Download

1 / 8

80 likes | 270 Views

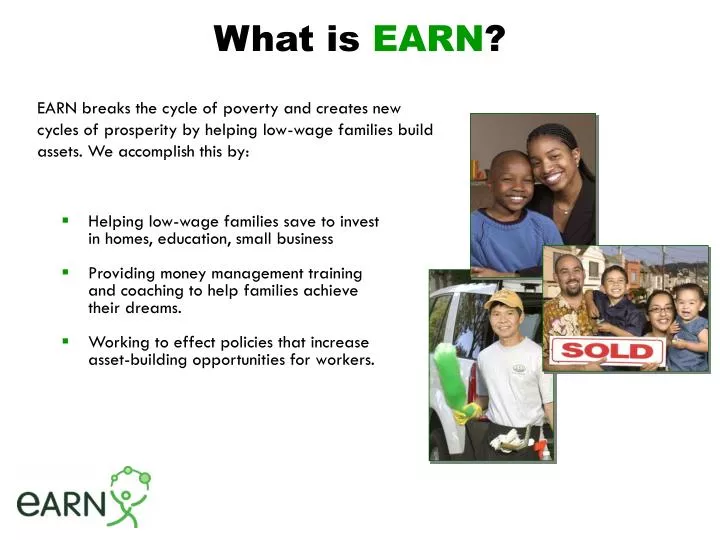

What is EARN ?. EARN breaks the cycle of poverty and creates new cycles of prosperity by helping low-wage families build assets. We accomplish this by:. Helping low-wage families save to invest in homes, education, small business

E N D

What is EARN? EARN breaks the cycle of poverty and creates new cycles of prosperity by helping low-wage families build assets. We accomplish this by: • Helping low-wage families save to invest in homes, education, small business • Providing money management training and coaching to help families achieve their dreams. • Working to effect policies that increase asset-building opportunities for workers.

2000+ Savers are Bay Area residents who dream of achieving financial security using IDAs; Average income is under $20k/year per household when they start 83% people of color, 65% women 25% Latino 64% are from households with children 17,000 newly banked San Franciscans through Bank on SF 300+ Alums with access to financial coaching and planning EARN Savers put aside 5% of their gross income EARN Savers have put aside over $2.2 million of their own hard earned dollars. 300+ Alums have invested over $2 million 67 Savers have purchased homes! Nearly all EARN homeowners have 30 year fixed rate mortgages EARN disallows predatory mortgage products Who EARN ServesHow They’re Doing

EARN Alumni Association • Additional Suite of Products and Services • Financial Coaching and Planning • Pilot in San Francisco • Micro-lending for credit card and medical debt • SAFE Accounts • 3:1 match for education • Very popular among Latino families • Networking + Additional Learning • Governed by Alumni Leadership Council • Determine annual focus • Produce annual event

Bank on San Francisco Learnings • This is working! • Over 17,000 newly banked San Franciscans • Keys to Success • Understanding Demand vs. Need • Getting granular and focusing on branches in key parts of San Francisco • Aligns incentives for branch managers • Circumvents community affairs staff • Remaining focused on a simple goal: get people banked • Linking to Financial Literacy has been very challenging • Banks not built to deliver training • Incentives and structure finally worked with CBOs

Lessons Learned - General Meet Latino Families where they really are • Distinguish between need and demand • Ex. Bank on SF focus group finding • Ex. Need for incentives for training • Segment the market • Ex. Don’t assume IDAs will work for all poor folks • Be thoughtful about how people actually obtain information to make key decisions • Word of mouth • Ethnic Media

Lessons Learned – SAFE Accounts • Important to Involve Entire Family in Orientation and Training • Children are often the lead translator for parents on educational, employment, legal, banking issues • Introduces children to importance of budgeting, saving, etc and creates dialogue between children and parents around saving and investing

Lessons Learned – IDAs/Homeownership • Identifying institutions that accept ITIN for mortgage loans • developing good referral relationships with loan officers is also important • Understanding how to improve, build or begin a good credit history. • Being clear about obstacles that Latino immigrants may face around homeownership (ITIN, stated income, credit history, HOA dues, etc.) Allows people time to identify resources to address issues.

Lessons Learned – IDAs/Homeownership – cont’d • Partnership with agencies like MEDA, Consumer Credit Counseling Services, and financial institutions is important. • Internal policies that protect low-income clients around risky mortgages • We believe this paternalism is justified • EARN’s Alumni Association is an important channel for staying in touch with Savers. • Continuing education and networking provides information on potential hazards around refinancing, changes in income of household, etc.