Download

1 / 8

80 likes | 88 Views

Explore the evolution of the global carbon market post the Durban outcomes. Analyze the impact on CDM and JI projects, trading schemes, and the international offset standards landscape. Assess the current challenges and opportunities facing the market.

E N D

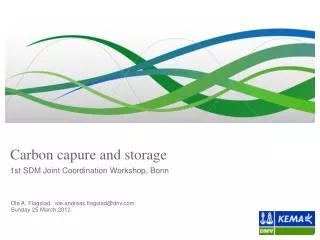

First SDM Joint Coordination WorkshopInitial Plenary: Durban Outcomes Bonn, 24February 2012 Henry Derwent

A reminder of how the international carbon market was supposed to work Kyoto Land Non-Annex1 (Dev’g Countries) K2 K1 NA1 Trading Scheme between Installations etc K3 CDM Projects Airland JI Projects

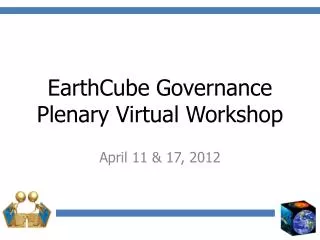

The way the global carbon market is going Country 1 Country 2 CDM System and developments Trading Scheme Domestic Projects National/local offset standards (EPA, California) Bilateral systems or deals Global Sector National Sector or City International offset standards (VCS, CCX, CCBA)

Offset Projects 2012: a Toxic Mixture of objections • Purchasing indulgences: corporates or individuals • « Anyway » tonnes: Can’t trust foreigners • « Anyway » tonnes: Can’t trust baselines • Contaminated currency (domestic and linking) • Allows putting-off domestic investment • The ghosts of low-hanging fruit • International negotiations: « Supply only » days are over • EUETS over-supply • Objections in principle to some meths • Integrity of land-use meths? • Emerging trading schemes not taking someone else’s rejects « Everybody knows the CDM doesn’t work» « The CDM is evil »

Primary CDM picture looks very bad CDM activity declined because: reduced compliance needs due to slow economic recovery uncertainty re: post-2012 rules less origination activity as buyers seek predictable credits and fewer projects competition with AAUs and secondary CERs Lower demand from EUETS Durban’s improvements not enough to change this CDM value(US$ billion -12% -59% -46%

Durban’s Improvements to the Mechanisms • Doubt about continuation of CDM (and JI?) removed • Materiality regime agreed • Pointers in the right direction on: significant deficiences, simplification, co-benefits, additionality, first of a kind, faster processing of methodologies, consequences of methodologies being put on hold, standardised baselines, suppressed demand, digitisation, reduced waiting times, support for underrepresented countries, loan scheme, new DOEs • Better understanding for the users’ experience, better norms of communication, and the rule of law • CCS • Appeals mechanism not agreed • But EU-ETS close-down (impacts on EU MS too) now beginning to be understood

Focus for this Workshop • Large number of issues on the table • Golden thread: effective functioning of the market • Kyoto Project Mechanisms under threat like never before • Participants leaving while need is rising • Going forward, little compelling reason for private sector to stay interested • A system that works is the best defence

www.ieta.org CLIMATE CHALLENGES, MARKET SOLUTIONS MAKING MARKETS WORK FOR THE ENVIRONMENT