Download

1 / 56

560 likes | 726 Views

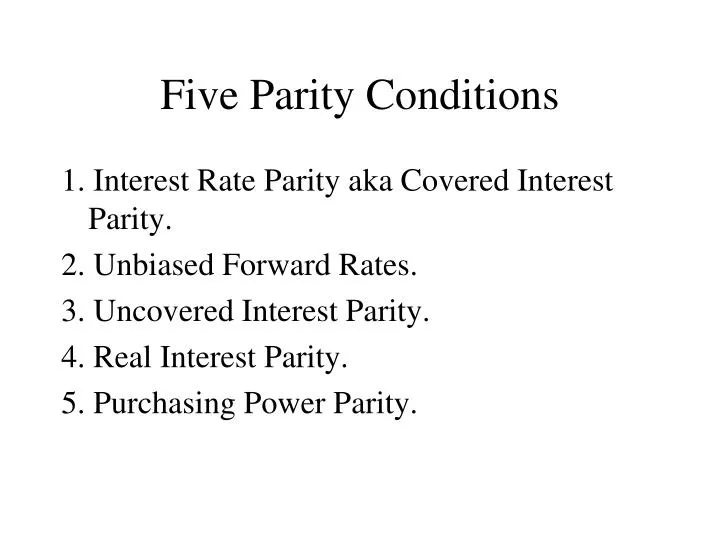

Five Parity Conditions. 1. Interest Rate Parity aka Covered Interest Parity. 2. Unbiased Forward Rates. 3. Uncovered Interest Parity. 4. Real Interest Parity. 5. Purchasing Power Parity. Unbiased Forward Rates. On the average , forward rate = spot rate that will prevail at maturity.

E N D

Five Parity Conditions 1. Interest Rate Parity aka Covered Interest Parity. 2. Unbiased Forward Rates. 3. Uncovered Interest Parity. 4. Real Interest Parity. 5. Purchasing Power Parity.

Unbiased Forward Rates • On the average, forward rate = spot rate that will prevail at maturity. • If = does not hold, the prospect of profits exists. Arbitrage? Not! • Make money with no investment but with risk: Buy low, sell high! • FX that exhibits a forward premium (discount) will appreciate (depreciate).

Uncovered Interest Parity • Combine interest rate parity with unbiased forward rates. • Transactions are identical to those of interest rate parity but with no forward hedging. There is FX risk. • Seek profit by borrowing low and investing high but this is not arbitrage.

UIP: Intuition • RF>RD implies S1<S0. A high interest rate currency will depreciate (IRP: exhibit forward discount). • Similarly, a low interest rate currency will appreciate (IRP: exhibit a forward premium).

Ex-post application of uncovered interest parity. • True ex-post by definition. • Split up domestic currency rate of return on a foreign security into two components: rate of return of the foreign security and the appreciation of the foreign currency. • Investment in a foreign security means investment in two different factors.

Application of ex-post uncovered interest parity • CAC 40 rose by 53.64 %, euro depreciated by 14.94% (vis-à-vis C$)during a certain year. • What rate of return did Canadian investor achieve? • 30.69% = (1+53.64%)x(1- 14.94%) –1 • 30.69% measured in C$’s, 53.64% measured in euros.

Who ripped off Charlie Canuck? • Focus: S&P500 for 2003. • RU$, rate of return in U$’s, = 19%. • RC$, rate of return in C$’s, = 1.7%. • Jan’03:U$0.63/C$ vs. Dec’03:U$0.737/C$. • Appreciation of C$: (.737/.63)-1=17%. • (1+19%)=(1+1.7%)(1+17%)

Charlie Canuck continued • What’s depreciation of U$? 17%? Not!! • Jan’03:C$1.587 vs. Dec’03:C$1.357. • U$appreciation=(1.357/1.587)-1= -14.5% • Exact Relation: (1+17%) = (1-14.5%)^-1; (1+C$appreciation)=(1+U$appreciation)^-1 • One plus appreciation of one currency equals the reciprocal of one plus appreciation of the other currency.

Two Useful Transformations • Appreciation in one currency vs. appreciation in the other currency. • Rate of return on a security measured in one currency vs. rate of return on the same security measured in another currency. • Must know how to transform data provided! • The data are provided in the form of percentages. • Data must be converted into decimal format before the transformations can be applied.

Real Interest Parity • Real interest rates tend to be equalized across currencies. • High inflation currency exhibits high interest rates. • (1+foreign interest rate) / (1+foreign inflation rate)=(1+domestic interest rate) / (1+domestic inflation rate).

Purchasing Power Parity • Law of one price: a commodity must trade at same exchange rate adjusted price. • Domestic price = S x Foreign price. • If > holds: buy foreign, sell domestic. • If < holds: buy domestic, sell foreign. • Commodity arbitrage tends to make inequality disappear.

Big MacCurrencies Down Unda • BM price in U.S. = U$2.32 • BM price in Aus. = A$2.45 • PPP implies: S(A$/U$) = A$2.45/U$2.32 = A$1.06/U$. • Compare to actual S = A$1.35/U$. • U$ overvalued, A$ undervalued. • Overvaluation of U$ = 27.36% implies undervaluation of A$ = 22%.

More on Aussie Big Macs • Price of BM in Aus. In U$=A$2.45/A$1.35 = U$1.82. • Compare with US price = U$2.32. • Overvaluation of BM in Aus. = -22%. • The overvaluation of a commodity in a country reflects the overvaluation of that country’s currency.

PPP across time • PPP holds at start of year • PPP holds at end of year • (Send/Sstart)= (1+Id)/(1+If) • (1+af) = (1+Id)/(1+If) • Intuition: A high inflation currency will depreciate.

Canadian Exporter • Transactions Exposure - FX cash flows it will receive over the next 6 months are contractually set. • Operating Exposure – FX cash flows it may receive beyond the 6-month time horizon from contracts as yet unsigned. • More subtle forms of operating exposure in vignettes.

Four operating exposure vignettes • 1. Aspen Skiing: Revenues exhibited positive operating exposure. • 2. Laker Airways: Ditto, but negative operating exposure. • 3. Petróleos Mexicanos: Revenues denominated/determined by U$. • 4. YCF: Revenues denominated in APeso but determined by U$.

Aspen Skiing • Colorado resort: all balance sheet items and cash flows in greenbacks. • Yet exposed to C$, FFr, etc. • In 1983, U$ appreciated, I.e. C$, FFr depreciated. • Domestic and foreign clientele shifted holidays to Banff, Chamonix, Chicopee.

Aspen Skiing Y-axis: Cash flows in U$; X-axis: S(U$/C$)

Aspen Skiing: Lesson Gleaned Although you operate exclusively domestically, if your clientele has the option of purchasing in a foreign market, you exhibit positive exposure to that foreign market’s currency. A U.S. firm with Aspen Skiing as client likewise possesses the same type of exposure.

Aspen Skiing: Two Hedges • Hedge positive operating exposure of cash flows to C$, FFr, etc. • Denominate some debt in C$, FFr, etc.Result: negative transactions exposure of debt offsets positive operating exposure of revenues. • Buy resorts in Canada, France, etc. Result: some revenue streams rise, other fall with rise in C$, FFr, etc.

Laker Airways • Early exploiter of air transport deregulation in late 70’s. Target market: Price conscious Brit tourists vacationing in Florida. • Cost structure: jet fuel U$-denominated. • Financed jets with cheap U$-debt provided by US Ex-Im Bank. • Steep U$ appreciated in early 80’s spelled doom for Laker Airways.

Laker Airways’ Exposures • Jet fuel: both transactions and operating exposure to U$. • Debt: transactions exposure to U$. • Revenues: negative operating exposure to U$. When U$ appreciated target clientele shifted holidays from Florida to Palma de Mallorca, Islas Canarias, Marbella, etc.

Laker Airways: Lessons Gleaned • If your business involves assisting a domestic clientele purchase goods/services in a foreign country, you have negative operating exposure to that foreign country’s currency. • Dollar denomination of debt aggravated the firm’s negative exposure to the greenback.

Sir Freddie’s Egregious Error • Error: Denominated debt in U$’s. • Appreciation of U$ resulted in: Sterling value of costs and debt service increasing; Sterling value of revenues decreasing. • Sir Freddie got squeezed! • Hedges: debt denominated in Sterling; cater to Yank clientele vacationing in UK.

Petróleos Mexicanos • Most of output sold in world oil markets, ergo U$-denominated. • Revenues exhibit both transactions and operating exposure to U$. • Hedge: debt denominated in U$’s. • Negative transactions exposure of debt service offsets positive exposure of revenues.

Yacimientos Pertrolíferos Fiscales (YPF) • Most of output sold domestically, i.e., Argentine peso denominated. • Debt denomination in U$´s also makes sense! Huh?? • No price controls on domestic oil. • PPP applies to oil. If U$ rises, peso price of oil rises.

YPF • Revenues: currency of denomination is peso but currency of determination is U$. • PPP: Ppeso = Pworld(U$) X S(AP/U$). • For PPP to hold, Ppeso must rise if S rises. • Hedge: debt denominated in U$’s. • Transactions exposure of debt offsets operating exposure of revenues.

Pemex & YPF: Lessons Gleaned • Pemex: Transaction exposure of debt service (denomination of debt in a foreign currency) can offset the positive transactions/operating exposure of a revenue stream. • YPF: As in Pemex, but revenue stream possess only positive operating (no transactions) exposure to a foreign currency.

Yankee Inc.’s Exposures • US firm exports to UK; major competitor in UK is importer from France • Export contracts denominated in sterling • Yankee faces positive transactions exposure to sterling; X variable is S(USD/BPS) • Yankee faces positive operating exposure to the euro; X variable is S(USD/EUR)

Canuck Ltd. • Canadian firm operating exclusively in Canada. • Competitor in Canada sources product in the UK. • Canuck Ltd. has positive exposure to the Pound Sterling, PS.

Canuck Ltd.’s Operating Exposure • Measured as slope of Canuck’s risk profile. • Vertical axis = cash flow measured in reference currency (C$). • Horizontal axis = FX rate measured in direct quotation (C$/PS). • Somehow calculate slope = PS1.923M, say. Interpret: As if receiving PS1.923M per period • Regression model improves this approach: slope calculation and statistical test.

Hedging operating exposure • Use denomination of long-term debt. • How to determine extent of exposure? Simple regression (use direct quotation). • Regress domestic currency CF on FX exchange rate. • Or regress domestic currency rate-of-return on %-age appreciation of FX.

Measuring Operating Exposure • Slope term of simple regression. • X-variable: S in direct quotation; also appreciation in S. • Y-variable: cash flow in reference currency; also growth rate in cash flow. • Critical statistics: slope term, t-statistic for slope term.

3 possible regression specifications: • Y = CF in reference currency and X = S (direct quotation) e.g. Tin Man. • Y = rate of return on stock measured in reference currency and X = % appreciation of S (direct quotation) e.g. Selamat Malam. • Y = growth rate in CF measured in reference currency and X = % appreciation of S (direct quotation) e.g. Marubeni-Iida.

Simple Regression Slope • Denominated in units of foreign currency. • As if that amount of FX received per period. • Null hypothesis: slope = 0, I.e., no operating exposure. • Alternative hypothesis: slope not = 0, I.e., operating exposure exists. • Reject null: absolute value of t statistic > 2.

Ballad of the Tin Man • Application of regression approach. • Simple regression slope coefficient is not significant. Ergo, no operating exposure to PS, PS denominated debt not appropriate. • Although the acquired company generates PS CF’s, debt employed in acquisition should be U$ denominated. • Ballad’s: currency of denomination is PS, currency of determination is U$.

Tin Man: effects of different debt denominations • Message of regression: CF(gross of debt service) in U$’s not affected by FX rate. • With PS debt: Rise in PS causes a reduction in U$ net of debt service CF. • With U$ debt: Rise in PS causes no change in U$ net of debt service CF. • PS debt causes negative exposure to PS.

Real Exchange Rate • Inflation adjusted exchange rate • Must account for two inflation rates: domestic and foreign • Real FX Rate at t = (Nominal FX Rate at t) X (1+Foreign Inflation Rate/1+Domestic Inflation Rate) ^ t • Important over long time horizons when inflation exerts its effect

PPP and Real FX Rates • PPP implies that real FX rates don’t change • All inflation rates cancel out • Result: real FX rate at end of period = nominal (and real) FX rate at start of period • Interpretation: If inflation is the sole cause of a change in FX rates, then the FX rates although changing in nominal terms are constant in real terms.

Nexus: PPP & Real FX Rate • Real FX appreciation means the FX appreciated too much or depreciated too little. • Real FX depreciation means the FX depreciated too much or appreciated too little. • Too much or too little using PPP as benchmark. • No change in real FX rate means the FX behaved exactly in accordance with PPP.

Compare aobserved with appp • (1+ aobserved )^T=ST / So • (1+ aPPP )^T= ST,PPP /So • really = in real terms • aobserved > appp:FX really appreciated • aobserved < appp: FX really depreciated

Thai T-Shirt Tale: application of real FX rate • Gauge profitability at start vs. end of year • Profitability = Baht profit margin per T-shirt • Two different year end scenarios examined • First scenario: Violation of PPP, nominal FX rate constant, real FX rate changes • Second scenario: Consistent with PPP, nominal FX rate changes, real FX rate constant

Thai T-Shirt Manufacturer • Incurs costs in baht • Exports to Canada, revenues in C$ • Faces Canada-based competitors in Canada • Default assumption in this course: exporter based in country X (Thailand) faces competitors in country Y (Canada) who are based in country Y • Paradigm: 2 firms competing in same market (Canada) but sourcing in 2 different countries (Canada, Thailand)

Thai T-Shirt: First Scenario • Real value of baht (currency of cost) rises • Real value of C$ (currency of revenue) drops • No nominal change in FX rate • Profit margin is squeezed • Conclusion: Profitability impaired if currency of cost appreciates or currency of revenue depreciates in real terms

Thai T-Shirt: Second Scenario • Real FX rate does not change • Nominal FX rate changes • Profitability is unaffected, real value of profit margin remains intact • Conclusion: Nominal exchange rate may change but if real exchange rate does not, profitability is not affected.