Download

1 / 1

10 likes | 84 Views

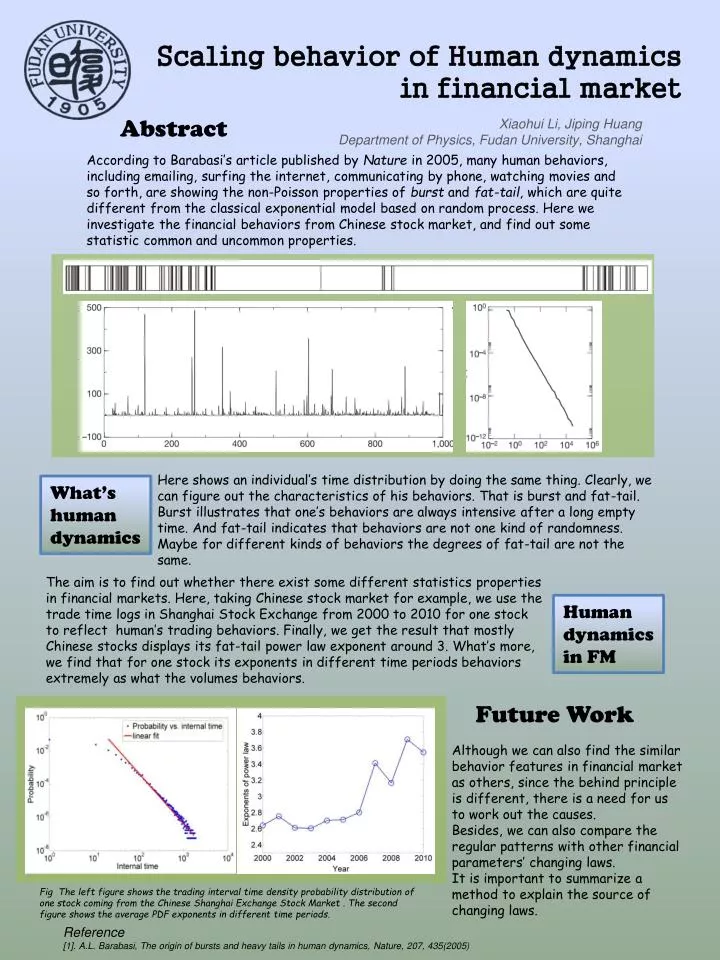

Scaling behavior of Human dynamics in financial market. Abstract. Xiaohui Li, Jiping Huang Department of Physics, Fudan University, Shanghai.

E N D

Scaling behavior of Human dynamics in financial market Abstract Xiaohui Li, Jiping Huang Department of Physics, Fudan University, Shanghai According to Barabasi’s article published by Nature in 2005, many human behaviors, including emailing, surfing the internet, communicating by phone, watching movies and so forth, are showing the non-Poisson properties of burst and fat-tail, which are quite different from the classical exponential model based on random process. Here we investigate the financial behaviors from Chinese stock market, and find out some statistic common and uncommon properties. Here shows an individual’s time distribution by doing the same thing. Clearly, we can figure out the characteristics of his behaviors. That is burst and fat-tail. Burst illustrates that one’s behaviors are always intensive after a long empty time. And fat-tail indicates that behaviors are not one kind of randomness. Maybe for different kinds of behaviors the degrees of fat-tail are not the same. What’s human dynamics The aim is to find out whether there exist some different statistics properties in financial markets. Here, taking Chinese stock market for example, we use the trade time logs in Shanghai Stock Exchange from 2000 to 2010 for one stock to reflect human’s trading behaviors. Finally, we get the result that mostly Chinese stocks displays its fat-tail power law exponent around 3. What’s more, we find that for one stock its exponents in different time periods behaviors extremely as what the volumes behaviors. Human dynamics in FM Future Work Although we can also find the similar behavior features in financial market as others, since the behind principle is different, there is a need for us to work out the causes. Besides, we can also compare the regular patterns with other financial parameters’ changing laws. It is important to summarize a method to explain the source of changing laws. Fig The left figure shows the trading interval time density probability distribution of one stock coming from the Chinese Shanghai Exchange Stock Market . The second figure shows the average PDF exponents in different time periods. Reference [1]. A.L. Barabasi, The origin of bursts and heavy tails in human dynamics, Nature, 207, 435(2005)