Download

1 / 29

290 likes | 303 Views

Learn about price elasticity in economics, factors affecting it, substitutes, necessities vs. luxuries, short run vs. long run elasticity, and competitive dynamics. Dive into calculations and formulas for price elasticity of demand and supply.

E N D

Elasticity Macroeconomics What is Marketing? Principles of Marketing

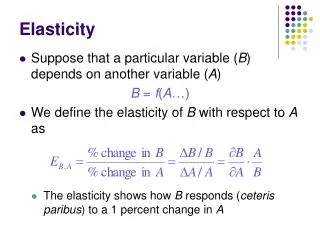

Elasticity How responsive or sensitive one thing is to a change in another thing

Substitutes Price elasticity of demand is fundamentally about substitutes. If it’s easy to find a substitute product when the price of a product increases, the demand will be more elastic. If there are few or no alternatives, demand will be less elastic.

Necessities vs. Luxuries A necessity is something you absolutely must have, almost regardless of the price. A luxury is something that would be nice to have, but it’s not absolutely necessary. In general, the greater the necessity of the product, the less elastic, or more inelastic, the demand will be, because substitutes are limited. The more luxurious the product is, the more elastic demand will be.

Share of the Consumer’s Budget If a product takes up a large share of a consumer’s budget, even a small percentage increase in price may make it prohibitively expensive to many buyers. The larger the share of an item in one’s budget, the more price elastic demand is likely to be.

Short Run Versus Long Run Price elasticity of demand is usually lower in the short run, before consumers have much time to react, than in the long run, when they have greater opportunity to find substitute goods. Thus, demand is more price elastic in the long run than in the short run

Competitive Dynamics Goods that can only be produced by one supplier generally have inelastic demand, while products that exist in a competitive marketplace have elastic demand. This is because a competitive marketplace offers more options for the buyer.

Practice Question: How elastic is the demand for: • Blood pressure medicine • Diamond engagement rings

Calculating Growth or Change Percentage change=

Calculating Price Elasticity of Demand The price elasticity of demand is defined as the percentage change in quantity demanded divided by the percentage change in price: • Price elasticity of demand= There are two general methods for calculating elasticities: • The point approach uses the initial price and initial quantity to measure percent change • The more accurate approach is the midpoint approach, which uses the average price and average quantity over the price and quantity change

Price Elasticity of Demand The price elasticity of demand is calculated as the percentage change in quantity divided by the percentage change in price

Price Elasticity of Supply The price elasticity of supply is calculated as the percentage change in quantity divided by the percentage change in price.

Elasticity Is Not Slope It’s a common mistake to confuse the slope of either the supply or demand curve with its elasticity. The slope is the rate of change in units along the curve, or the rise/run (change in y over the change in x)

Income Elasticity of Demand For most products, most of the time, the income elasticity of demand is positive: that is, a rise in income will cause an increase in the quantity demanded. This pattern is common enough that these goods are referred to as normal goods. However, for a few goods, an increase in income means that one might purchase less of the good; for example, those with a higher income might buy fewer hamburgers, because they are buying more steak instead. When the income elasticity of demand is negative, the good is called an inferior good

Cross-Price Elasticity of Demand A change in the price of one good can shift the quantity demanded for another good. • For complements, like bread and peanut butter, then a drop in the price of one good will lead to an increase in the quantity demanded of the other good • if the two goods are substitutes, like plane tickets and train tickets, then a drop in the price of one good will cause people to substitute toward that good, and to reduce consumption of the other good

Wage Elasticity of Labor Supply In the labor market, for example, the wage elasticity of labor supply—that is, the percentage change in hours worked divided by the percentage change in wages—will determine the shape of the labor supply curve • In general wage elasticity of labor supply depends on age

Elasticity of Savings In markets for financial capital, the elasticity of savings—that is, the percentage change in the quantity of savings divided by the percentage change in interest rates—will describe the shape of the supply curve for financial capital • In the short run, the elasticity of savings with respect to the interest rate appears fairly inelastic

Total Revenue The key consideration when thinking about maximizing revenue is the price elasticity of demand. Total revenue is the price of an item multiplied by the number of units sold: TR = P x Qd

Shifts in Supply The shift in supply can result either in a new equilibrium with a much higher price and an only slightly smaller quantity, as in (a), or in a new equilibrium with only a small increase in price and a relatively larger reduction in quantity, as in (b). Often a represents the short term impact while b represents the longer term impact.

Quick Review • What is elasticity? • What are the price elasticity of demand and price elasticity of supply? How are they calculated using the midpoint method? • What are other elasticities using common economic variables? How are they calculated? • How does a firm’s price elasticity of demand affect total revenue?