Download

1 / 14

160 likes | 536 Views

Mechanics of an Interest Rate Swap. Ahmad Sharif Pour Date: June 1, 2011. Agenda . Overview of Interest Rate Swap Valuing Interest Rate Swap Risks Associated with Interest Rate Swap Reasons for the Rapid Growth of Interest Rate Swap Market. Interest Rate Swap .

E N D

Mechanics of an Interest Rate Swap Ahmad Sharif Pour Date: June 1, 2011

Agenda • Overview of Interest Rate Swap • Valuing Interest Rate Swap • Risks Associated with Interest Rate Swap • Reasons for the Rapid Growth of Interest Rate Swap Market.

Interest Rate Swap • Interest rate swap transactions began in 1981 • Eurobond as principal security • The largest component of the OTC interests rate derivatives market • As of December 2010, national amount outstanding ($364 trillion) • Gross market value ($13 trillion)

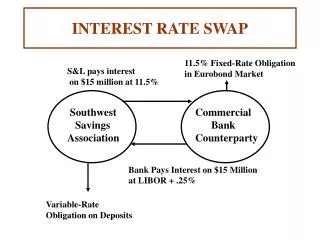

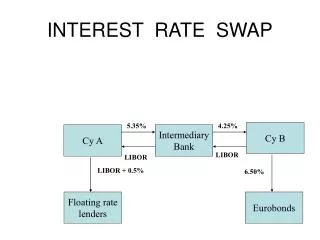

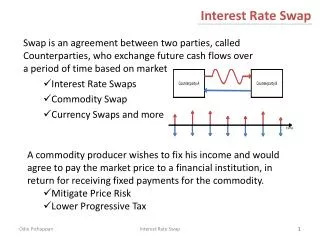

An Overview of Interest Rate Swaps • An agreement between two counterparties • Exchange periodic interest payments based on predetermined principal value • Time frame • Notional principal amount • Fixed interest rate (Fixed-rate payer) • Floating interest rate (Floating-rate payer) • Treasury bills, LIBOR (London Interbank Offered Rate), commercial paper, bankers acceptance, certificates of deposit, federal funds rate, and prime rate • Payment dates

Fixed Rate Firm A (Payer) Firm B (Receiver) Floating Rate Time Frame: 5 years Notional principal amount: $50 Million Fixed rate: 10% Floating rate: six-month LIBOR Payment dates: Every six months

How Interest Rate Swaps are used • Applications of Interest Rate Swaps • Alter Cash flow of asset to provide a better match between assets and liabilities • Asset Swap • Alter cash flow of assets from fixed to floating or from floating to fixed without affecting the underlying assets. • Liability Swap • Alter cash flow of liabilities from fixed to floating or from floating to fixed without affecting the underlying assets

Asset Swap 10% 9.5% Firm A Financial Intermediary Firm B LIBOR + 60 bps LIBOR + 40 bps LIBOR + 150 bps 10% Financial Intermediary Net: .7% Bond Bond Net = [(LIBOR + 150 bps + 10%) - LIBOR + 60bps] = 10.9% Net = [(10%+ LIBOR + 40bps) – 9.5%] = LIBOR + 90bps

Interest Rate Swap Valuation • Summing the present value of cash flow • 1st step: calculate the present value of floating rate payments • 2nd step: calculate the present value of the notional principal. Then, multiply it by the days in the period • LIBOR futures rate as discount rate • 3rd step: calculate the swap rate • Divide the results from step 1 by results from step 2 • Result is the fixed rate that the party is willing to pay in return for receiving the 6-month LIBOR

Interest Rate Swap Risks Interest Risk

Interest Rate Swap Risks-Cont. • Credit risk • Occurs when counterparties default on the swap agreement • Only one party at a time will be subject to credit risk • Example • Suppose company A pays 8% and company B pays 6-month LIBOR • Now, if market rate on swaps falls below 8%, company B benefits and company A may default. • Company B suffers a credit loss if company A goes bankrupt • What happens if the interest rate increase to 9%?

Reasons for the Rapid Growth of Interest Rate Swap Market • Ability of institutional investors and corporate borrowers to changes the nature of their assets and liabilities • Credit arbitrage opportunities • Comparative advantage • Increased volatility of interest rates • Caused borrowers and lenders to hedge or manage their risk exposure • Interest rate swap is more liquid than forward rate contract

Take-away • Interest rate swap is an agreement between two counterparties to exchange periodic interest payment • Notional principal amount is not exchanged. Rather the interest rate times notional principal amount is exchanged. • Alter cash flow of assets from fixed to floating or from floating to fixed without affecting the underlying assets. • Interest rate valuation methods: • Summing present value of cash flows • YTM and zero coupon method • Interest rate swaps risks • Interest risk • Credit risk

References • 5/24/2011, Amounts outstanding of over-the-counter (OTC) derivatives, http://www.bis.org/statistics/otcder/dt1920a.pdf • Fabozzi, Frank. Modigliani, Franco. and Jones, Frank. 2010, Foundations of Financial Markets and Institutions(Pearson Prentice Hall) • 5/24/2011, Understanding Interest Rate Swap Math and Pricing, http://www.treasurer.ca.gov/cdiac/publications/math.pdf • Beidleman, Carl R. I991, Interest Rate Swaps (Richard D. Irwin, INC.)