Download

1 / 24

260 likes | 640 Views

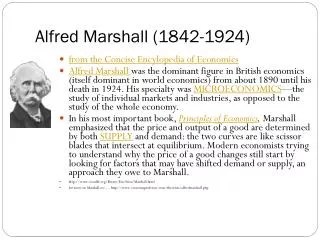

Alfred Marshall. Archer Jean Cathy . Who is Alfred Marshall??. The 1992 Nobel Prize winner in economics Founder of the Cambridge School of Economics * Author of the famous book called the Principles of Economics An opponent to women’s educational degree. Background Information.

E N D

Alfred Marshall Archer Jean Cathy

Who is Alfred Marshall?? • The 1992 Nobel Prize winner in economics • Founder of the Cambridge School of Economics • *Author of the famous book called the Principles of Economics • An opponent to women’s educational degree

Background Information • Born in a London suburb on 26 July 1842 • Died on 13 July 1924 (age 81) • Educated at the Merchant Taylor's School • showed particular interest for mathematics

Contributions to Modern Economics • Supply & demand curve • Elasticity of demand • Consumer surplus • Producer surplus

Definitions A curve that shows the equilibrium between supply and demand • Demand: how much (quantity) of a product or service is desired by buyers. • Supply: how much the market can offer • Price is a reflection of supply and demand

Shifts in Demand Demand Increases Demand Decreases

Shifts in Supply Supply Increases Supply Decreases

Equilibrium • Goods are being distributed efficiently because the amount being supplied is exactly the same as the amount being demanded

Disequilibrium Demand Supply • Price above the equilibrium level • Supply surplus Price Floor Price Ceiling • Price below the equilibrium level • Supply shortage

Definition • A formula that measures the change in quantity demanded due to a price change. Change in quantity demand Initial Price × Initial Demand Change in Price

Values • Smaller than 1 - Inelastic • Small change in price doesn’t create a big effect on the quantity demanded • Good is a necessary • There are no substitutes available • Doesn’t cost a lot (Salt) • Greater than 1 - Elastic • Small change in price cause a great change in the quantity demanded • The higher the price elasticity, the more sensitive consumers are to price changes • Good is not a necessary • There are substitutes available • Cost a lot (Pizza) • Equals to 1 - Unitary elastic • Small changes in price do not affect the total revenue

Definition • The difference between the maximum price that consumers are willing to pay and the price that the consumers are paying for a goods • Can be calculate from the supply and demand curve • Adjustable for price ceiling and price floor

Calculation of Consumer Surplus • Consumer surplus equals the area of the green triangle • ½(5 × 5) = 12.5

Calculations with Price floor and Price Ceiling • Consumer surplus equals the area of the green triangle • ½(4 × 4) = 8

Definition • The difference between the minimum price that producers are willing to sell and the price that the producers are selling for a goods • Can be calculate from the supply and demand curve • Adjustable for price ceiling and price floor

Calculation of Producer Surplus • Producer surplus equals the area of the pink triangle • ½(5 × 5) = 12.5

Calculations with Price floor and Price Ceiling • Producer surplus equals the sum of area of the pink triangle and the area of the rectangle • ½(4 × 4) + (4 × 2) = 16

Deadweight Loss Calculation • Deadweight loss is the loss of consumer and producer surplus from government intervention • Deadweight loss can be calculate in two ways: • (Sum of producer and consumer surplus without price floor and ceiling) – (Sum of producer and consumer surplus with price floor and ceiling) • (12.5 + 12.5) – (8 + 16) = 1 • Area of the gray triangle • ½(2 × 1) = 1