Download

1 / 20

200 likes | 216 Views

Discover how to convert life insurance policies into benefits for long-term care, protect assets, and gain financial independence. Learn about regulatory structures and real cases of policy transformation. Find out about various options and government benefits available.

E N D

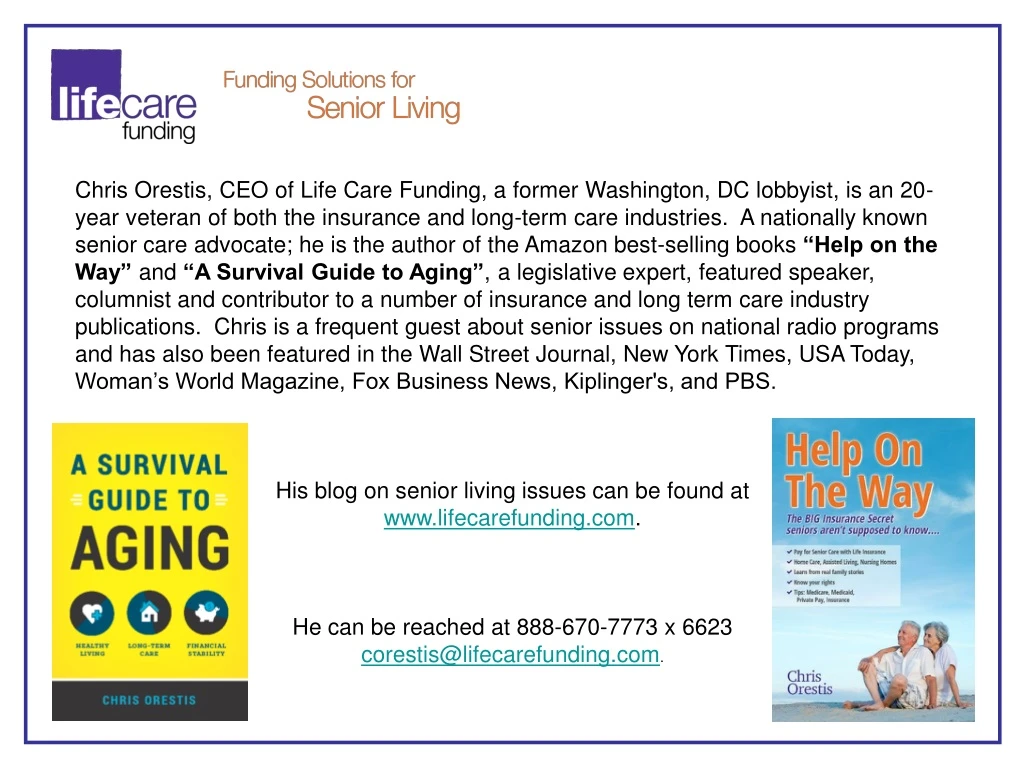

Chris Orestis, CEO of Life Care Funding, a former Washington, DC lobbyist, is an 20-year veteran of both the insurance and long-term care industries. A nationally known senior care advocate; he is the author of the Amazon best-selling books “Help on the Way” and “A Survival Guide to Aging”,a legislative expert, featured speaker, columnist and contributor to a number of insurance and long term care industry publications. Chris is a frequent guest about senior issues on national radio programs and has also been featured in the Wall Street Journal, New York Times, USA Today, Woman’s World Magazine, Fox Business News, Kiplinger's, and PBS. His blog on senior living issues can be found at www.lifecarefunding.com. He can be reached at 888-670-7773 x 6623 corestis@lifecarefunding.com.

Founded in 2007, Life Care Funding specializes in converting the death benefit of an in-force life insurance policy into a Long Term Care Benefit plan to cover the costs of Homecare, Assisted Living, Skilled Nursing Home Care and Hospice.

Policy experts, patient advocates and members of Congress warned of a “silent crisis” affecting nearly every American family: The inability to pay for long-term care, even as the population most at risk continues to grow. - The Gupta Guide (MedPage Today)

Problem- • Families confronting Long Term Care are unprepared, uninformed and are looking for comprehensive advice and access to options • Seniors want to remain financially independent and in control of care decisions • Seniors don’t want to be a burden on their family or become a ward of the state • Solution- • Numerous options to remain private pay are available • Converting an existing life insurance policy into a Long Term Care Benefit Plan is a mainstream option that every attorney and advisor needs to know about

Alarming Liabilities • OBRA ’93 / DRA (Mandates to recover $) • Filial Responsibility Laws (28 states) • Health Care & Retirement Corporation of America v. Pittas (Pa. Super. Ct.) • Larry Grill et al v. Lincoln National Life Insurance Company (California Central District Court) • Families and Advisors are being held liable for poor financial planning and punitive court cases are mounting

A Life Insurance Policy is legally protected as personal property by the US Supreme Court and the policy holder has the guaranteed right to use it to pay for Long Term Care and Housing. A Life Insurance Policy is a Financial Asset just like a stock or bond. Supreme Court case Grigsby v. Russell (1911) Justice Oliver Wendell Holmes

Alarming Liabilities • OBRA ’93 / DRA (Mandates to recover $) • Filial Responsibility Laws (28 states) • Health Care & Retirement Corporation of America v. Pittas (Pa. Super. Ct.) • Larry Grill et al v. Lincoln National Life Insurance Company (California Central District Court) • Families and Advisors are being held liable for poor financial planning and punitive court cases are mounting

Seniors in the US own approximately $500 billion* of life insurance Very limited options to access value in a policy Stop paying premiums and lapse or abandon policy • Can’t afford premiums? • Need to qualify for Medicaid? Surrender policy back to insurance company (usually less than 10% of face value) 88% of policies lapsed or surrendered for little or no value 38% of Medicaid applicants must liquidate policy to qualify *Source: Conning and Company Research

Convert a Life Insurance Policy into a Long Term Care Benefit Plan • No costs whatsoever to family or advisor • Funds deposited into an irrevocable, FDIC insured bank account • Automatic, payments are made directly to a provider of long term care • Monthly payments can be adjusted to address changing care needs • Funeral benefit and any account balance paid to family • Tax-free account and Medicaid qualified spend-down • Qualified for VA Aid and Attendance Benefit

Enrollment Example #1 Case Study: 37651290D Policy owner: 86 MalePolicy value: $90,000 (UL) Lapse Value: $0 Cash Value: $0 Life Care Benefit: $31,500 or 30% of death benefit • $1,800 monthly Benefit payment to Assisted Living community for duration of benefit period. • $4,500 Final Expense benefit issued at maturity.

Enrollment Example #2 Case Study: 14793181H Policy owner: 70 MalePolicy value: $250,000 (term) Lapse Value: $0 Cash Value: $0 Life Care Benefit: $150,000 or 60% of death benefit • $30,000 initial benefit payment to cover out-of-pocket expenses to retrofit home and purchase specialty bed. • $10,000 monthly Benefit Payment for duration of benefit period. • Account balance of $70,000 and $5,000 Final Expense benefit issued at time of death.

Regulatory Structure: Policy Transfer- Adheres to secondary market regulations governing life settlement market. Benefit Account- Adheres to Banking regulations. Use of Funds- Adheres to Medicaid and VA regulations. Available- All 50 states

In 2010, the National Conference of Insurance Legislators unanimously passed the Life Insurance Consumer Disclosure Model Law. Conversion of a life insurance policy into a Long Term Care Benefit Plan is one of the mandated options in the Model Law. Multiple states have introduced Life Policy Conversion Consumer Disclosure Laws Granting Medicaid Departments authority to educate citizens they have right to convert life policies to pay for any form of care they select. : CA, FL, GA, KY, LA, MA, MD, ME, NJ, NY, PA, TX, and WA

Life Care Funding has attracted positive attention from the press and policymakers “…Life Care Funding puts the money in an FDIC insured account used to send monthly payments directly to a long term care provider…You can switch from one provider to another as your needs change; but you can’t use the money for a vacation (or blow it at a casino).” 10/9/2013 “But a few state law makers who have introduced laws to publicize the [Benefit Plan] option have pointed out that it beats surrendering a policy to access government benefits while also giving families more control over how to spend the money.” 8/30/2013 “Texas enacted a law earlier this month that gives state Medicaid officials the authority to tell people applying for help they can sell long-held life-insurance policies to a third party to pay for custodial health care of their choice.” 6/27/2013

Accepted by all Long Term Care Providers in the U.S.

There are just two criteria to qualify for a Benefit Plan • Life policy of $50,000 and above in danger of lapse/surrender • Universal, term, group, federal • Variable is possible but requires additional paperwork • High cash value whole life usually does not work • Immediate need to fund care • Limited savings and desire to preserve home • Desire to remain private pay rather than go on State assistance • Need to divest asset to eventually qualify for Medicaid • Delay in collecting Veteran’s benefits • Delay in collecting on LTCi policy • Automatic declines for an LTCi policy • Need to supplement LTCi or Veteran’s benefits

Which audiences can be best helped by the Benefit Plan? • Families with an immediate need to fund care for a loved one • Current clients (or their parents) that want to remain private pay rather than go on State assistance • Automatic declines for an LTCi policy • The parents of someone you are selling an LTCi policy to • Parents or attendees of your current seminars • If you have existing relationships with CPAs or Attorneys their clients • If you have current AL community relationships you can help their resident remain private pay longer • Compensation based on policy face for licensed producers (life settlement regs.) • Note: Exemption for CPAs, CFPs, Attorney

Application Process • SIMPLE and QUICK process— • 1) Application (est. 10 minutes) • Simple application (3 pages) • Signed HIPAA and Insurance Authorization Forms • Provide available policy and medical information • 2) Underwriting: APS review and phone interview (est. 7 business days) • 3) Enrollment: Packets sent to agent to present to family (est. 3 weeks) • HELP DESK available

Who Benefits and How? • Consumer: Convert an asset they already own and will abandon into a long term care benefit plan that will provide private pay dollars to their preferred form of senior housing and care while preserving a portion of the death benefit for the family. • Provider: Long term care service provider receives private pay funding for services (1/3 higher than CMS rate) over a guaranteed timeframe without disruption from cutbacks in Medicaid reimbursements. • Medicaid and Tax Payers: Medicaid qualified spend down of policy extends the ability to keep a person private pay and delay entry onto Medicaid generating considerable savings to stressed Medicaid budgets and tax payers-- (FL estimated $150M annual1). • 1 Florida State University Center for Economic Forecasting and Analysis, Scoring Medicaid Savings of HB 1055: Conversion of Life Insurance Policies to Long Term Care Benefit Plans in Florida, published January, 2012

Life Care Funding Phone: 888-670-7773 info@lifecarefunding.com www.lifecarefunding.com