Download

1 / 30

300 likes | 394 Views

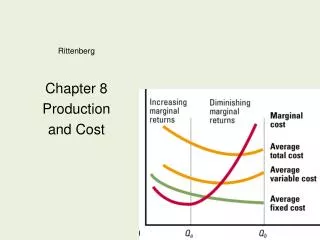

8. Production Function and Cost. Chapter 8 : main menu. Progress Checkpoint 1. Statement 1 : If there is at least one variable factor, it is a short-run period Statement 2 : If there is at least one variable factor, it is a long-run period. Which statement is correct? Are both correct?.

E N D

Progress Checkpoint 1 • Statement 1 : If there is at least one variable factor, it is a short-run period • Statement 2 : If there is at least one variable factor, it is a long-run period. • Which statement is correct? Are both correct?

Progress Checkpoint 1 • Statement 1 is incorrect. In short run, there is at least one fixed factor. It is possible that all factors may be fixed. • Statement 2 is incorrect. In long run, all factors are variable. If there is a variable factor with a fixed factor, it is still a short run.

Progress Checkpoint 1 • Sam operates a photocopying shop. He is considering two plans in expanding his shop : • Plan 1 : Use more photocopying papers, employ more workers but keep the number of photocopying machines unchanged. • Plan 2 : Use more of all factors of production. • Which is a short run and which is a long run expansion plan? • How will the scale of production be affected by EACH plan?

Progress Checkpoint 1 • Plan 1 is a short run expansion plan, because a fixed factor (the photocopying machines) exists. The scale of production will not change. • Plan 2 is a long run plan, because all factors are variable. The scale of production will be enlarged.

Concept Explorer 8.1 • What are the values of TP and AP of each unit of labour? • After which unit of labour does diminishing (marginal) returns set in? • At which unit of labour is average product at its maximum?

Concept Explorer 8.1 • Diminishing returns sets in after the unit of labour is employed, as MP begins tod thereafter. • The average product is at its maximum (=7.75) when the unit of labour is employed. 0 3 9 21 31 38 42 42 - 3 4.5 7 7.75 7.6 7 6 3rd iminish 4th

Concept Explorer 8.2 • Reasons for diminishing (marginal) returns • Why does diminishing (marginal) returns happen in reality? • Why does it happen only in the short run?

Concept Explorer 8.2 • Reasons for diminishing (marginal) returns • In short run, initially when a few labour is employed, the fixed factor is not fully utilized. • When more labour is employed, division of labour can be adopted, cooperation among workers is possible, and workers also learn from experience. • This will increase marginal product.

Concept Explorer 8.2 • Reasons for diminishing (marginal) returns • However, when more labour is continuously added, coordination among factors of production becomes difficult. • Also, the fixed factor may be insufficient for the increasing number of workers to use. • Hence, marginal product will eventually diminish.

Concept Explorer 8.3 • Is the law of diminishing (marginal) returns illustrated? • Mr. Chan is the owner of a DVD player producing firm. • The number of machines used in his firm is fixed. • He observes the following decrease in daily output when some workers are absent from work due to sickness : • Is the law of diminishing (marginal) returns illustrated in Mr. Chan’s firm?

Concept Explorer 8.3 • We can transform the above table into the following by assuming that : • Mr. Chan’s firm normally employs 10 workers, and • the daily output of his firm is 100 units of DVD player. 5(5 absentees) 6(4 absentees) 7(3 absentees) 8(2 absentees) 9(1 absentee) 10(assumed) 26(= 100 - 74) 47(= 100 - 53) 67(= 100 - 33) 84(= 100 - 16) 96(= 100 - 4) 100(assumed) 21(= 47 - 26) 20(= 67 - 47) 17(= 84 - 67) 12(= 96 - 84) 4(= 100 - 96) -

Concept Explorer 8.3 • Mr. Chan’s firm is in short run because machines are a fixed factor. • We can see that when more and more workers are added, the marginal product diminishes. • Thus the law of diminishing (marginal) returns is illustrated in his firm.

Theory in Life 8.1 • Famine and the law of diminishing (marginal) returns • It is said that if the law of diminishing (marginal) returns did not hold, there would not be famine anymore. Why?

Theory in Life 8.1 • If the law of diminishing (marginal) returns did not hold, then when more and more farmers (a variable factor) worked on a farmland (a fixed factor), marginal product (in terms of agricultural product) would not fall. • This implied that the total product would be ever increasing. • There would be no limit to the amount of agricultural product grown from a piece of land. • Famine could be avoided.

Theory in Life 8.1 • However, it is observed that many countries in the world suffer from famine. • This implies that the amount of food grown on farmland is not sufficient to avoid famine, and there is a limit on the total product of a piece of farmland. • The law of diminishing (marginal) returns is empirically confirmed.

Progress Checkpoint 2 • Consider the following input-output relationship of a firm : (a) What are the values of AP and TP of EACH unit of labour? (b) After which unit of labour does diminishing returns set in? (c) At which unit of labour is average product at its maximum?

Progress Checkpoint 2 (a) • Diminishing (marginal) returns begins to set in after the unit of labour is employed • Average product is at its maximum at 16 when the unit of labour is employed. 0 9 24 42 62 80 93 98 - 9 12 14 15.5 16 15.5 14 4th 5th

Theory in Life 8.2 • Fixed and variable costs of a fast food shop • Raymond operates a fast food shop in a shopping centre. The following list shows some of the cost items of his shop : • Rent of the shop • Water charges • Labour cost • Expenses on food • Management fee of the shopping centre • Fire insurance payment • Which of the above are fixed costs? • Which are variable costs?

Theory in Life 8.2 • Fixed and variable costs of a fast food shop • Raymond operates a fast food shop in a shopping centre. The following list shows some of the cost items of his shop : • Rent of the shop • Water charges • Labour cost • Expenses on food • Management fee of the shopping centre • Fire insurance payment • Which of the above are fixed costs? • Which are variable costs? Fixed costs they remain constant no matter whether more output is produced. Variable costs they increase when more output is produced.

Concept Explorer 8.4 • Calculation of total, average and marginal costs • What are the values of the unknowns in the following table? • What is the amount of fixed cost? • At which unit of output does diminishing returns set in? • At which unit of output is average cost at its minimum?

Concept Explorer 8.4 • At 2 units of output, • TC = AC x Q = $7.5 x 2 = $15, or • TC = TC(Q = 1) + MC(Q = 2) = $10 + $5 = $15 • At 3 units of output, • AC = TC $18 = = $6 Q 3 • At 4 units of output, • MC = TC (Q = 4) - TC (Q = 3) = $23 - $18 = $5

Concept Explorer 8.4 • When Q = 0, VC = $0 and TC = $3. Therefore, • TC = FC + VC • $3 = FC + $0 • $3 = FC • The amount of fixed cost is $3. • Marginal cost and marginal product are inversely related. As marginal cost starts to increase after 3 units of output are produced, marginal product starts to decrease. Diminishing returns set in after 3 units of output are produced. • Average cost is at its minimum at $5.75 when 4 units of output are produced.

Concept Explorer 8.5 • Suppose labour is the only factor required in the production process of a firm. The following shows some information of the firm in two months : • If the market price of the firm’s product is fixed at $5, what are the values of total revenue, total cost, average cost and profit for the firm in each month? • How does average cost change in the period?

$200 $360 = = 50 100 Concept Explorer 8.5 • We can observe that when the firm doubles its output by doubling its labour employed, the profit increases by more / less than double. • This is because the average cost is higher / lower. $250 ( = $5 x 50) $500 ( = $5 x 100) $200 ( = $20 x 10) $360 ( = $18 x 20) $4 $3.6 $50 ( = $250 - $200) $140 ( = $500 - $360)

Progress Checkpoint 3 • Consider the following cost-output relationship of a firm : • Complete the above table. • What is the amount of fixed cost? • At which unit of output does diminishing returns set in? • At which unit of output is average cost at its minimum?

Progress Checkpoint 3 • At 1 unit of output, TC = $22 and MC = $12. Therefore the total cost at 0 unit of output is $10 (= $22 - $12). TC $35 At 4 units of output, AC = = = $8.75 Q 4 TC $39 - $35 At 5 units of output, MC = = = $4 Q 5 - 4 • The amount of fixed cost is $10.

Progress Checkpoint 3 • Marginal cost and marginal product are inversely related to each other. • As marginal cost starts to increase after 4 units of output are produced, marginal product starts to fall. • Diminishing returns set in after 4 units of output are produced. • Average cost is at its minimum at $7.8 when 5 units of output are produced.