Download

1 / 18

180 likes | 333 Views

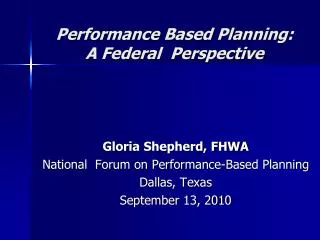

National Association for State Community Services Programs 2011 Mid-Winter Training Conference. The Federal Perspective. FINANCIAL SYSTEM. Cash Management System. Procurement System. Budget System. Human Resources/ Payroll System. CORE FINANCIAL Cost Accounting Reporting.

E N D

National Association for State Community Services Programs 2011 Mid-Winter Training Conference The Federal Perspective

FINANCIAL SYSTEM Cash Management System Procurement System Budget System Human Resources/ Payroll System • CORE FINANCIAL • Cost Accounting • Reporting Property Management System Travel System Inventory Management System Contract Management System

Budget System • Subgrantees Not Submitting an Annual Budget

Cash Management System • Subgrantees given advances that exceeded the cash needs of the program • Advances not put in interest bearing accounts • Subgrantees not provided cash advances

Procurement System • Competitive process not used for procurement of contractors • Cost analysis not done in the selection of the contractor • Bid/Proposal specifications inadequate or not written at all • Cumbersome procurement procedures • Incomplete documentation of procurement activities • Lease/purchase analysis for equipment not performed

Human Resources/Payroll System • Payroll information did not support that employees were providing services to the program

Inventory Management System • Inventory records do not track the point of purchase to the installation of materials on the house

Grant/Contract Management System • Contractors billed for labor charges that had not been performed and materials that had not been installed • Inadequate oversight of contractors • Inadequate documentation for contractor billing • Subgrantees not monitored to ensure compliance with financial regulations • Evaluation of contractors not documented

Property Management System Subgrantees not performing a physical reconciliation of equipment Subgrantees not requesting permission to purchase equipment prior to purchase Equipment records do not include required information

FOR PROFIT WEATHERIZATION SERVICESAgency Self Assessment • Does the organization have the skills needed to run a for profit project? • Has the organization identified what help they will need and where to get the help? • Do the staff have the time required to learn the things that they need to know? • Does the organization have the money to hire the staff and/or consultants needed?

FOR PROFIT WEATHERIZATION SERVICESAgency Self Assessment (cont.) • Is the organization interested in the proposed for profit project? • Is the organization committed to the success of the for profit project? • Is the organization willing to devote the time needed to develop a successful for profit project? • Will the project fill an unmet need in the community or can you do it better that the current businesses providing the goods/services?

FOR PROFIT WEATHERIZATION SERVICESAgency Self Assessment (cont.) • Is there sufficient customer demand for the goods/services offered by the project? • Will the organization be able to compete competitively? • Does the Board of Directors and Administration understand financial statements such as cash flow, profit and loss, and balance sheets? • Has the organization developed a comprehensive business plan?

Business PlanningThe steps involved in developing a business plan include: STEP 1: Determine what is wanted from the venture, recognizing the time and investment involved. STEP 2: Survey the target-population you plan to serve to determine if the necessary volume required to produce the desired income is attainable

Business Planning The steps involved in developing a business plan include:(cont) STEP 3: Prepare a statement of assets to be used in the venture STEP 4: Analyze estimated expenses in terms of fixed or variable nature and determine the break point

Business Planning The steps involved in developing a business plan include:(cont) STEP 5: Review the risks to which the organization is subject and methods with which these risks are going to be minimized STEP 6: Establish an adequate system of accounting records

Federal Regulations 10 CFR 600.134 - Equipment “The recipient shall not use equipment acquired with Federal funds to provide services to non-Federal outside organizations for a fee that is less than private companies charge for equivalent services, unless specifically authorized by Federal statute, for as long as the Federal Government retains an interest in the equipment.” “User charges shall be treated as program income.”

Federal Regulations (cont.) 10 CFR 600.135 – Supplies and other expendible property “The recipient shall not use equipment acquired with Federal funds to provide services to non-Federal outside organizations for a fee that is less than private companies charge for equivalent services, unless specifically authorized by Federal statute, for as long as the Federal Government retains an interest in the supplies.” “User charges shall be treated as program income.”