Download

1 / 26

260 likes | 277 Views

Explore the ample opportunities for Chartered Accountants (CAs) in the co-operative sector, including statutory audit of co-op societies, tax audit, investment audit, concurrent audit, internal audit, VAT audit, audit committee participation, financial consultancy, appearing before income tax authorities, and decision making in debt settlement cases.

E N D

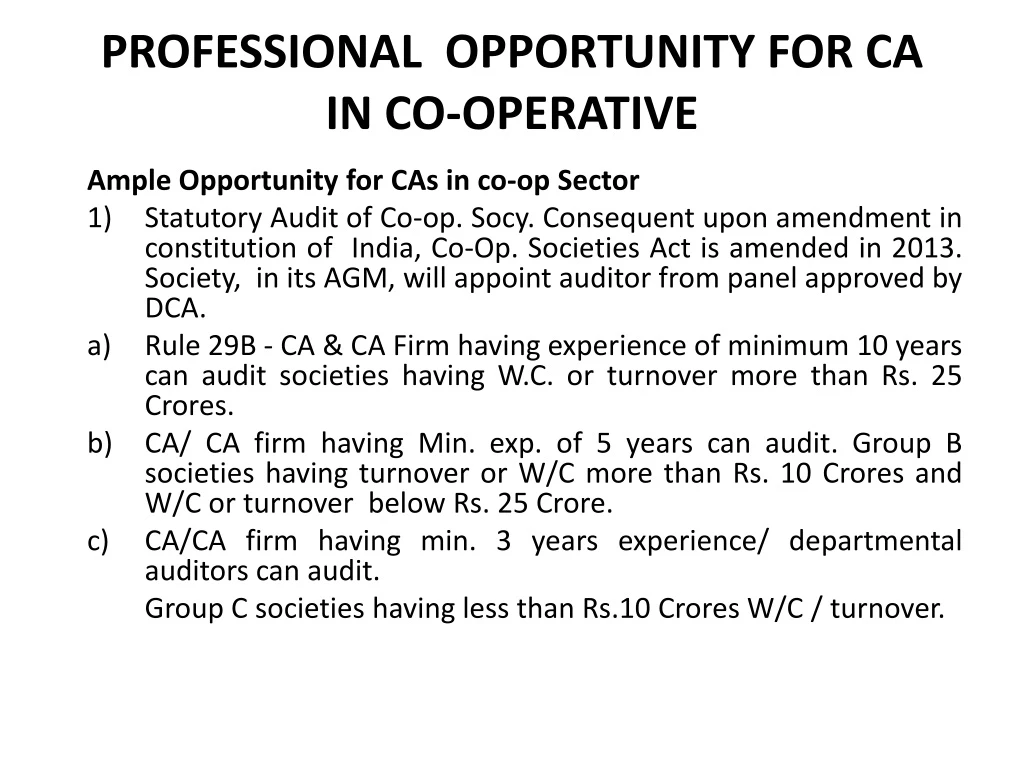

PROFESSIONAL OPPORTUNITY FOR CA IN CO-OPERATIVE Ample Opportunity for CAs in co-op Sector Statutory Audit of Co-op. Socy. Consequent upon amendment in constitution of India, Co-Op. Societies Act is amended in 2013. Society, in its AGM, will appoint auditor from panel approved by DCA. Rule 29B - CA & CA Firm having experience of minimum 10 years can audit societies having W.C. or turnover more than Rs. 25 Crores. CA/ CA firm having Min. exp. of 5 years can audit. Group B societies having turnover or W/C more than Rs. 10 Croresand W/C or turnover below Rs. 25 Crore. CA/CA firm having min. 3 years experience/ departmental auditors can audit. Group C societies having less than Rs.10 Crores W/C / turnover.

2) Tax Audit u/s 44AB Co-op. Socy. having turnover exceeding Rs. 1 Crore, is required to get tax audit u/s 44AB of IT Act to be done by Chartered Accountant. Previously, this limit was Rs. 40 Lakh. 3) Investment Audit of Ucb/dccb/scb Ucbsare required to invest their entire SLR in Govt. Securities. Investments are clasified in three categories i) Held till maturity ii) Available for sale iii) Held for trading

Investment in held till maturity is valuated at cost. Premium on purchase is amortized till the date maturity. Investment in remaining two categories are marked to market and any depreciation is recognized while appreciation is ignored. Auditor should scrutinize that Sale and Purchase transactions are done at rates beneficial to bank. Investment shown by bank tallies with the amount as shows by SGL/ CSGL Certificate.

4) Concurrent Audit of Ucbs • As per RBI guidelines, concurrent audit to all UCbs is now mandatory. • It is carried out quarterly basis • As per Ghosh Committee Report, RBI introduced concurrent audit for all Scheduled banks and Ucbs having deposit over Rs.50 Crores. But based on the recommendations of JPC which enquired in to stock market scam, all Ucbs are required to introduce system of concurrent audit. • Concurrent audit system is to be regarded as part of bank’s early warning system to ensure timely detection of irregularities and lapses. • CAs carring out internal/ concurrent audit shall not take assignment as statutory audit.

Internal Audit of big Co-operative Big Co-op. like Sugar factory, spinning mill and agro and industrial processing socy. get the internal audit conducted by CA. It helps in timely corrections of errors and lapses etc. • Audit of electronic and data processing system (System Audit). CA having CISA / DISA qualification can carry out system audit of banks. 7) VAT Audit Co-op. Socy. having turnover exceeding prescribed limit, is required to carry out VAT Audit by CA/CA firm

8) Audit Committee As per RBI Guidelines • To ensure and enhance the effectiveness of internal audit/ inspection as management tool. • Audit committee should be set up at board level consisting chairman and 3 or 4 director. • One or more of such directors should be CA or person experience in finance, accountancy and audit system. 9) Co-opted directors on BOD (Sec. 28A(4A) • Board may co-op. two persons having experience in field of management, banking, finance or specialization in any other field relating to objects of socy. • Generally, CAs are co-opted as expert director on bank.

10) Financial Consultancy • In big Co-operative like Sugar, Milk Federation, in financial decision making for erecting new plant co-generation, distillery, cattle feed factory, chilling unit, paper plant, only CA can give good type of advice to co-operative. • CA can effectively prepare cash flow, fund flow statements. He can calculate various financial ratios like current ratio, debt equity ratio, interest coverage ratio, ROI etc. and can advise co-operative in effective way. • CA can work out Break even analysis (BEP) • He can suggest whether it is profitable to buy or let by making financial analysis.

11) Appearance before Income Tax authority. • CA can consult his clients in Income Tax matters and appears before I.T. Authorities on behalf of clients. 12) Deciding the amount payable by borrower under OTS - case referred to CA either by bank or by borrower.

Session - II CO-OPERATIVE GOVERANANCE • Co-operative Governance means how co-op. socy. is managed and controlled. • The best way of managing and functioning of socy. • Co-op. Governance means observance of Act & Rule & bilaws in Managing the socy. • Co-op. governance is the way the society is organized and managed to ensure that financial stake holders (share holders, creditors & bankers) receive their fair share of society’s earning and assets. • Co-operative governance is concerned with the ways the co-op. society’s are governed.

There are verious participants in co-op society. a) Share Holders, b) Creditors, c) Bankers d) BOD, E) Employees, f) Customers. • Keeping view interests of verious stake holders, co-op. governance is concerned with effective management of relationship between verious stake holders. • Co-op. governance is acceptance by management of rights of share holders as true owners of co-op. society and their own role as trustee on behalf of share holders.

Co-op. governance is i) Application of best management practices. ii) Compliance with law in true letter and spirit. iii) Adherance to ethical standards for effective management. iv) Distribution of wealth and discharge of social responsibility for sustainable growth of stake holders. Final Authority in Co-op.Socy. (Sec. 26) • Final authority of Socy. shall vests in members. Annual General Meeting (Sec. 27) • Every Socy. shall convey AGM once in year before 25th Sept. Board may call this meeting (Rule 14 AJ).

AGM will consider following • Annual report presented by Board. • Latest available audit report and report of Board thereon. (RR) • Consideration of enquiry report. • Disposal of net profits. • Approval of annual budget. • Amendment of bilaws. • Perusal of list of employees who are relatives of BOD etc. appointment of auditors. Sec - 27 A - Participation of members in the management (w.e.f. 11/02/2013) • He must attend 3 out of 5 AGM • Utilise minimum services as specified in bilaws.

If member fails to utilise minimum service or fails to attend meeting as above, he will lose his right to vote for period of three years. • Sec. 27 B - Returns to be filed with Registrar • Board of every co-op. socy. shall file following returns within 6 months of close of FY. • Annual return of activities. • Audited statement of account. • Plan for disposal of surplus. • List of amendments to byelaws. • Declaration regarding holding AGM and conduct of election when due. • Misappropriation or embezzlement of funds and action taken against persons responsible.

28 A (1) Management of co-op. socy. west in Board. • 28 A (2) Number o BORD minimum 9, Maximum 21 Reservation • 1 Seat for SC & ST • 2 seats for women • Sec. 28A (4A) 2 co-opted directors having experience in banking, finance, management. This is in addition to max. number of BOD. • 3 Functional directors. • Functional and expert directors shalln't form part of Quorum. • Sec. 29A (4B) - State Govt. may nominate one director on BOD of Socy. other than PAC. • Sec. 28B - Board to arrange for election.

Sec.28C Powers and Functions of BOD • to admit members. • to dispose of application for allotment of shares. • to mobilize resorces and invest funds. • sanction of loans to members. • to acquire/ dispose of movabe and immovable property required for achieving objectives of socy. • to set up specific goals to be achieved towards organisational objectives. • to approve expenditure necessary for business and etc.

29C - Disqualification of BOD. • If he is in default to that socy. or any other co-op. socy. as borrower. • Interested directly or indirectly in contract made with socy. or in sale or purchase made by socy. • Carries on business carried on by socy. • Employed as legal practitioner on behalf of such socy. or accepts employment as legal practitioner against such socy. • If he is paid employee (other than CEO) of such socy. or of its financing bank. • He is a near relation of paid employee of such socy. • He is disqualified to be member of the socy. or to vote as such member. • He was member of Board which failed to make arrangement for election within time limit specified in Sec. 39A.

He is a representative of co-op. socy. which is in default to financing bank. • He absents three consecutive meetings of Board without leave of absence. Sec. 29 (c) (3) If Board of Co-op. Socy. fails. • To assist CEC for conducting election or • To call AGM u/s 27 or special G. Meeting u/s 28 or • To present the audited accounts and annual report to AGM. • Every member of Board shall be disqualified for being elected or appointed or continued as member of Board for period of 5 years from date of order of disqualification. • Rule 14 AK - Board may meet as and when required to transact the business. • But interval between two consecutive meeting shalln't exceed 3 months.

Sec. 30 - Supersession or Suspension of Board • No board of co-op. socy. shall be superseded or kept under suspension for period exceeding 6 months. • In case of bank, this period is one year. Grounds for superstation / suspension (Sec. 30 (2) If in the opinion of Registrar, board • Persistently makes default or is negligent in performance of the duties imosed on it by Act, Rules or byelaws or • Commits any act, which is prejudicial to the interest of socy. / members. • When there is stalementin constitution or functioning of board. • Has serious financial irregularities or Frauds which have been detected. • Fails to provide books and record, information and assistance to election commission. • He supersedes or keep under suspension the board of Directors

BOD shall not be superseded or kept under suspension if there is no Govt. shareholding or loan or any financial assistance or any guarantee by the Govt. • In case of bank, bod shall be superseded / kept under suspension only after consultation with RBI/ Nabard. • 39A (15) Board of every co-op. socy. shall inform the EC about expiry of its term of office at least six months before date of expiry of their term. • Sec. 30 B - Power of State Govt. to give directions in public interest. • For safeguarding interest of members, or in public interest and for securing proper implementation of co-op. and other development programs, S. Govt. may issue directions to the socy.

Sec. 57 Disposal of Net profit • 25% to Reserve Fund. • 2% to Co-operative Education fund. • Unless it contributes to co-op. Edu. Fund, it cannot pay dividend to its members. • Sec. 57A - Co-op. Edu. Fund shall • Be Utilised for the purpose of promotion of co-op. movement in the state and for providing education to the members, directors and training to employees of co-op. society.

Investment of fund (Sec. 58) • Co-op. socy. may invest its funds. • In Govt. saving bank. • Trustee Securities. • Shares/ securities of any other societies. • With any co-op. bank. • Any sch. bank or FI regulated by RBI and approved by General body of socy.

Restriction on Borrowings (Sec. 59) • Co-op. Socy. shall receive deposit and loans only to such extent as may be specified in byelaws. • Admission of members before General Meeting of Socy.(Rule 8) • Co-op socy. shall not admit members within 30 days prior to date of AGM. • Rule 9 - CEC may Formulate guidelines for preparation of electoral rolls and for conducts of elections of all co-operatives in state.

Rule 14 - AF CEO shall report casual vacancy in BOD to CEC within 7 days of its occurance. • Rule 26 Soc. shall not enter into transaction with non members unless byelaws permit or previous sanction of Registrar has been obtained by socy.

DRAFTING SKILL RELATED TO CO-OPERATIVE • Co-operative play Pioneer role in rural development. • For the above purpose, co-op. get huge funds from Central Govt., State Govt. NCDC, NDDB, NABARD etc, • These funds are in the form of Govt. Capital, loan, subsidy and guarantees. • In order to avail the above facilities, co-op. has to submit proposals to various authorities.

Drafting various proposals for loan, capital subsidy and guarantee require special skill. • Financial position of socy. is required to stated in nutshell and within half page. • Necessary schedules referring items in B/S to be attached. • Fund flow and cash flow statement are required to be prepared. • Amount of fixed and variable expenses to be given separately. • BEP is required to be given. • It is to be shown how co-operative with repay the loan and capital on due dates.

For purpose of redemption of capital on due date, capital redemption fund will be created every year. • This fund will be separately invested so that co-op. can draw amount and pay Govt. capital on due date. • Proposal will also show whether infrastructure facilities are available. • Proposal will also give plan for marketing the produce. • All above, require excellent drafting skill which C.A. posseses.