Download

1 / 35

350 likes | 424 Views

Explore the basics of demand theory, budget constraints, and consumer choice maximizing utility while considering prices and income levels. Learn about essential goods, demand functions, and elasticity of demand.

E N D

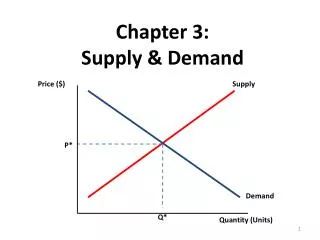

The Budget Constraint • Attainable consumption bundles are bundles that the consumer can afford to buy. • Attainable consumption bundles satisfy the following inequality known as the budget constraint. p1x1+p2x2 ≤ M

Opportunity Cost, Real Income and Relative Prices • Rewriting the budget constraint by solving for X2 gives: x2 = M/p2 – (p1/p2)x1 Where:M/p2 is real income P1/P2is the relative price The relative price shows that the opportunity cost of good 1 is P1/P2units of good 2. P1/P2 is the absolute value of the slope of the budget line.

Endowments Rather Than Money • Sometimes an endowment of goods is assumed rather than cash. • Sally owns apples x10 and eggs x20. • Her budget constraint is: p1x1+p2x2 ≤ p1x10 + p2x20 • Solving for x2: x2 = (p1x10 + p2x20)/p2 – (p1/p2)/x1 As before, the budget constraint depends upon relative prices and real income (the endowment).

The Choice Problem • The non-satiation assumption implies that utility maximizing consumption lies on the budget line. • The consumer choice problem is: maximize U(x1, x2) by choice of x1 & x2, subject to constraint p1x1+p2x2 = M

The Choice Problem • In principle we refer to the solution (x1*,x2*) as endogenous variables, as these variables are determined within the model. • The actual values of X1*and X2* depend on the exogenous variables in the model, (p1, p2and M) and on the specific form of the utility function.

Figure 3.3 Non-satiation and the utility-maximizing consumption bundle

Demand Functions X1* = D1(p1, p2, M) X2* = D2(p1, p2, M) • These demand function equations simply say that the choice of X1* and X2*depend upon the prices of all items in the consumption bundle and the budget devoted to that bundle.

Anna’s optimal choice when both goods are perfect substitutes

Graphic Analysis of Utility Maximization • Assume indifference curves are smooth and strictly convex. • Interior solutions are where quantities of both goods are positive. • Corner solution is one where the quantity of one good is positive and the quantity of the other is zero.

Interior Solution • An interior solution is described by: • P1x1*+P2x2*Ξ M, the optimal bundle lies on the budget line. • MRS(X1*, X2*) Ξ P1/P2, the slope of the indifference curve equals the slope of the budget line at the optimal bundle.

Corner Solutions • A corner solution graphically lies not in the interior between the two axis, but at a corner where the budget line intersects one of the two axes. • For example, if at the point where the budget line intersects the X2 axis, the budget line is steeper than the indifference curve, only good 2 will be purchased.

Excise Tax Versus Lump-Sum Tax • Given a choice between a lump sum tax and an excise tax that raises the same revenue, the consumer will choose the lump sum tax (see Figure 3.8).

Figure 3.13 The consumption response to a change in the price of another good

Consumption Response to a Change in Price • The price-consumption path connects the utility maximizing bundles that arise from a change in the price of p1 or p2. • Note that when p1changes, M and p2are assumed to be constant. Likewise if p2were to change, M and p1are assumed to be constant.

Figure 3.14 The price-consumption path and the demand function

Elasticity • Elasticity is a measure of responsiveness of the quantity demanded for one good to a change in one of the exogenous variables: price or income.

Figure 3.15 The need for a unit-free measure of responsiveness

Own-Price Elasticity • Own-price elasticity (Ell) relates to how much the one good changes when its own price changes. • Ell= % change in x1/ % change in P1 OR

Elasticity • If we allow changes in the exogenous variables to approach zero we obtain marginal or point elasticity.

Elasticity • Arc elasticity measures discrete changes in x1 when there is a discrete change in p1,p2 or M). • By allowing changes in the exogenous variables to approach zero gives marginal or point elasticity. • Price elasticity of demand for a good is the elasticity of quantity consumed per capita with respect to the price of the good.

Income Elasticity • The income elasticity of demand is the elasticity of quantity consumed per capita with respect to income per capita.

Cross Price Elasticity • The cross price elasticity of demand for good 1 with respect to the price of good 2, is the elasticity of per capita consumption of good 1 with respect to p2.