Download

1 / 26

260 likes | 415 Views

Review Chapter 13 and Chapter 14. Chapter 13 Outline. Expected Returns and Variances of a portfolio Announcements, Surprises, and Expected Returns Risk: Systematic and Unsystematic Diversification and Portfolio Risk Systematic Risk and Beta The Security Market Line (SML). Portfolios.

E N D

Chapter 13 Outline • Expected Returns and Variances of a portfolio • Announcements, Surprises, and Expected Returns • Risk: Systematic and Unsystematic • Diversification and Portfolio Risk • Systematic Risk and Beta • The Security Market Line (SML)

Portfolios • The risk-return trade-off for a portfolio is measured by the portfolio expected return and standard deviation, just as with individual assets Portfolio = a group of assets held by an investor Portfolio weights = Percentage of a portfolio’s total value in a particular asset

Portfolio Expected Returns (1) • The expected return of a portfolio is the weighted average of the expected returns for each asset in the portfolio • You can also find the expected return by finding the portfolio return in each possible state and computing the expected value

Calculate Portfolio Variance • Portfolio variance can be calculated using the following formula: • Correlation is a statistical measure of how 2 assets move in relation to each other • If the correlation between stocks A and B = -1, what is the standard deviation of the portfolio?

Measuring Systematic Risk • Beta (β) is a measure of systematic risk • Interpreting beta: • β = 1 implies the asset has the same systematic risk as the overall market • β < 1 implies the asset has less systematic risk than the overall market • β > 1 implies the asset has more systematic risk than the overall market

Reward-to-Risk Ratio: • The reward-to-risk ratio is the slope of the line illustrated in the previous slide • Slope = (E(RA) – Rf) / A • Reward-to-risk ratio = • If an asset has a reward-to-risk ratio = 8? • If an asset has a reward-to-risk ratio = 7?

The Fundamental Result • The reward-to-risk ratio must be the same for all assets in the market • If one asset has twice as much systematic risk as another asset, its risk premium is twice as large

Chapter 14 Cost of capital and long-term financial policy

The Dividend Growth Model Approach • Can be rearranged to solve for RE

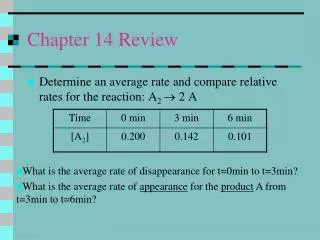

Example: Estimating the Dividend Growth Rate • One method for estimating the growth rate is to use the historical average • Year Dividend Percent Change • 20051.03 • 20061.139.7% Geom. Av = 7.97% • 20071.2611.5% • 20081.335.55% • 20091.40 5.26% arithmetic av.=8% • Analysts’ forecast can be used

Alternative Approach to Estimating Growth • If the company has a stable ROE, a stable dividend policy and is not planning on raising new external capital, then the following relationship can be used: • A company has a ROE of 17% and payout ratio is 15%. If management is not planning on raising additional external capital, what is its growth rate? Solution: g=17*(1-.15)=14.45% • g = Retention ratio x ROE

The SML Approach (CAPM) • Use the following information to compute our cost of equity • Risk-free rate, Rf • Market risk premium, E(RM) – Rf • Systematic risk of asset, E(RA) = Rf + A(E(RM) – Rf)

SML example • Suppose the company has an equity beta of 1.28 and the current risk-free rate is 3.2%. If the expected market risk premium is 9.8%, what is the cost of equity capital? Solution: 15.744%

Cost of Equity • Suppose the company has a beta of 1.45. The market return is expected to be 15.2% and the current risk-free rate is 4%. Dividends will grow at 5% per year and last dividend was $1.2. The stock is currently selling for $7.35. What is our cost of equity? • Using SML: 20.24% • Using DGM: 22.14%

Cost of Debt example • Suppose you have a bond issue currently outstanding that has 17 years left to maturity. The coupon rate is 8% and coupons are paid annually. The bond is currently selling for $955.874 per $1000 bond. What is the cost of debt? Solution: 8.5%

Cost of Preferred Stock • Preferred stock generally pays a constant dividend every period • Dividends are expected to be paid every period forever • Preferred stock is perpetuity • RP = D / P0

Cost of Preferred Stock example • A company has preferred stock that has an annual dividend of $2. If the current price is $15, what is the cost of preferred stock? Solution: 13.33%

Flotation Costs • The required return depends on the risk, not how the money is raised • However, the cost of issuing new securities should not just be ignored either • Basic Approach • Compute the weighted average flotation cost

NPV and Flotation Costs example • A company is considering a project that will cost $1.2 million. The project will generate after-tax cash flows of $250,000 per year for 9 years. The WACC is 12% and the firm’s target D/E ratio is .5 (1/2). The flotation cost for equity is 4% and the flotation cost for debt is 2%. What is the average flotation cost? What is the NPV for the project after adjusting for flotation costs?

Solution • D=400,000 fd = 400,000*.02 = 8,000 • E=800,000 fE = 800,000*.04 = 32,000 • Fac = .0267 + .0067 =.0334=3.34% • PV=(1,240,000) • PVFCF= 1,332,062.448 • NPV = 92,062.448 positive