Download

1 / 6

60 likes | 323 Views

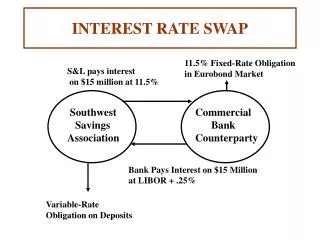

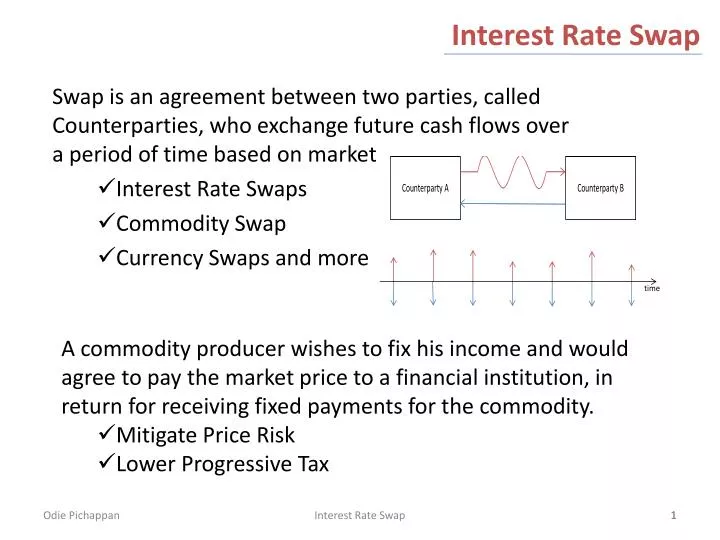

Interest Rate Swap. Swap is an agreement between two parties, called Counterparties, who exchange future cash flows over a period of time based on market Interest Rate Swaps Commodity Swap Currency Swaps and more.

E N D

Interest Rate Swap Swap is an agreement between two parties, called Counterparties, who exchange future cash flows over a period of time based on market • Interest Rate Swaps • Commodity Swap • Currency Swaps and more • A commodity producer wishes to fix his income and would agree to pay the market price to a financial institution, in return for receiving fixed payments for the commodity. • Mitigate Price Risk • Lower Progressive Tax Interest Rate Swap 1

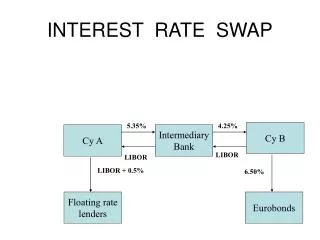

Swap Terminology Long Swap (Buyer) Counterparty that receives variable/floating cash flow Short Swap (Seller) Counterparty that is paying variable/floating cash flow Buyer Party-A Payer Seller Party-B Receiver Fixed to Floating Floating to Fixed Payer – counterparty that pays fixed rate. Receiver – counterparty that receives fixed rate. Interest Rate Swap

Swap Terminology • Day count convention (Yield basis) – determines how interest accrues over time period (Actual/360 float, 30/360 fixed). • ISDA - International Swaps and Derivatives Association, Inc. • Notional principal – amount on which the periodic payment of cash flow is calculated. • Payment period – interest calculation period and cash exchanged at the end of the period. • Rate fixing – normally done 2 days before start of period. • Tenor – Maturity of the swap Interest Rate Swap 3

Comparative Advantage • Apple Inc wants to borrow at floating rate and Boeing Co wants to borrow at fixed rate, under following borrowing rates. • Apple has relative advantage in fixed market and Boeing has relative advantage in floating market. • The total arbitrage gain by entering into a swap deal would be 1.41% - 1.23% = 0.18% • Design a swap where the gain are equally shared between the 2 companies and the swap dealer. Interest Rate Swap 4

Comparative Advantage Calculation gained 6 bps gained 6 bps gained 6 bps LIBOR LIBOR Boeing Net 7.60% Apple Net L+1.05 5.26% 5.20% LIBOR + 2.34% 6.25% Both counterparties gained 6 bps by borrowing in their preferred market where they have comparative advantage. Interest Rate Swap 5

Counterparty Report Interest Rate Swap 6