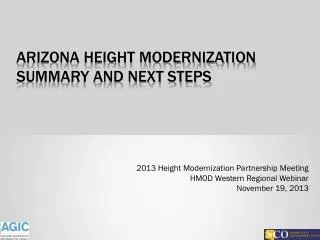

BPA Faces an Enormous Amount of Uncertainty:Planned Net Revenues for Risk are Designed to Address that Uncertainty 1997-2001 Rates Maximum value 2002-2006 Rate Case anticipates market prices that average $34 / MWh flat undelivered (maximum $126 / MWh and minimum $6 / MWh) $500 $400 $300 $200 $12.2 Million $100 (Mean) $Millions $0 ($100) - $26.5 Million - $1.5 Million - $10.1 Million (Mean) - $4.9 Million - $0.2 Million -$22.8 Million ($200) (Mean) (Mean) (Mean) (Mean) (Mean) ($300) ($400) 90% Confidence Interval ($500) ($600) Minimum value Total Hydro DSI Economy SW Market Weather Nuclear ENW6_15_00IF ppt

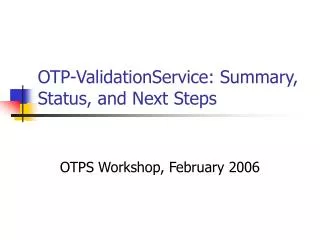

Rate Case Planned Net Revenues Actual Net Revenue Relative to Rate Case Expectations, Net Revenues Were Significantly Higher in FY’s 90 & 91, and Lower in FY’s 92 & 93 500 400 300 200 100 $ millions 0 1994 1998 1989 1990 1991 1992 1993 1995 1996 1997 1999 (100) BPA sets rates to recover costs. Rates are designed around the revenue requirement which is the best cost forecast at the time. Sometimes either the cost or revenue forecast, or both, significantly deviate from plans. The results of the early 90’s are extreme examples of the magnitude of possible deviations. (200) (300) (400) ENW6_15_00IF ppt

Historical Perspective on Risk and Reserves Between 1975 and 1983, BPA often failed to pay Treasury all it owed in a timely manner. In the late 1980’s, with rising rates and increasing costs, BPA realized that it needed additional financial flexibility in order to ensure that Treasury payments were made, thus the Accelerated Front End Savings (AFES) was established as part of the refinancing program. In the early 1990’s, through the 10-year financial plan, the focus shifted to the ongoing need to covering risks and ensure a high probability of Treasury payments (TPP). ENW6_15_00IF ppt

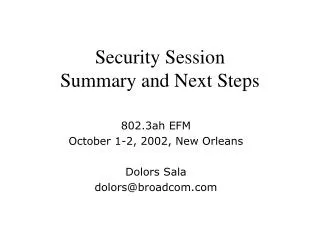

Rates Adjusted FY’s 90 & 91: Net Revenue Increases Were Primarily Due to AFES; FY’s 92 & 93: Net Revenue Shortfalls Were Primarily Due to Low Aluminum Prices and Low Streamflows 400 300 200 100 0 $ millions (100) (200) (300) (400) (500) 1990 1991 1992 1993 Net Revenue Difference ENW DS Savings Aluminum Revenues (600) Streamflow Impacts Other Impacts ENW6_15_00IF ppt

Additional Federal Amortization $300M Extraordinary Columbia Capital Improvements $150M Rate Relief $1,150M Benefits of Previous Energy Northwest Refinancings Maintain low power rates Facilitate BPA’s positioning in the emerging deregulated wholesale power market The early Energy Northwest refinancings enabled BPA to make Treasury payments as planned through times of considerable hardship. Had refinancings not occurred BPA would have had three options: 1) raise rates, 2) miss Treasury payments, and/or 3) reduce costs. If BPA had missed Treasury payments, Northwest cost-based rates would have been seriously threatened. ENW6_15_00IF ppt

Historical Perspective on Risk and Reserves Between 1975 and 1983, BPA often failed to pay Treasury all it owed in a timely manner. In the late 1980’s, with rising rates and increasing costs, BPA realized that it needed additional financial flexibility in order to ensure that Treasury payments were made, thus the Accelerated Front End Savings (AFES) was established as part of the refinancing program. In the early 1990’s, through the 10-year financial plan, the focus shifted to the ongoing need to covering risks and ensure a high probability of Treasury payments (TPP). ENW6_15_00IF ppt

Current Perspective on Risks and Reserves The 2002 Rate Filing includes the ability to achieve the full 88% TPP for the first time. • $800M SOY cash reserves. • Currently proposed 2002-2006 $100M per year planned net revenues for risk (PNRR). Compared to 1991-1992, BPA is addressing most risk before the fact through rates rather than after the fact by depleting reserves or failing to pay Treasury. Now BPA can focus on creating additional stability by • Lowering the fundamental cost structure, • Ensuring adequate capital financing, and • Adding more flexible features to Energy Northwest debt (variable rate debt, etc) ENW6_15_00IF ppt

Program Proposal ENW6_15_00IF ppt

Background on Capital Plan BPA reduced Capital Program levels and accepted targets in the Cost Review for refinancing savings (achieved) A Capital Strategy was developed that had two major elements a) development and implementation of Capital Budgeting Process, and b) managing access to capital Capital Plan focused on managing access to capital As part of Capital Plan process, numerous alternatives were looked at and Capital Plan focused on those tools which reduced overall debt service costs Capital Plan meets two key criteria: reduction in overall debt service and continuing availability of BPA’s Treasury borrowing authority ENW6_15_00IF ppt

Major Recommendations Included in the Capital Plan Extend the final maturities on Columbia debt to 2013-18 Substitution of Surety Bonds for some debt service reserve amounts - already accomplished for $38 million in May 2000 Selective Redemption of ENW debt - an ongoing program designed to maximize cashflow savings Managing Federal Amortization - manages the terms and amortization of federal Treasury bonds to extend availability of borrowing authority ENW6_15_00IF ppt

Program Proposal Extend final maturities of Columbia debt to 2013-2018, creating a better asset/liability match Complete an initial advance refunding sometime between November 2000 and April 2001 (approximately $600M) Include a significant increase of variable rate debt As cash flows into the Bonneville fund from lower ENW debt service, utilize it to retire higher interest Federal debt. Expect the advance refunding proposal to be fine-tuned and improved as ENW’s financial advisor becomes increasingly engaged and an underwriter is selected Complete additional refundings (up to an additional approximate $400-700M) as bonds become currently callable (assumed refinancing dates of 2004 and 2008 for analysis purposes only) ENW6_15_00IF ppt

Proposed refinancings: Are evaluated in the context of BPA’s total debt portfolio Emphasize prudent debt management by minimizing overall debt service expense Reinforce asset/liability matching by extending Columbia debt Have a specific plan for prudent use of cash flows In addition to minimizing total debt service, supports other ENW/BPA desires to: a) Increase variable rate debt, and b) Assure continued availability of BPA borrowing capacity with Treasury Proposed Debt Optimization Advantages ENW6_15_00IF ppt

1.2 1.0 0.8 0.6 0.4 0.2 0.0 2000 2001 2002 2003 2004 2005 2006 2007 2008 Refinancing Columbia Debt Lowers Power’s Annual Debt Service (Reflects Advance Refunding Only) Before Refinancing After Refinancing Power Debt Service After Refinancing $ in billions Non-Federal Debt Service Before Refinancing 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 ENW6_15_00IF ppt

Additional Discussion Concerning Debt Optimization The present value (discount rate of 9%) of combined federal and non federal debt service savings from the advance refunding alone ranges from $90M to $150M, depending on interest rates at the time of refinancing and other factors. Average annual savings to preference ratepayers of at least $10-15M per year (2001-2018) Other ideas which could increase the present value savings • Extending existing $120M variable rate debt (issued 3/98) to 2018 • Using alternative debt structure for new bonds • Completing additional refundings after FY 2001 • Engaging the expertise of ENW’s financial advisor and the underwriter (to be selected) once it is decided to move forward ENW6_15_00IF ppt

Communications Strategy BPA views debt optimization as a normal and prudent course of business No elaborate public process is planned or expected Account Executives and others will be thoroughly briefed in order to respond to customers’ and constituents’ questions ENW6_15_00IF ppt

Questions/Answers Relating to the Future What happens with net-billing and the power generated by Columbia when the debt is fully paid? The relationship between Bonneville and Energy Northwest stays the same. That is, net-billing continues to exist, and all the power generated is still marketed by BPA. BPA would still be financially responsible for all Columbia costs, including capital additions/replacements and funding future decommissioning. What happens if BPA and/or ENW wants to sell Columbia? As a condition to sale or other transfer of the project (unless the project has been terminated), all of the bonds then outstanding would have to be defeased. In addition, all of the net-billing participants in the project would have to consent to the sale. What would happen if BPA were sold? As a practical matter, all of the bonds for all three projects would have to be defeased prior to a sale of BPA or bondholder security otherwise assured. ENW6_15_00IF ppt

Maintenance of Capital Programs ENW6_15_00IF ppt

Capital Funding Review Process Bonneville’s capital requirements go through many critical reviews before expenditures proceed. 1. Pre Rate Case: Public review and input process involves customers and constituents prior to rate case 2. Internal BPA Capital Budgeting: Requires use of risk weighted rates of return and critical choices among alternative proposals 3. Administrative: Proposed capital spending levels reviewed by BPA management 4. BPA’s Budget: Review and approval or disapproval by OMB and other Executive Agencies 5. Appropriations Committees: Review by both House & Senate Committees 6. Northwest Power Planning Council Review: Regional F&W and power program reviewed ENW6_15_00IF ppt

Expected Average Annual Capital ExpendituresFY2000 to 2011 Corporate $11M Power $ 95M Transmission $195M ENW6_15_00IF ppt

Assurance that BPA Management Will Stay Committed to the Capital Plan With ENW approval, it would take deliberate and conscious action to NOT follow the Capital Plan. The current high level of reserves and risk mitigation already built into rates minimizes risk that the cashflow savings will need to be diverted for other uses, and reserves also provide cashflow flexibility for implementation of the plan. BPA management has thoroughly reviewed the Capital Plan and is committed to its implementation in the best long-term interests of the Region’s ratepayers. Debt optimization, including extension of Columbia debt, is consistent with prudent debt management and overall sound business principles. It would be imprudent not to seek to optimize. Our intention is to include this program in our budget submission. The positive impact on borrowing authority provides additional incentive for following through on debt optimization. ENW6_15_00IF ppt

Summary ENW6_15_00IF ppt

Summary With Energy Northwest approval, Bonneville executive management is committed to carry out Debt Optimization. Debt Optimization is in the economic best interests of the Region’s ratepayers over the long term as it lowers BPA’s overall costs and contributes to sustained long term access to low cost capital. Debt Optimization is a carefully tailored strategy which greatly differentiates it from the previous Accelerated Front-End Savings (AFES) Program, in that proposed refinancings: 1) Have an immediate, committed use for the cashflow savings 2) Reinforce asset/liability matching by extending Columbia debt 3) Exemplify an industry best practice of comprehensive debt portfolio management Debt Optimization is a phased-in program that ENW will be able to review over time. ENW6_15_00IF ppt

Next Steps ENW6_15_00IF ppt

Next Steps Continue work between BPA and ENW staffs as well as ENW financial advisor Present more detailed information to AL&F Committee at July Meeting Select underwriter by early August Obtain AL&F Committee decision to move forward at August Meeting By the end of August notify the Participant Review Board of refinancing plans Perform necessary analysis and Official Statement work between September and November to be in a position to go to market between November 2000 and April 2001 ENW6_15_00IF ppt

BPA Year End Financial Reserves • Financial reserves comprise cash in BPA Fund and cash equivalents in form of a deferred borrowing balance • Reserves are BPA’s principal means of mitigating risk ENW6_15_00IF ppt

4000 3500 3000 2500 2000 1500 1000 500 0 1994 1994 1995 1996 1997 1998 1999 2000 BPA and Energy Northwest Have Significantly Reduced Staffing BPA FTE EN ENW6_15_00IF ppt