Download

1 / 4

40 likes | 44 Views

Learn how to prepare a post-closing trial balance to ensure the equality of debits and credits in the general ledger and to prepare for the next fiscal period. Understand the accounting cycle for a merchandising business organized as a corporation, including source document verification, transaction recording, ledger posting, subsidiary ledger preparation, worksheet creation, financial statement preparation, and adjusting/closing entries.

E N D

LESSON 16-3 Preparing a Post-Closing Trial Balance

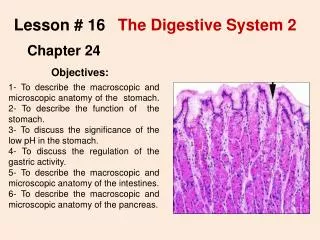

3 2 4 5 7 POST-CLOSING TRIAL BALANCE page 496 1. Heading 1 2. Accounts that have balances 3. Debit balances 4. Credit balances 5. Word Totals 6. Totals 7. Double lines A post-closing trial balance is prepared to prove the equality of debits & credits in the general ledger & to prepare the general ledger for the next fiscal period 6 LESSON 16-3

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 497 1. Source documents are checked, and transactions are analyzed. 1 2 2. Transactions are recorded in journals. 3. Journal entries are posted to the accounts payable ledger, the accounts receivable ledger, and the general ledger. 3 4 5 4. Schedules of accounts payable and account receivable are prepared from the subsidiary ledgers. 5. A work sheet is prepared from the general ledger. (continued on next slide) LESSON 16-3

6. Financial statements are prepared. ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 497 7. Adjusting and closing entries are journalized from the work sheet. 9 8. Adjusting and closing entries are posted to the general ledger. 9. A post-closing trial balance of the general ledger is prepared. 8 7 6 (continued from previous slide) LESSON 16-3