Download

1 / 12

120 likes | 272 Views

QIS5: Process, timeline and main results. Press Briefing Frankfurt, 22 March 2011. Objectives of QIS5. Commission’s Call for Advice (July 2010): Quantitative impact Check principles and calibration targets Encourage (re)insurers and supervisors to prepare for the introduction of Solvency II

E N D

QIS5: Process, timeline and main results Press Briefing Frankfurt, 22 March 2011

Objectives of QIS5 Commission’s Call for Advice (July 2010): Quantitative impact Check principles and calibration targets Encourage (re)insurers and supervisors to prepare for the introduction of Solvency II To provide a starting point for an ongoing dialogue between supervisors and (re)insurers Also: EIOPA to test feasibility and assess complexity

QIS5 process Ownership of technical specifications: European Commission “Double” calculations (no default approach set by the EC) Calculation with and without transitional provisions for discounting Internal Models and Standard Formula calculation Modular approach and equivalent scenario for the adjustment for the loss-absorbing capacity of technical provisions and deferred taxes Groups: accounting consolidation as well as aggregation and deduction method “Alternative” approaches: QIS5 to collect information to assess the impact of the issues and/or enable comparisons on potential alternatives (default defined by EC) Value of participations based on SCR of the undertaking in which the participation is held Introduction of the illiquidity premium in risk free rate Risk margin with diversification between lines of business (solo) without diversification between entities at group level Transitional provisions for own funds Tiering of expected profits in future premiums EIOPA and Commission verifying national guidance

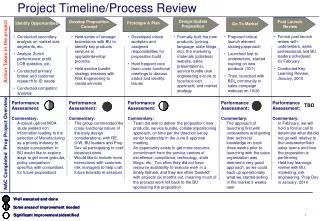

QIS 5 timeline Consultation technical specifications National analysis / quality check Jan. 2010 Jul. 2010 Nov. 2010 Mar. 2011 Draft technical specifications Running of the exercise European Report Apr. 2010 Aug. 2010 Jan. 2011

QIS 5 was a field test! “On the one hand, the quantitative results of QIS5 allow identifying major trends and drawing conclusions about the “big picture”. On the other hand, supervisors consider that the detail of the quantitative results should be treated with caution.” 220 Q&A

Participation solo Participation rate More than doubled solo participation • 1511 Small • 791 Medium • 217 Big • 610 Life • 1284 Non-Life • 111 Reinsurers • 175 Captives • 336 Composites • 382 Health • 454 Mutual

Participation groups Groups: QIS4: 106 QIS5: 167 Increase in number of small and medium groups

Conclusions Industry remains overall well capitalised Need to reduce complexity Further work needed to improve calibration (e.g. in non life underwriting or catastrophe risks) 3 areas identified where transitionalswill make full sense: equivalence, hybrids and technical provisions EIOPA to undertake development of Technical Standards and Guidelines to ensure a consistent implementation and enhance practicability and feasibility

Thank youFor questions, please contactSybille Reitz, EIOPA Press Officepress@eiopa.europa.eu Perrine Kaltwasser, EIOPA, QIS5 TF leader