Download

1 / 28

280 likes | 299 Views

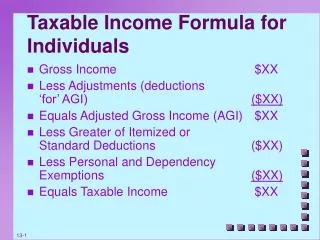

This presentation by Louisiana Oil and Gas Association covers rules, valuation approaches, market data, and proposals for oil and gas property taxes.

E N D

Presentation to the Louisiana Tax Commission2011 Rules and Regulations Chapter 9 – Oil and Gas PropertiesbyLouisiana Oil and Gas Association andLouisiana Mid-Continent Oil and Gas AssociationJune 22, 2010 Information included in this presentation is the same as submitted in writing June 4, 2010 to the Louisiana Tax Commission. This presentation is prepared only to facilitate the verbal presentation on June 22, 2010 as indicated in the LTC Docket Number RR-2011, Notice of Hearing.

Exhibit 1 Valuation of Louisiana Oil and Gas Wells for Property Taxes Legal Conclusions of Taxable Property Valuation Approach? Cost Taxable Cost (studies, company books) Inflation Factor to Current Cost Additional Adjustments (if appropriate) Reality Check (% of discounted cash flow value,sale of same property, other) Replacement Cost New Less Physical Depreciation (age from serial no.) Taxable Market Value Preliminary Market Value Review Status and Production Data for Shut-In and Low Producing Wells (LDNR, operators, other) Market Adjustments (obsolescence) Review Other Market Data (environmental, operators, buyers, sellers, other) RCNLD Less Some Market Adjustment Less Shut-In and Low Production Credits Red above indicates the major ongoing differences between industry and the LAA. The box indicates where assessors generally stop in their appraisal of wells.

Oil Well Exhibit 2

Exhibit 3 Louisiana Oil Producing Wells Profile Daily # Of % Of Annual % Of ProductionWellsTotalProduction * Total 0 – 1 barrel 15,648 59.5% 1.870 2.4% > 1 – 10 barrels 7,143 27.2% 9.792 12.4% > 10 barrels 3,504 13.3% 67.322 85.2% Total Producing 26,295 78.984 Source: LDNR SONRIS database * millions of barrels

Exhibit 3 Louisiana Gas Producing Wells Profile Daily # Of % Of Annual % Of ProductionWellsTotalProduction * Total 0 – 10 mcf 11,653 49.0% 9.6 .5% > 10 – 100 mcf 5,408 22.8% 94.0 4.8% > 100 mcf 6,698 28.2% 1,863.0 94.7% Total Producing 23,759 1,966.6 Source: LDNR SONRIS database* billion cubic feet

Valuation of Oil & Gas Propertiesfor Investments and Acquisitions/Sales How do owners, investors, buyers, and sellers value specific oil and gas properties? Discounted Cash Flow (sales of other properties are benchmarks) What is DCF? “Future cash flows multiplied by discount factors to obtain present values.” Source: Forbes Financial Glossary at www.forbes.com

Exhibit 5 Example of Gas Well Production Decline Curve

Exhibit 5 Example of Discounted Cash Flow Valuation ($ thousands) Net Present Value Discount Before Tax RateCash Flow 16% $473 Gas Gas Before 16% Volume x Price = Total - Operating - Production = Tax Cash DCF YearMMSCF$mcfRevenueCostTaxesFlowFactor 2010 59.61 $4.23 $ 252.17 $ 59.3 $ 34.04 $158.87 .862 2011 46.91 4.91 230.31 60.4 31.09 138.77 .743 2012 37.39 5.66 211.62 61.7 28.57 121.40 .641 2013 30.37 5.96 181.01 63.8 24.44 92.82 .552 2014 25.07 6.11 153.16 67.0 20.68 65.51 .476 2015 20.98 6.47 135.72 70.4 18.32 47.03 .410 2016 17.76 6.72 119.36 73.9 16.11 29.33 .354 2017 15.20 6.86 104.26 77.7 14.07 12.52 .305 2018 4.58 7.05 32.32 26.6 4.36 1.40 .263 Totals 257.87 $1,419.93 $560.8 $191.68 $667.65

What is relevant to the valuation of oil and gas wells and related property inthe market? Irrelevant: Past Capital Cost Relevant: Anticipated Future Income and Liabilities (Income Approach) We recognize the LTC Oil & Gas Rules & Regulations represent a Cost Approach mass appraisal system. Our proposals try to stay within this system, but use Income Approach concepts.

2010 Survey of Authorizations for Expenditureof Louisiana Oil and Gas Properties Exhibit 6 Wells Wells TangibleCompletion Minimum 1% 0% Simple Average 20% 26% Weighted Average 19% 23% Median 18% 25% Maximum 58% 56% # of Wells Region 1 41 23% 29% Region 2 126 19% 25% 2005 27 19% 26% 2006 27 21% 22% 2007 34 17% 26% 2008 47 21% 26% 2009 2220%27% Totals 157 20% 26%

LOGA/LMOGA Proposal for Cost • Taxpayers should report taxable historical cost for wells, surface equipment, and related property. • If the LTC chooses to continue using the American Petroleum Institute’s Joint Association Survey on Drilling Cost as the source of cost for wells, no more than 25% should be applied to total API cost by depth bracket to estimate taxable cost. • If the LTC chooses to continue using a Surface Equipment schedule, we proposal no change from 2010.

LSU Center for Energy Studies Report Exhibit 6, Page 47 First year decline for GAS wells changed from 95% in 1977 to 62% in 2001. First year decline for OIL wells changed from 89% in 1977 to 68% in 2001.

Exhibit 8 Production decline curves have become steeper (same in Louisiana).

LOGA/LMOGA Proposal for Percent Good (Depreciation) Page 10 of Proposal YearAgeHorizontalsGasOil & Other 2010 1 45 85 90 2009 2 34 76 84 2008 3 29 67 78 2007 4 26 54 70 2006 5 23 43 62 2005 6 20 33 54 2004 7 20 26 45 2003 8 20 22 37 2002 9 20 20 30 2001 10 20 20 25 2000 11 20 20 22 1999 12 20 20 20 & Prior

Conclusions from DCF Analysis • Drilling & completion costs and depth are irrelevant to the value of a well. The same projected income stream with equal risk from any historical cost or depth has the same value. • Age is generally irrelevant to the value of a well. The income stream is the most relevant factor in value. • A property tax appraised value of no more than the current year’s gross revenue per well and related surface equipment is a high “ceiling” that could be reasonably implemented in the LTC rules and regulations to bring a key market factor (income) into the valuation of taxable oil and gas property.

LOGA / LMOGA Oil & Gas Well Plugging Cost Survey($ thousands) # of Average P&A Plugging Net RegionWellsCost per WellCostReceivedValue 1 15 $108 $ 1,633 $ 61 -$ 1,571 2 204 246 50,185 363 - 49,822 3 66 310 20,454 221- 20,233 Totals 285 $254 $72,272 $645 -$71,626

Conclusions from Plug & Abandonment Survey • Most inactive wells (no potential reentry) have negative market value. Even if salvage value is received, it only slightly offsets the plugging cost (average < 1%). • Only inactive wells with potential reentry have value. • Permanently inactive platforms and facilities also have a negative value. I.e., the cost to decommission is far more than salvage value, which, when present, is relatively minimal. (Decommissioning agreements allowed contractors to keep whatever they could salvage.)

Observations of Orphan Wells • As of June 2, 2010, the LDNR SONRIS database indicated 2,846 orphan wells in Louisiana. • Why were they orphaned? They had no current or anticipated value. Worse than zero value, significant cost was required to plug and abandon ... and they would be liable for annual property taxes on over stated values (assuming current LTC rules and regulations for inactive wells continued). • What is the difference between orphan wells and permanently inactive wells with owners? The owners of orphan wells walked away from them. (They both have negative values).

LOGA / LMOGA Proposal for Obsolescence • Producing – One year revenue as the ceiling value for the well and related equipment (including surface equipment). • Inactive – Wells inactive less than two years should receive 90% reduction from depreciated value. Wells inactive over two years and not approved for reentry should receive an appraised value of $100. • Alternative – If the LTC denies #1 and #2 above, continue obsolescence adjustments a minimum as indicated in the 2010 rules and regulations. • Surface Equipment – Replace “may” with “shall” in Table 907.C-1.

Exhibit 1 Valuation of Louisiana Oil and Gas Wells for Property Taxes Legal Conclusions of Taxable Property Valuation Approach? Cost Taxable Cost (studies, company books) Additional Adjustments (if appropriate) Inflation Factor to Current Cost Reality Check (% of discounted cash flow value,sale of same property, other) Replacement Cost New Taxable Market Value Less Physical Depreciation (age from serial no.) Preliminary Market Value Review Status and Production Data for Shut-In and Low Producing Wells (LDNR, operators, other) Market Adjustments (obsolescence) Review Other Market Data (environmental, operators, buyers, sellers, other) RCNLD Less Some Market Adjustment Less Shut-In and Low Production Credits Red above indicates the major ongoing differences between industry and the LAA. The box indicates where assessors generally stop in their appraisal of wells.