Download

1 / 12

120 likes | 138 Views

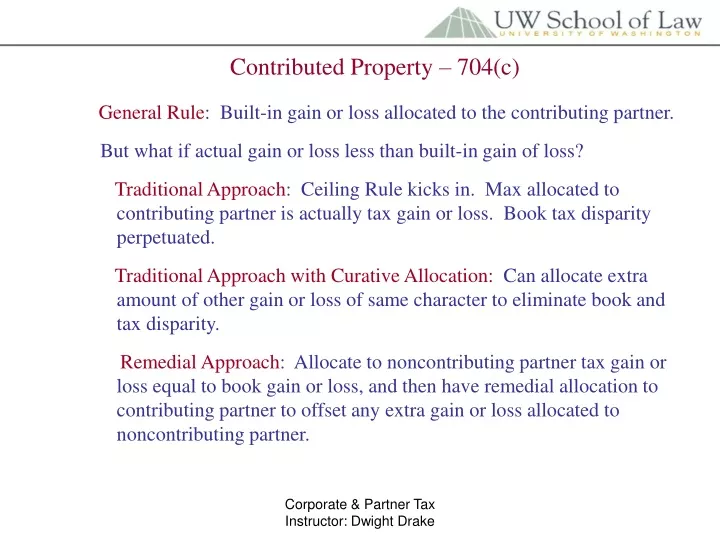

Contributed Property – 704(c). General Rule : Built-in gain or loss allocated to the contributing partner. But what if actual gain or loss less than built-in gain of loss?

E N D

Contributed Property – 704(c) General Rule: Built-in gain or loss allocated to the contributing partner. But what if actual gain or loss less than built-in gain of loss? Traditional Approach: Ceiling Rule kicks in. Max allocated to contributing partner is actually tax gain or loss. Book tax disparity perpetuated. Traditional Approach with Curative Allocation: Can allocate extra amount of other gain or loss of same character to eliminate book and tax disparity. Remedial Approach: Allocate to noncontributing partner tax gain or loss equal to book gain or loss, and then have remedial allocation to contributing partner to offset any extra gain or loss allocated to noncontributing partner. Corporate & Partner Tax Instructor: Dwight Drake

Problem 196 - 3 Buy land as joint tenants and contribute to partnership or buy through partnership? Both partners are dealers. If they buy and contribute, their dealer status will taint property as inventory for 5 yrs. If partnership buys, 724(b) not apply and property may qualify as investment property from day one. Buy land for 100k. Appreciate to 200k by year three. C contributes 100k cash for 1/3 interest, which used to improve property. Sell for 450k. How allocate gain 250 gain (450 – 200 basis). 100k allocated to A & B, built-in gain at C admission. Excess 150k allocated equally – 50k to each. Corporate & Partner Tax Instructor: Dwight Drake

Problem 196 - 3 Buy land as joint tenants and contribute to partnership or buy through partnership? Both partners are dealers. What result in (b) if use reverse 704(c) election and apply traditional allocation method? Restate book accounts on C’s admission to FMV – 200k. Thus, book gain on sale is 150k (450k – 300K) and tax gain of 250 (450 – 200). Book gain allocated equally to all three – 50k each. Excess tax gain of 100k allocated to A & B. Same net result as in (b). Corporate & Partner Tax Instructor: Dwight Drake

Problem 196 - 3 Buy land as joint tenants and contribute to partnership or buy through partnership? Both partners are dealers. (d) What result if no adjustment to capital accounts when C admitted and no special allocation of built-in gain? Here, 250 gain allocated equally to each partner – 83,333 to each. Capital accounts as follows: No allocation Allocation A 133,333 (50 + 83333) 150,000 (50 + 100) B 133,333 (50 + 83333) 150,000 (50 + 100) C 183,333 (100 + 83,333) 150,000 (100 + 50) Total 450,000 450,000 Result: Economic value shift of 33,333 from A & B to C. Could be treated as gift if relatives or compensation payment if employee. Corporate & Partner Tax Instructor: Dwight Drake

Problem 196 - 3 Corporate & Partner Tax Instructor: Dwight Drake