Download

1 / 36

360 likes | 508 Views

Summarization on supply chain finance (SCF) research in foreign countries. author:Mingsheng Yang cooperator: Shanshan Ye mentor:Zhou Jian. Research gap.

E N D

Summarization on supply chain finance (SCF) research in foreign countries author:Mingsheng Yang cooperator: Shanshan Ye mentor:Zhou Jian

Research gap • In the past, academic papers mainly dealt with the design and optimization of the flo- ws of goods and information. • The financial flows have only recently fou- nd greater attention in the academic supp- ly chain management(SCM) literature.

Origin of supply chain finance • Stemmler and Seuring (1989) were amon- gst the first authors to use the term ‘‘supp- ly chain finance’’. • They speak of the control and optimization of financial flows induced by logistics, co- mprise inventory management, the hand- ling of the logistically induced financial flo- ws as well as the supporting processes, the insurance management for stocks, for example.

Origin of supply chain finance • Pfohl et al. 2000, denominated the flow of financial reso- urces as the ‘‘financial supply chain’’ and located it at the interface between the fields of logistics and finance. • They examined the management of the net current ass- ets as an important issue within the scope of SCM. • Beyond physical reduction in stocks, they analyzed the instruments of cash management ,they consider opti- mal timing of activities, the control of receivables, liab- ilities, and advance payments. • Moreover, the optimization and support of the inven- tory and cash managements were described within the scope of process management.

Origin of supply chain finance • Stenzel (2007) defined ‘‘logistics financing’’ as another approach to the optimization of financial flows within supply chains. • It assumed an active marketing of financial serv- ices in addition to logistics services by logistics service providers. This opens up another field of financing logistics structures. • Steinmuller examines possibilities to finance log- istics real estate. and Feinen particularly deals with the leasing of logistics real estates.

Origin of supply chain finance • Fettke P (2007) used the term ‘‘Financial Chain Management (FCM)’’ in the context of financial flow research, has to be seen in contrast to the term supply chain finance. • The processes managed by the FCM are thus reduced to the processing steps of the business initiation and business transaction processes. • FCM is supposed to optimize cross-company financial processes using collaborative and automatic transactions between suppliers, customers as well as financial and logistics service providers.

Definition of SCF • Supply chain finance (SCF) is the intercom- pany optimisation of financing as well as the integration of financing processes with custo- mers, suppliers, and service providers in order to increase the value of all participating compa- nies. • The task of SCF is to save capital cost by means of better mutual adjustment or use completely new financing concepts within the supply ch-ain—eventually in combination with a changed role or task sharing.

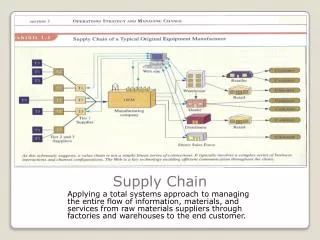

A conceptual framework of supply chain finance In order to conceptualize the term supply chain finance, it has to be examined which assets (objects) within a supply chain are actually financed by whom (actors) and on what terms (levers). These three dimens- ions add up to the framework of the SCF which is depicted in the following picture:

Dimension of SCF —objects • Objects of finance may be fixed assets and working capital. • Production facilities and stocks as well as the equipment and machines are ranked amongst the fixed assets. • Working capital comprises all those asset items of the current assets. • net working capital=circulating asset - short-term liabilities • cash-to-cash-cycle = average turnover period + period of receivables - period of payables • The cash-to-cash-cycle is a key figure to a dynamic and holistic treatment of the net working capital performance.

Dimension of SCF —Actors • Lambert refers to the suppliers, the customers, and the focal company of a supply chain as primary members, whilst logistics service providers are seen as supporting members. • If the supply chain concerning ‘‘delivery’’ of capital and financial services, financial intermediaries should be included. • Financial intermediaries in the narrow sense are specialised in the balance of asset and financial requirements between investors and acceptors. • In the broader sense, it particularly offer performances in order to allow a completion of financial contracts betw- een original and/or intermediary investors and acceptors or to effect this completion easier and cheaper respec- tively.

Dimension of SCF —levers • The dimensions of financing levers comp- rise three aspects: which amount of assets (volume of financing) needs to be financed for how long (duration of financing) at whi- ch capital cost rate? • Capital costs lever= Volume*duration time *capital cost rate

supply chain cash flow risks • A study conducted by Sloan[1] showed that the cash flow component of earnings is a better indicator of the persistence of earn- ings performance than the accrual compo- nent of earnings. • We study cash flows generated from regu- lar business operations as they are closely related to supply chain activities. [1] R.G. Sloan, Do stock prices fully reflect information in accruals and cash flows about future earnings? The Accounting Review 71 (3) (1996) 289–315

supply chain cash flow risks • Ellram[1] recognized a trend in which more corp- orate executives are now extending the supply chain manager's accountability from functional efficiency (reducing operating costs) to organiz- ation wide efficiency such as cash flow efficiency. • So, a better understanding of the relationship between supply chain performance and financial measures is critical to both supply chain and financial managers. [1]L.M. Ellram, B. Liu, The financial impact of supply management, Supply Chain Management Review (November-December2002) 30–37.

supply chain cash flow risks • The Cash Conversion Cycle (CCC), also known as the Cash-to-Cash Cycle or simply the Cash Cycle, is heavily dependent on a company's supply chain capability. • To reduce the CCC, a company can reduce days-in-inventory, shorten days-in-receivables and prolong days-in-payables. • These three time-related factors are affected by the lead time of production, credit periods of receivables and payables, and early collection/ payment patterns due to trade discounts.

supply chain cash flow risks • A potential problem of focusing on reducing the CCC is that it does not address any risk factors. For example, when a discount is offered as a means to reduce days-in-receivables, it usually increases cash inflow risks due to lacking know- ledge in predicting the amount of early collection. • Some common practices intended to reduce the CCC can lead to higher cash flow risks and de- monstrate that properly structured asset-backed securities, which acquire a fixed portion of AR, can reduce a vendor's financial costs, CCC and cash inflow risks.

Measuring cash flow risks • The CCC is one of the popular supply chain performance measures. • It contains three elements, 1) days in inventory, 2) days in receivables, and 3) days in payables, and can be expressed as: CCC=Inv/(COGS/365)+AR/(Sales/365)- AP/(COGS/365) where Inv and COGS represent average invent- ory and annual Cost of Goods Sold respectively.

Measuring cash flow risks • The three cycle times vary across industries and may depend on the market power of the organiz- ation with respect to its customers and suppliers. • Three time related factors that impose significant influences on the CCC and cash flow risks : (1) The lead time for internal processing (production and delivery) and the timing of its related cash outflows. (2) The credit periods for AR to its customers and the pattern of early collection of AR. (3) The credit periods for AP from its suppliers and the pattern of early payment of AP.

Sharing inventory risk • A supply chain may operate under either preorder mode, consignment mode or the combination of these two modes. • Under preorder the retailer takes full inventory risk during the sale; • While under consignment, the supplier taking the inventory risk. • The combination mode shares the risk in the supply chain.

Sharing inventory risk • Firms hold inventory to satisfy consumer demand, how- ever, there exists various market uncertainties, inventory overage, unexpected demand decline, for instance. • Some firms may avoid taking the risk by transferring it to the others. • Consider a supplier and a retailer. The supplier may sell the inventory to the retailer by enforcing preorder. • In contrast, the supplier may also offer consignment, where the retailer sells the product for the supplier for some commission. • A supply chain may also be operated under a combina- tion of the above two modes so that the risk is shared among the firms

Sharing inventory risk • With different allocation of the inventory risk, firms may install different inventory levels which influence the efficiency of the supply chain. • There is a stream of literature has investigated this problem: • Cachon [1] focuses on the demand uncertainty and addresses how the firms, one supplier and one retailer, will invest inventory under each supply chain mode; • Netessine and Rudi [2] address a similar problem, but in addition consider the effect of the retailer's advertising effort; and[3] they extend this problem with considering one supplier and multiple retailers; etc • [1] Cachon GP. The allocation of inventory risk in a supply chain: push, pull and advanced purchase discount contracts. Management Science 2004;50(2):222–38. • [2] Netessine S, Rudi N. Supply chain structures on the Internet and the role of marketing operations interaction. In: Simchi-Levi D, Wu SD, Shen M, editors. Handbook of quantitative supply chain analysis: modeling in the ebusiness era. New York: Springer; 2004. p. 607–42 • [3] Netessine S, Rudi N. Supply chain choice on the Internet. Management Science 2006;52(6):844–64.

Sharing inventory risk—the capital constrained • In practice, many firms are financial constrained. Financial structure and operational decisions usually cannot be separated under an imperfect capital market. • Without any capital constraint, the supplier prefers the consignment mode which operates most efficiently. • If capital constrained, he will choose the combination mode. • To share the inventory investment between the supplier and the retailer can lower the inventory risk and thus reduce the financing cost even if the retailer is highly capital constrained.

Coordination contracts related to inventory financing costs • The prior literature on supply chain coordination does not take inventory financing costs into acc- ount, and implicitly assumes that a supplier and its retailers incur zero cost of the funds for inven- tory. • Firms frequently finance their working capital from a variety of credit sources, such as banks, and incur positive financing costs. Lenders ask interest for the loans they grant. • Even in the case of zero credit default risk, lend- ers still demand positive financing costs.

Coordination contracts related to inventory financing costs • Prior studies analyze the retailer’sstocking policies at positive inventory financing costs, EOQ, for example. • Gupta and Wang (2009) have recently taken the supplier’s viewpoint, and conjecture that finance charges for inventory may be used to improve efficiency. They show the effect of finance charges on the supplier’s as well as the retailer’s profits by changing the size of the finance charge in numerical simulations.

Coordination contracts related to inventory financing costs • From a supplier’s perspective, a supplier is strategic and coordinates the supply chain as a Stackelberg leader. • The supplier’s trade-credit is a tool for supply chain coordination. • A supplier’s sharing demand uncertainty is not enough for its retailers to order the optimal quantity for the entire supply chain. • In addition, positive financing costs call for trade-credit in order to subsidize the retailer’s costs of inventory finan- cing. • Using these multiple schemes, the supplier fully coordi- nates the supply chain for the largest joint profits.

Coordination contracts related to inventory financing costs four extensively coordination mechanisms • (a) all-unit quantity discount • (b) buybacks • (c) two-part tariff • (d) revenue-sharing. • In quantity discount, two-part tariff and buyback contract, the supply chain is always better off with trade-credit , if the supplier is a credit-worthy borrower or has a sufficiently large inter- nal capital. These three contracts yield the iden- tical joint profits with trade-credit, but revenue-sharing contract is less profitable.

Financing in the cash constrained • Money acts as a catalyst if potential demand is high but finance constraints. • Sullivan (1998) found that 28% of all business bankruptcies were due to financing reasons. • We consider a simple two-stage supply chain consisting of a single manufacturer (M) and a retailer (R) under a single-period setting. • M produces goods and ships it to R with zero lead time. R returns the defective quantity to M who is liable for it. • For simplicity we assume that both the firms have no other assets but the cash available with them, before they commence their respective activities.

Financing in the cash constrained • We assume that there is a single lender (L) who is approached for a short-term loan by both the firms. M and R are small firms with no bargain- ing power. • The objective is to solve L’s problem to maxim- ize her profit under certain meaningful constrai- nts. We assume that all the three participants have an outside option of investing in a constant risk-free rate a’ per unit dollar per unit time. • The sequence of events during the period refers to the fifth reference listed below.

Difference between down flow of goods and up flow of money • In downstream flow, holding of goods and materials increase the inventory holding cost whereas in upstream flow of money, holding of money earns interest which is completely opposite. • Further, the amount of goods and materials to be delivered downstream depends on the orders placed from the downstream partner and remains constant if the order size is not changed. However, in upstream flow of money, the amount to be paid to an upstream partner will depend on the terms of payment that may include penalty for late payments and/or discounts for early payments. • These differences make the management of upstream flow of money an important and distinct research problem.

The complexity of the flow of money • First, the inflows and outflows of cash are continuous throughout an organization’s life span. These flows never cease to exist and, therefore, the problem is dynamic in nature. • Second, future cash inflows and outflows are mostly unknown, because such inflows and outflows depend on movement of goods which again depends on market demand. • Third, even if the future values of such inflows and outflows are known before hand the problem is computationally NP-Complete.

Way of modeling the supply chain finance • Due to the complexity of the supply chain finance, we must consider a simple static case of situation first, where the future receipts from distributors, and the payment terms and amounts of all suppliers are known. And we develop an integer programming mode. • Next, we can present a heuristic approach where the cash inflows from distributors are known but the amounts and payment terms from suppliers are unknown. • Lastly, we should present a dynamic solution where both the future cash inflow from distributors and upcoming pa- yment terms (invoices) from the suppliers are unknown. • Lastly, we can present the managerial implications on applicability of different solution techniques in various real life situations.

Trade credit for supply chain coordination • Trade-credit is a short-term business loan for a buyer’s purchase of goods from a seller. • There are two basic forms of trade-credit: (a) a net-term policy (e.g., net 30 days) (b) a two-part term policy (e.g., 2/10 days, net 30 days). It has three clauses: (i) discount percentage (ii) discount period (iii) net date

Trade credit for supply chain coordination • Trade-credit has been the largest source of working capital for a majority of b2b firms in the United States, and a critical source for many businesses, especially for startup and growing businesses. • Unlike prior studies that take the buyer’s perspective given a supplier’s trade-credit, Gupta and Wang (2009) have recently conjectured that trade-credit may be used to improve efficiency in the entire supply chain. They show the effect of finance charge in trade-credit on the supplier’s as well as the buyer’s profits by changing the size of the finance charge in numerical simulations.

Trade credit for supply chain coordination We take the supplier’s perspective, and present trade-credit as a tool for channel coordination. We also derive the optimal finance charge anal- ytically. Specifically, the supplier coordinates the retailer’s order quantity decisions by designing a markdown allowance and a risk premium in the trade-credit favorable to the retailer. This coordi- nation scheme enables the retailer to share the demand uncertainty and inventory financing costs with the supplier, and produce not only the largest profit for the entire supply chain, but also the supplier’s profit maximization.

Trade credit for supply chain coordination • The supplier sets a wholesale price and grants trade-credit and markdown allowance. Given the supplier’s offer, the retailer determines the order quantity and the financing option for the inventory, either trade-credit or direct financing from a traditional lender such as a bank. • We can derive the optimal markdown allowance and risk premium. These two incentives entice the retailer to choose the same order quantity as in a fully integrated supply chain. Given that the supplier maximizes profit through coordination, the firm increases its own portion of the joint profit by raising the wholesale price. Traditio- nal lenders may have an information disadvantage when it comes to market demand, and may quote a higher risk premium to the retailer than the expected bankruptcy loss.

REFERENCES • 1 Hans-Christian Pfohl • Moritz Gomm (2009) Supply chain finance: optimizing financial flows in supply chains. Logist. Res. 1:149–161 2-11页 • 2 Chih-Yang Tsai(2008)On supply chain cash flow risks. Decision Support Systems 44 (2008) 1031–1042 12-17页 • 3 Guoming Laia,*, Laurens G. Deboa, KatiaSycarab (2009) Sharing inventory risk in supply chain: The implication of financial constraint. Omega 37 (2009) 811 – 825 18-21页 • 4 Chang Hwan Lee , Byong-Duk Rhee (2010) Coordination contracts in the presence of positive inventory financing costs. Production Economics 124 (2010) 331–339 22-25页 • 5 N.R. Srinivasa Raghavan, Vinit Kumar Mishra(2009) Short-term financing in a cash-constrained supply chain. Production Economics 134 (2011) 407–412 26-27页 • 6 Sushil Gupta, Kaushik Dutta (2010) Modeling of financial supply chain. European Journal of Operational Research 211 (2011) 47–56 28-30页 • 7 Chang Hwan Lee, Byong-Duk Rhee.(2010) Trade credit for supply chain coordination. European Journal of Operational Research 214 (2011) 136–146 31-34页

THE END THANKS !