Download

1 / 19

620 likes | 2.04k Views

Portfolio Selection. Chapter 8 Charles P. Jones, Investments: Analysis and Management, Tenth Edition, John Wiley & Sons Prepared by Elshahat, Ahmed, Florida International University. Building a Portfolio Using Markowitz Principles.

E N D

Portfolio Selection Chapter 8 Charles P. Jones, Investments: Analysis and Management, Tenth Edition, John Wiley & Sons Prepared by Elshahat, Ahmed, Florida International University Elshahat, Ahmed

Building a Portfolio Using Markowitz Principles • Identify optimal risk-return combinations available from the set of risky assets being considered. • Tool: Markowitz efficient frontier analysis. • Input: expected returns, variances, & covariances • Select the optimal portfolio from among those in the efficient set. • Criteria: investor's preferences Elshahat, Ahmed

1 – Identifying Optimal Risk-Return Combinations • Assumptions: • A single investment period • Liquidity of positions (no transaction cost). • Investor preferences is based only on portfolio's expected return and risk. • Steps: • The Attainable Set of Portfolios • Efficient Portfolios • The Efficient Set Elshahat, Ahmed

The Attainable Set of Portfolios Determine the risk-return opportunities available. A large number of possible portfolios exist. • The attainable (opportunity) set is the entire set of all portfolios that could be found from a group of n securities. • Risk-averse investors should be interested only in those portfolios with the lowest possible risk for any given level of return. Elshahat, Ahmed

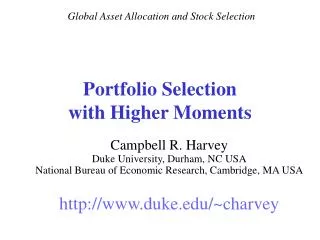

Efficient Portfolios • Portfolio that has the smallest portfolio risk for a given level of expected return or the largest expected return for a given level of risk • Given the minimum-variance portfolios, we can plot the minimum-variance frontier as shown in this Figure. • X dominates Y. Elshahat, Ahmed

The Efficient Set (Frontier)(AB) • The efficient set is determined by the principle of dominance — portfolio X dominates portfolio Y if it has the same level of risk but a larger expected return, or the same expected return but a lower risk. • The solution to the Markowitz model revolves around the portfolio weights Elshahat, Ahmed

Understanding the Markowitz Solution • Think of efficient portfolios as being derived in the following manner: • Inputs: Determine the Required E(R), 10%. • Create all portfolios that can yield 10%. • Choose the one with the lowest risk. • Determine anther Required E(R), 11%. • Continue the process. Elshahat, Ahmed

2 – Selecting an Optimal Portfolio of Risky Assets • Markowitz model does not specify one optimum portfolio. Rather, it generates the efficient set of portfolios, all of which, by definition, are optimal portfolios. • Indifference Curves:describe investor preferences for risk and return. • Each indifference curve represents the combinations of risk and expected return that are equally desirable to a particular investor. Elshahat, Ahmed

Indifference Curves Properties • Indifference curves cannot intersect • Investors have an infinite number of indifference curves • The curves for all risk-averse investors will be upward-sloping, but the shapes of the curves can vary depending on risk preferences. • Higher indifference curves are more desirable than lower indifference curves. • The greater the slope of the indifference curves, the greater the risk aversion of investors. • The farther an indifference curve is from the horizontal axis, the greater the utility. Elshahat, Ahmed

Selecting the Optimal Portfolio • The optimal portfolio for a risk-averse investor is the one on the efficient frontier that is tangent to an investor's indifference curve that is highest in return-risk space. Elshahat, Ahmed

SOME IMPORTANT CONCLUSIONS ABOUT THE MARKOWITZ MODEL • Markowitz portfolio theory is referred to as a two-parameter model. • The Markowitz analysis generates an entire set of efficient portfolios, all are equally good. • The Markowitz model does not address the issue of investors using borrowed money • Different investors will estimate the inputs to the Markowitz model differently. • The Markowitz model remains cumbersome to work with because of the large variance-covariance matrix Elshahat, Ahmed

Alternative Methods of Obtaining the Efficient Frontier – SIM & MIM • THE SINGLE-INDEX MODEL (SIM):relates returns on each security to the returns on a common index. Elshahat, Ahmed

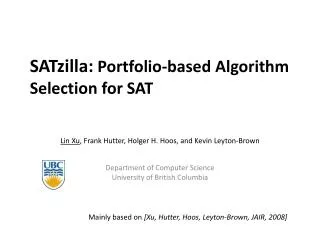

THE SINGLE-INDEX MODEL • The single-index model divides a security's return into two components: • Micro event: A unique part, represented by ai, affecting an individual company but not all companies in general. • Macro event: A market-related part represented by βiRM, broad-based and affects all (or most) firms. • Error term Elshahat, Ahmed

Critical Assumption of the SIM • Securities are related only in their common response to the return on the market (the residual errors for security i are uncorrelated with those of security j). • It implies that stocks covary together only because of their common relationship to the market index. • There are no influences on stocks beyond the market, such as industry effects. • Thus, covariance depends only on market risk. Elshahat, Ahmed

Splitting Risk into Two Parts Elshahat, Ahmed

The Asset Allocation Decision • The allocation of portfolio assets to broad asset markets. • How much of the portfolio's funds are to be invested in stocks, how much in bonds, money market assets, and so forth. • Some Major Asset Classes: • International Investing • Bonds • Treasury Inflation-Indexed Securities. • Real Estate Elshahat, Ahmed

COMBINING ASSET CLASSES Elshahat, Ahmed

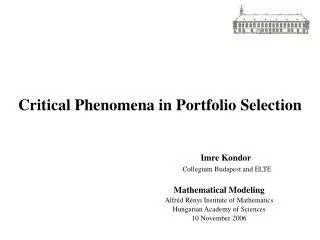

The Impact of Diversification on Risk Elshahat, Ahmed

How Many Securities Are Enough to Diversify Properly? • As few as 20 stocks could be adequate Elshahat, Ahmed