Download

1 / 9

190 likes | 692 Views

International Parity Conditions. Appendix 6A Exchange rates are influenced by interest rates and inflation rates, and together, they influence markets for exchange rates in the future, known as forward rates . The linkages among these variables are called Parity Conditions .

E N D

International Parity Conditions Appendix 6A • Exchange rates are influenced by interest rates and inflation rates, and together, they influence markets for exchange rates in the future, known as forward rates. • The linkages among these variables are called Parity Conditions. • Parity Conditions are key relationships used to predict movements in exchange rates. 2005 South-Western Publishing

Homemade Hedging of Exchange Rate Risk • If a US exporter is expecting to receive 100 Euros (€) in three months, the exporter could borrow in Euros for 3 months. Those Euros could be sold immediately for dollars, and invested for three months in the US at a known interest rate, rUS. • If the 3-month rate of interest in Europe is rEMU = 1%, the US exporter would borrow 1% less than the amount of Euros he expects to receive, or 100/1.01 = 99.01 Euros. When he receives them, he “pays off” his Euro loan with the 100 Euros he received. • If spot price of the Euros now is $1.15, he or she receives $113.86. If the 3-month US interest rate is rUS = .005, then the exporter will have $114.43. The exporter has converted an unknown value of 100 Euros three months from now into a known value of dollars.

Covered Interest Arbitrage • The forward rate in 90 days as f90, which is the rate for the Euro or other foreign currencies. • If the investor buys €100, in 90 days he has €100(1+ rEMU). • If he has already agreed to sell those Euros for dollars at f90, then he knows he’ll have €100(1+ rEMU )/ f90. • If this is larger than investing in the US, the investor is wise to do this, which is covered interest arbitrage. The ‘cover’ is the use of the forward rate. • Investors throughout the world are looking for markets with high interest rates. But high interest rates may signal a declining currency, so they try to protect against this loss using forward rates.

Interest Rate Parity • If interest rates in Europe were higher than they were in the US, no one would invest in the US so long as they thought the Euro and dollar would be stable. • The equilibrium condition is known as interest rate parity. • Let e0 be the current exchange rate price for a foreign currency. An approximation of this parity condition is given as: (f90 – e0) / e0 = [rUS - rEMU]Interest Rate Parity • Suppose interest rates in the Europe are 1% for 90 days, and only .5% in the US. We would expect the value of the Euro must fall to make investing in both countries end up with the same return. • Using the formula above, the left side is the expected forward discount. (f90 – e0) / e0 = -.005, or a half percent expected drop in the Euro over the next 90 days (3 months).

The Fischer Effect • Domestic interest rates, r, are the sum of a real return, i, and an expected change in the price level, Ex(%DCPI), which is the inflation rate. r = i + Ex(%DCPI) • It is often presumed that real returns become equal world wide. In that case, the Fisher Effect can be used to examine differences in two country’s interest rates. For the example of the US and the EMU, we have: [rUS - rEMU ] = Ex(%DCPI)US - Ex(%DCPI)EMU • This equation is known as the international fisher effect.

Relative Purchasing Power Parity • Purchasing power parity says that countries with high inflation (the p’s in the equation) have declining exchange rates. • Using “e” for exchange rates, the equation for relative PPP was given as: e1 = 1 + ph e0 1 + pf • A percentage change in an exchange rate over 90 days is (e90 – e0)/ e0 . If the foreign inflation rate is small, a useful approximation is: (e90 – e0)/ e0 = Ex(%DCPI)US - Ex(%DCPI)EMU • If inflation in the US is greater than in Europe (EMU), the value of the Euro will tend to rise and the value of the dollar fall. Similarly, if inflation is greater in Europe, the Euro will fall.

International Fischer Effect • Since differences in inflation rates tend to lead to differences in interest rates, we can use differences in interests rates predict changes in exchange rates. [et – e0]/e0 = [rUS - rEMU] • Suppose that the left side of the above equation is the percentage change in the value of the Euro measured in dollars. • When the US has higher interest rates, the Euro rises in value. • When interest rates are higher in Europe, the Euro will decline in value.

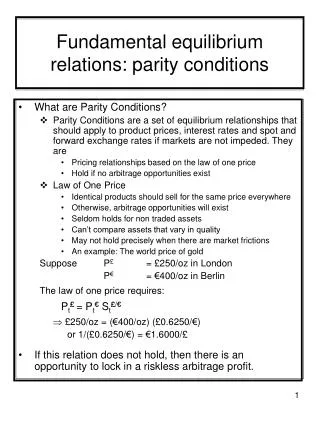

Diagram of Parity Conditions Exchange Rate Forecasts Unbiased Forward Rate Purchasing Power Parity Forward Rate Premium or Discount International Fischer Effect Differences in Inflation Rates Fisher Effect Interest Rate Parity Differences in Interest Rates Figure 6A.1 page 291

Unbiased Forward Rates • A result of the diamond-shaped diagram is that forward rates are forced by competitive pressures to signal where exchange rates are moving. • This is called an unbiased forward rate hypothesis. • If the currency Euro sells for $1.15, and the forward rate in 90 days is $1.14, the market ‘predicts’ a decline in the price of the Euro.