Download

1 / 23

230 likes | 328 Views

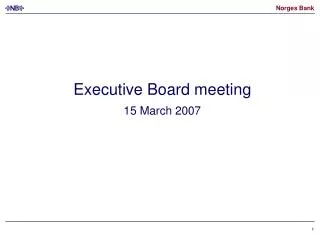

Executive Board meeting 27 June 2007. Growth forecasts Consensus Forecasts GDP. Percentage change on previous year. 2007. 2008. 2. Source: Consensus Forecasts.

E N D

Growth forecasts Consensus ForecastsGDP. Percentage change on previous year 2007 2008 2 Source: Consensus Forecasts

House prices1) and housing starts in the US Seasonally adjusted. 12-month rise2) January 2003 – May 2007 (Housing starts April) New dwellings Existing dwellings 1) Median price for dwellings 2) 3-month moving average Housing starts 6 Sources: Reuters and Norges Bank

Equities Indices,1 November 2006 = 100. 1 November 2006 – 25 June 2007 US Euro area Norway US Japan Emerging economies 7 Source: Reuters

Oil price Brent Blend and futures prices USD per barrel. 3 January 2002 – 25 June 2007 25 June 2007 Previous monetary policy meeting (29 May 2007) 8 Sources: Telerate, IPE and Norges Bank

Current key policy rate for the G-10 currencies, and market expectations for the next 3 and 12 months1) 1)At 26 June 2007. 9 Sources: Bloomberg and Reuters

Change in international effective exchange rates since MPR 1/07At 25 June 2007 10 Sources: Norges Bank, Bank of England and Bloomberg

25 June 2007 Previous monetary policy meeting (29 May) Key policy rates and forward ratesAs at previous monetary policy meeting and at 25 June 2007 UK Euro area US Sweden 11 Sources: Reuters, Bloomberg and Norges Bank

Interest rate paths Sweden Market after MPR 2 Market before MPR 2 MPR2 Market before MPR 1 Market after MPR 1 MPR1 12 Sources: Reuters and Norges Bank

3-month interest rate differential and import-weighted exchange rate (I-44) 1) January 2002 – December 2010 I-44 (left-hand scale) I-44 at 25 June 2007 Average 1 - 25 June 2007 Previous monetary policy meeting (29 May 2007) 25 June 2007 Weighted interest rate differential (right-hand scale) 1) A rising curve denotes an appreciation of the krone. 13 Sources: Bloomberg, Reuters and Norges Bank

Yields on 10-year government bonds 1 January 2006 – 22 June 2007 UK US Euro area Norway Sweden Sources: Reuters

Various inflation indicators12-month change. Per cent. January 2002 – May 2007 Weighted median CPI-ATE 20 per cent trimmed mean CPI 14 Source: Statistics Norway

CPI-ATE Total and by supplier sector. Projections MPR 1/07. 12-month rise. Per cent. June 2004 – May 2007 Domestically produced gods and services (0.7)1) CPI-ATE Imported consumer goods (0.3)1) 1) Norges Bank's projections. 13 Sources: Statistics Norway and Norges Bank

CPI-ATE Total and by supplier sector. Projections MPR 2/07. 12-month rise. Per cent. June 2004 – May 2007 Domestically produced gods and services (0.7)1) CPI-ATE Imported consumer goods (0.3)1) 1) Norges Bank's projections. Sources: Statistics Norway and Norges Bank

Regional network - expectations of a rise in sales prices in the next 12 monthsDiffusion index¹) Domestically oriented manufacturing, building and construction and corporate services Retail trade and household services ¹) Share that answer higher + (0.5 x share that answer unchanged). 15 Source: Norges Bank

Capacity utilisation and labour supply Will the enterprise find it difficult to accommodate an (unexpected/expected) rise in demand? Per cent Capacity utilisation Labour supply 17 Source: Norges Bank

House prices 12-month rise, annualised seasonally adjusted monthly rise and annualised rise in 3-month, moving, centred average. Per cent January 2002 – May 2007 Annualised rise in 3-month moving average 12-month growth. Seasonally adjusted monthly rise, annualised 18 Sources: Norwegian Association of Real Estate Agents, ECON, Finn.no, Association of Real Estate Agency Firms and Norges Bank

Growth in domestic credit (C2) to households Per cent. Monthly figures. January 2002 – April 2007 12-month growth Growth in 3-month moving average, annualised 19 Sources: Statistics Norway and Norges Bank

Property prices and corporate debt and liquid assetsChange on same month/half year previous year. Per cent. January 2001 – April 2007 (C3 March) Commercial property prices Debt1) and liquid assets2) Money supply (M2) Total credit (C3) 1) Mainland non-financial enterprises (C3). 2) Non-financial enterprises' liquid assets (M2). Sources: Statistics Norway and Norges Bank 20

Actual ARIMA MPR 2/07 BVAR Monthly indicator VAR Regional network Mainland GDP Growth on previous quarter. Seasonally adjusted. Per cent 2005 Q1 – 2007 Q31) 1) Projection for 07 Q2 and 07 Q3. See the box "Short-term projections for mainland GDP growth" in Inflation Report 2/06 for a description of the different models. 21 Sources: Statistics Norway and Norges Bank

Baseline scenarios in MPR 1/07 and MPR 2/07 Output gap Key policy rate MPR 2/07 MPR 2/07 MPR 1/07 MPR 1/07 CPI-ATE CPI MPR 2/07 MPR 2/07 MPR 1/07 MPR 1/07 Sources: Statistics Norway and Norges Bank 22

Key policy rate in baseline scenario and estimated forward rates1)Per cent. At 25 June 2007 Baseline scenario MPR 2/07 Market 25 June 2007 Market before MPR 1/07 (14 March) I) A credit risk premium and a technical difference of 0.20 percentage point have been deducted to make the forward rates comparable with the key policy rate. 23 Sources: Reuters and Norges Bank