Download

1 / 10

110 likes | 264 Views

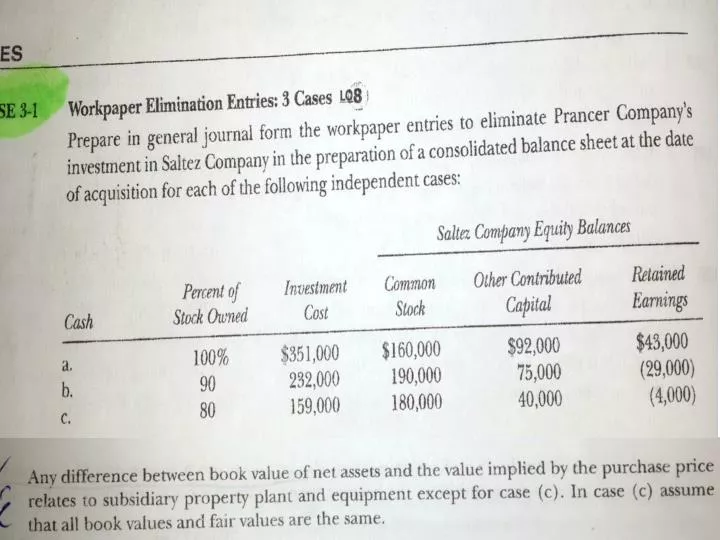

a. Common Stock 160,000 Other Contributed Capital 92,000 Retained Earnings 43,000 Difference between implied and book value 56,000 (351,000/100% - (160,000+92,000+43,000) Investment in Saltez 351,000 Property, Plant, and Equipment 56,000

E N D

a. Common Stock 160,000 Other Contributed Capital 92,000 Retained Earnings 43,000 Difference between implied and book value 56,000 (351,000/100% - (160,000+92,000+43,000) Investment in Saltez351,000 Property, Plant, and Equipment 56,000 Difference between implied and book value 56,000 b. Common Stock 190,000 Other Contributed Capital 75,000 Difference between implied and book value 21,778 (232,000/0.9-[190,000+75,000-29,000]) Retained Earnings 29,000 Investment in Saltez 232,000 Noncontrolling Interest 25,778 Property, Plant, and Equipment 21,778 Difference between implied and book value 21,778

c. Common Stock 180,000 Other Contributed Capital 40,000 Retained Earnings 4,000 Investment in Saltez 159,000 Gain on Purchase of Business – Prancer ** 13,800 NoncontrollingInterest (.2) ($198,750) + $3,450* 43,200 ** The ordinary gain to Prancer is $159,000 – (.80)($216,000) = $13,800 * Noncontrolling interest reflects the noncontrolling share of implied value (.20 x $198,750, or $39,750), plus the NCI portion of the bargain (.20 x $17,250) NOTE: We know this is a bargain acquisition in part c because the investment cost of $159,000 implies a total value of $198,750. Since this value is less than the book value of equity of $216,000 [$180,000+$40,000-$4,000], the difference is a bargain of $17,250. This bargain is allocated between the parent (this portion is reflected as a gain) and the NCI.

Part A Investment in Sun Company 192,000 Cash 192,000 Part BPRUNCE COMPANY AND SUBSIDIARY Consolidated Balance Sheet January 2, 2008 Assets Cash ($260,000 + $64,000 – $192,000) $132,000 Accounts Receivable 165,000 Inventory 171,000 Plant and Equipment (net) 484,000 Land ($63,000 + $32,000 + $28,333*) 123,333 Total Assets $1,075,333 Liabilities and Stockholders’ Equity Accounts Payable $151,000 Mortgage Payable 111,000 Total Liabilities 262,000 Noncontrolling Interest ($192,000/0.9 0.1) $21,333 Common Stock 400,000 Other Contributed Capital 208,000 Retained Earnings 184,000 Total Stockholders’ Equity 813,333 Total Liabilities and Stockholders’ Equity $1,075,333 * [$192,000/0.9 – ($70,000 + $20,000 + $95,000)] = $28,333

* Implied Value = Parent’s value $212,000 + NCI $37,412 = $249,412 Common Stock-Shipley 90,000 Other Contributed Capital-Shipley 90,000 Retained Earnings-Shipley 56,000 Land $249,412 - $236,000 13,412 Investment in Shipley Company 212,000 Noncontrolling Interest 37,412

Part B SHIPLEY COMPANY Balance Sheet December 31, 2007